sistema fiscal estatal y municipal - sdeslp.gob.mxsdeslp.gob.mx/estudios/experiencias...

TRANSCRIPT

sisteMa fisCal estatal y MUniCipal

State and municiPaL tax SyStem

E l sistema fiscal del Estado de San Luis Potosí es moderno y competitivo. Es normado por la Ley de Hacienda Pública

del Estado de San Luis Potosí. Los impuestos estatales para el año 2011, son sobre adquisición de vehículos automotores usados, sobre negocios o instrumentos jurídicos, sobre loterías, rifas, sorteos, concursos, apuestas y juegos permitidos, sobre nóminas, sobre servicios de hospedaje, sobre tenencia o uso de vehículos, y a la adquisición de bienes inmuebles desincorporados del régimen ejidal.

Por su parte, los impuestos municipales, para el caso de la capital del Estado, son regulados por la Ley de Ingresos de dicho municipio. Para el ejercicio fiscal 2011, los impuestos que incluye son el predial, adquisición de inmuebles y otros derechos reales, de plusvalía y el de espectáculos públicos.

The tax system of the State of San Luis Potosi is modern and competitive. It is regulated by the Law of Public Revenue of

the State of San Luis Potosi (Ley de Hacienda Pública del Estado de San Luis Potosi). State taxes for the year 2011, are on acquisition of used motor vehicles, business or legal instruments, lotteries, raffles, drawings, contests, legal gaming, payrolls, lodging, ownership or use of vehicles and the purchase of real estate not included in the ejido (coop) regime.

Municipal taxes for the capital of the State are regulated by the Law of Public Revenue of such municipality. Taxes for the fiscal year 2011 cover property tax, real estate and other real rights, capital gains and public performances.

E l sistema fiscal del Estado de San Luis Potosí es moderno y competitivo. Es normado por la Ley de Hacienda Pública del Estado de San Luis Potosí. En lo

no previsto por esta Ley, se aplicará supletoriamente el Código Fiscal del Estado y, en defecto de éste, las normas del derecho común local. Los impuestos estatales para el año 2011, son los siguientes:

Impuesto sobre adquisición de vehículos automotores usados. Son sujetos de este impuesto, las personas físicas o morales que adquieran vehículos automotores usados por cualquier título o causa, cuando por dichas operaciones no se cause el Impuesto al Valor Agregado. En las permutas se considerará que se efectúan dos adquisiciones. La base del impuesto será la que resulte de aplicar al valor total del automotor contenido en la factura, de la siguiente tabla de acuerdo al año de antigüedad de la unidad:

En ningún caso, el impuesto será menor a ocho días de salario mínimo general de la zona y la tasa del impuesto es el 1.5 por ciento sobre la base indicada en el artículo anterior. Son responsables solidarios del pago de este impuesto, sin perjuicio de lo que disponga el Código Fiscal del Estado, las personas siguientes: el enajenante del vehículo; los servidores públicos que, en ejercicio de sus funciones autoricen el cambio de propietario, baja o dotación de placas o cualquier trámite de control vehicular, sin comprobar el pago del impuesto; y los consignatarios o comisionistas que intervengan en cualquier operación de adquisición de vehículos automotores usados.

Impuesto Sobre Negocios o Instrumentos Jurídicos. Son sujetos de este impuesto, las personas físicas y morales, o unidades económicas que realicen, entre otros, los actos jurídicos relacionados con la constitución de sociedades civiles y mercantiles.

The tax system of the State of San Luis Potosi is modern and competitive. It is regulated by the Law of Public Revenue of the State of San Luis Potosi (Ley de Hacienda

Pública). In matters unforeseen by this Law, the State Tax Code (Código Fiscal del Estado) shall be additionally applied and, in its absence, the rules of local common law. State taxes for the 2011 fiscal year are as follows:

Tax on the purchase of used motor vehicles. Tax on acquisition of used motor vehicles. People or companies subject to this tax are individuals or legal entities who acquire used motor vehicles for whatever reason when Value Added Tax (Impuesto al Valor Agregado, IVA) is not applicable. The base tax will be the result of the total invoice value of the vehicle as shown in the table:

In no case may the tax be less than eight days local minimum salary and the tax rate shall be 1.5 percent as indicated above. The mutually responsible of the corresponding tax payment, are the seller of such vehicle and the public officer who authorizes its change of title, while exercising his authority and allows the issuance of new license plates, or any other transaction regarding vehicle control, without actually corroborating the payment of due tax, without breach to the articles set forth in the State Tax Law. Also jointly responsible shall be the commission agents or consignees in any acquisition transaction of used motor vehicles.

Tax on business or legal instruments. Subject to this tax are individuals, legal entities or economic units performing, among others, legal acts related to constituting partnerships and businesses.

v.1 iMpUestosestatalesstate tax

AÑOS DE ANTIGÜEDADAGE OF VEHICLE (YEARS)

1 2 3 4 5 6 7 8 9

FACTORFACTOR

0.850 0.725 0.600 0.500 0.400 0.300 0.225 0.150 0.075

Impuestos EstatalesState Tax

114 www.sdeslp.gob.mx

La base para el pago del impuesto será el capital de la sociedad, a razón del tres al millar; fusión de sociedades civiles y mercantiles. La base del impuesto será la diferencia entre el capital social de la fusionante, antes y después de la fusión, a razón del tres al millar; aumentos de capital de sociedades civiles y mercantiles. La base será el importe del capital aumentado, a razón del tres al millar; disolución y liquidación de sociedades. La base del impuesto será el número de fojas del instrumento, a razón de un día de salario mínimo, por cada una; cualquier otra modificación a escrituras constitutivas de sociedades. La base del impuesto será el número de fojas del documento donde conste la modificación, a razón de un día de salario mínimo, por foja; y contratos de mutuo entre particulares, con garantía prendaria o hipotecaria, así como la constitución de estas garantías para el cumplimiento de cualquier otra obligación. La base del impuesto será el importe del contrato y, la tasa, a razón de tres al millar.

Impuesto Sobre Loterías, Rifas, Sorteos, Concursos, Apuestas y Juegos Permitidos. Es objeto de este impuesto gravar los ingresos provenientes de la realización o celebración, así como de la obtención de premios en efectivo o en especie, derivados de la celebración de rifas, sorteos, loterías, apuestas, juegos con máquinas de sistemas, programas automatizados o computarizados, concursos de cualquier índole, que lleven a cabo entidades públicas o privadas. El impuesto se causa al momento en que se efectúe la explotación de las actividades señaladas, así como al instante del pago o entrega del premio. Son sujetos de este impuesto, las personas físicas o morales, o unidades económicas sin personalidad jurídica que realicen o celebren rifas, sorteos, loterías, apuestas y concursos de toda clase, así como juegos con máquinas de sistemas, programas automatizados o computarizados, aún cuando por dichos eventos no se cobre cantidad alguna que represente el derecho a participar en los mismos, y que obtengan ingresos o premios derivados o relacionados con las actividades indicadas

The basis for the tax shall be the capital of the company, at a rate of three to one thousand; merging partnerships and businesses. The tax base shall be the difference between social capital of the merger, before and after merging at a rate of three to one thousand; Capital increase in partnerships and businesses. The tax base shall be the amount of the increase in capital at a rate of three to one thousand; termination and liquidation of partnerships. The tax base shall be the number of pages of the document, in proportion to one day’s minimum salary per page; Any other modification to articles of incorporation. The tax base shall be the number of pages of the document that contains the modification, in proportion to one day’s minimum salary per page; and Contracts held between individuals, with collateral security or mortgage, as well as the constitution of these guarantees for compliance with any other obligations. The tax base shall be the cost of the contract at the rate of three to one thousand.

Taxation of lotteries, raffles, drawings, contests, and legal betting and gaming. It is the object of this tax to lev y income arising from winning, such as cash prizes or specif ically derived from the winning of raf f les, drawings, lot teries, gambling, machine gaming, automated or computerized programs or contest s of any kind, that are carried out by public or private entit ies. The tax is applied the moment such activit ies are realized, and also at the time of payment or deliver y of the prize. Subject to this tax, are individuals, legal entit ies or economic groups without legal status that engage in raf f les, drawings, lot teries, gambling and contest s of any kind, as well as machine gaming, automated programs, even when these event s are not charged any amount for the right to par ticipate including income or prizes deriving

BUSINESS GUIDE 2011 115

previamente, incluyendo las participaciones de bolsas formadas con el importe de las inscripciones o cuotas que se distribuyan en función del resultado de las propias actividades. Para efectos del cálculo el impuesto se determinará aplicando la tasa del 5 por ciento al valor nominal de la suma de los billetes, boletos, contraseñas, documentos, objetos o registros distribuidos para participar en loterías, rifas, concursos, sorteos y juegos con máquinas de sistemas, programas automatizados o computarizados; y en cuanto a los concursos, el impuesto se determinará aplicando la tasa del 6 por ciento sobre el monto total de los ingresos obtenidos, por las inscripciones que permitan participar en el evento.

Impuestos Sobre Nóminas. Son objeto de este impuesto las erogaciones pagadas dentro del territorio del Estado, en dinero o en especie, por concepto de remuneración al trabajo personal subordinado, considerándose como tales salarios y, en general, toda remuneración derivada de una relación laboral; honorarios y todo tipo de pagos realizados a los administradores, comisarios o miembros de los consejos directivos y de vigilancia en toda clase de sociedades y asociaciones; y honorarios a personas que presten servicios profesionales en forma preponderante al contribuyente, en términos de lo dispuesto por la Ley del Impuesto Sobre la Renta. Los sujetos de este impuesto son las personas físicas y morales o unidades económicas que dentro del territorio del Estado, realizan las erogaciones señaladas. El Impuesto se causará y pagará a razón del dos por ciento, se causará en el momento en que se realicen las erogaciones objeto del impuesto y se pagará en forma mensual mediante declaración que deberá presentarse a más tardar el día quince del mes siguiente al de las erogaciones. Para el fomento de la inversión productiva y la generación de empleos, las empresas de nueva creación por el primer año de funcionamiento, recibirán un estímulo fiscal hasta del cien por ciento del Impuesto sobre Nóminas. No se consideran de nueva creación las que deriven de

from these. Also including distribution of amount s arising from registration fees and resulting from such activit ies. For tax calculation purposes, a rate of 5 percent shall be applied on the nominal value of the sum of the ticket s, vouchers, passwords, document s, object s or records distributed for par ticipation in lot teries, raf f les, contest s, drawings, and machine gaming, computerized or automated programs. And in the case of contest s, the tax shall be determined by applying a rate of 6 percent over the total amount of the income gained from enrollment for par ticipation in the event.

Payroll Tax. Subject to this tax are expenditures made within the State limits, whether in money or in kind, by concept of payment to the workforce, payments deemed as salaries and in general any remuneration derived from a labor relation, professional fees and any and all types of payments made to administrators, commissioners or members of boards of directors and supervisors, and any and all types of partnerships and associations; and fees for predominant professional services provided to taxpayers in the terms set forth in the Income Tax Law (Ley del Impuesto Sobre la Renta). Subject to this tax are individuals, legal entities or economic groups that realize such expenditures within the State. The tax rate shall be of two percent and such taxes shall be paid monthly by means of a written document which shall be submitted no later than the fifteenth of the month following the expenditure. To promote productive investment and employment new companies shall receive a fiscal stimulus of up to one hundred percent of their payroll tax during the first year of operations. Merging or dividing companies shall not be participants of this benefit,

116 www.sdeslp.gob.mx

escisión o fusión de sociedades, o aquéllas cuyos trabajadores provengan de sustitución patronal de otras empresas relacionadas por pertenencia accionaria.

Impuesto Sobre Servicios de Hospedaje. Es objeto de este impuesto el pago por el servicio de hospedaje que se reciba en hoteles, moteles, suites posadas, campamentos, paraderos de casas rodantes y de tiempo compartido, así como en toda clase de establecimientos que presten servicios de esta naturaleza. No se consideran servicios de hospedaje, el albergue o alojamientos prestados por hospitales, clínicas, asilos, conventos, seminarios, internados y aquellos prestados por establecimientos con fines no lucrativos. Son sujetos al pago del impuesto todas las personas físicas o morales que dentro del Estado de San Luis Potosí reciban los servicios mencionados. La base para el cálculo y determinación del impuesto será el importe pagado en efectivo, bienes o servicios, considerando solo el albergue sin incluir alimentos, demás servicios relacionados y el impuesto al valor agregado. El impuesto se calculará y determinará aplicando a la base señalada, una tasa del 2 por ciento y se causará en el momento de pago por la prestación del servicio de hospedaje recibido.

Impuesto Estatal Sobre Tenencia o Uso de Vehículos. Es objeto de este impuesto gravar la tenencia o uso de vehículos automotrices, de más de diez años de fabricación o ejercicio automotriz, anteriores al ejercicio fiscal en curso, a que se refiere el artículo 5o. fracción V de la Ley Federal del Impuesto sobre Tenencia o Uso de Vehículos. Son sujetos de este impuesto las personas físicas y morales tenedoras o usuarias de vehículos automotores. El impuesto local sobre tenencia o uso de vehículos se pagará mediante declaración, en la forma oficial aprobada,

neither will those companies whose employees proceed from substitution employment from other companies related through stock ownership.

Tax on Boarding and Lodging Services. The object of this tax is for lodging in hotels, motels, inns, campsites, trailer areas and timeshares, as well as any and all establishments that provide services of this type. Lodging services not deemed as such are shelters provided by hospitals, clinics, homes, convents, seminaries, boarding institutions and those provided by non-profit establishments. Subject to taxation are individuals, legal entities, who within the State of San Luis Potosi receive such services. The basis for calculation and determination of this tax shall be the amount paid in cash, goods or services, considering only shelter but excluding food and other related services and the Value Added Tax (Impuesto al Valor Agregado, IVA). The tax shall be calculated and determined applying the set base, a rate of 2 percent and shall be applied at the moment of payment for services rendered.

State Tax for Ownership and Use of Vehicles. This tax encases ownership or use of vehicles over 10 years old or in use, previous to the current fiscal year, referred to in Article 5, Section V of the Federal Law of Tax on Ownership or Use of Vehicles (Ley Federal del Impuesto Sobre Tenencia o Uso de Vehículos). Individuals and legal entities owning or using vehicles are subject to this tax. The tax for owning or using vehicles shall be paid by means of an officially authorized writ ten declaration, within the first 3 months of each year; together with the

BUSINESS GUIDE 2011 117

dentro de los tres primeros meses de cada año; conjuntamente con los derechos de control vehicular. El impuesto sobre tenencia o uso de vehículos se pagará conforme a las siguientes tarifas, en salarios mínimos: vehículos automotores de más de diez años y hasta veinte, pagarán 3; y motocicletas y motonetas, pagarán 1.5.

Impuesto a la Adquisición de Bienes Inmuebles Desincorporados del Régimen Ejidal. Son sujetos del impuesto las personas físicas y morales o unidades económicas que adquieran, en su primera enajenación, mediante cualquier forma de transmisión legal de la propiedad, bienes inmuebles desincorporados del régimen ejidal. Cuando los adquirentes o beneficiarios sean la Federación, Estados o municipios, así como los organismos públicos descentralizados de cualquiera de los tres órdenes de gobierno, los mismos estarán exentos del pago de dicho impuesto. Asimismo, estarán exentos los ejidatarios cuando transmitan por cualquier figura legal de uno a otro, bienes desincorporados del régimen ejidal. La base para el cálculo y determinación del impuesto será la que resulte mayor entre el precio pactado o valor declarado y el valor catastral del inmueble. Para efecto de determinar la base del impuesto deberá atenderse al valor que arroje el avalúo catastral con una antigüedad no mayor de seis meses a partir de la fecha en que se formalice la operación. El impuesto se calculará y determinará aplicando a la base anterior, la tasa del diez por ciento. Este impuesto se causará en el momento de la protocolización del acto jurídico por el que se transmita la propiedad del bien inmueble de que se trate, mediante la escritura pública correspondiente.

vehicle permit. The tax for ownership or use of vehicles shall be paid conforming to the following rates based on minimum wages: 10 to 20-year-old vehicles shall pay 3; and motorcycles and motorscooters shall pay 1.5. Taxation of the Acquisition of Real Estate not included in the Ejido (coop) regime. Subject to this tax are individuals, legal entities or economic units that acquire, in the first alienation through any form of legal transfer of property, real estate not included in the Ejido (coop) regime. When the Federal Government, states, or municipalities are the purchasers, including public entities decentralized from any of the three branches of government, these shall be exempt of such tax. Also, the communal landholders (ejidatarios) shall be exempt when property transfers not included in the Ejido regime are made from one legal figure to another. The base for calculation and determination of this tax shall be the amount of the largest difference resulting between the agreed price or declared value and the registered value of the property. For the purpose of determining the basis of the tax it shall be related to the appraisal registered not more than six months previous to the date of the transaction. The tax shall be calculated and determined at a rate of 10 percent as in the previously established base. The tax shall be effective at the moment of recording the deed, whereby the property has been transferred, in the corresponding protocols.

118 www.sdeslp.gob.mx

L os impuestos municipales son regulados por la Ley de Ingresos del Municipio de San Luis Potosí. Para el ejercic io f iscal 2011, se incluyen los siguientes:

Predial. Este impuesto se calculará aplicando la tasa que corresponda de acuerdo al tipo de predio, y sobre la base gravable que señala la Ley de Hacienda para los Municipios de San Luis Potosí.

Adquisición de Inmuebles y Otros Derechos Reales. Este impuesto se pagará aplicando la tasa neta del 1.6 por ciento sobre la base gravable: no pudiendo ser este impuesto en ningún caso, inferior al importe de 4 salario mínimo general diario de la zona económica que corresponda al Estado de San Luis Potosí (SMGZ). Para los efectos de vivienda de interés social y vivienda popular se deducirá de la base gravable el importe de 15 SMGZ elevados al año, y del impuesto a pagar resultante se reducirá el 50 por ciento; el importe del impuesto a pagar en ningún caso podrá ser inferior a 4 SMGZ. Se considerará vivienda de interés social aquella cuyo valor global al término de la construcción no exceda de 20 SMGZ elevados al año; se considera vivienda de interés popular aquélla cuyo valor global al término de la construcción no exceda de 30 SMGZ elevados al año, siempre y cuando el adquiriente sea persona física y no tenga ninguna otra propiedad u otros derechos reales.

De Plusvalía. Este impuesto se causará aplicando a la base gravable establecida por la Ley de Hacienda para los Municipios de San Luis Potosí, las tasas señaladas por esta Ley en materia de impuesto predial.

Municipal taxes are regulated by the Law of Municipal Income of San Luis Potosi (Ley de Ingresos del Municipio de San Luis Potosi). For the 2011 fiscal year, the following

are included:

Real Estate Tax. This tax shall be calculated by applying a rate correspondant to the property type, and over the tax base indicated in the Income Tax Law for the Municipalities of San Luis Potosi.

Property Acquisition and other Real Rights. This tax shall be paid by applying the net rate of 1.6 percent over the taxable base: this tax shall not in any case amount to less than the total cost of 4 Minimum Wage in Force (Salario Mínimo General en la Zona, SMGZ) corresponding to the State of San Luis Potosi. In the case of social and popular dwellings the total amount of 15 Minimum Wage in Force (Salario Mínimo General en la Zona, SMGZ ) to year will be deducted from the taxable base, and the resulting tax shall be reduced by 50 percent; the total tax to be paid may not be less than 4 SMGZ in any case. Social dwellings are those whose global value at the end of construction do not exceed 20 SMGZ to year; popular dwellings are those whose global value at end of construction do not exceed 30 SMGZ to year, if and when the buyer is an individual and does not own any other property or real rights.

Capital Gains. This tax shall be effective by conforming to the rates set forth in the Law of Revenue for the Municipalities of San Luis Potosi (Ley de Hacienda para los Muncipios de San Luis Potosi), regarding property tax.

v.2 iMpUestos MUniCipalesMUniCipal tax

BUSINESS GUIDE 2011 119

Espectáculos Públicos. Este impuesto se aplicará de acuerdo a lo establecido con la Ley de Hacienda para los Municipios de San Luis Potosí, y de acuerdo al anexo 5 del Convenio de Adhesión al Sistema Nacional de Coordinación Fiscal, se cobrará la tasa de 4 por ciento a los que demuestren estar dentro de los lineamientos que marca dicho convenio.

Public Performances. The Law of Revenue for the Municipalities of San Luis Potosi (Ley de Hacienda para los Municipios de San Luis Potosi) shall be the guideline for the application of this tax and in accordance with Appendix 5 of the Council of Support to the National System of Fiscal Coordination (Convenio de Adhesión al Sistema Nacional de Coordinación Fiscal), the rate of 4 percent shall be charged to those who prove compliance with the regulations set forth in such agreement.

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ Vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

ESTATALES / STATE

CONCEPTOCONCEPT

•Por Otorgamiento,sustitución, renunciao renovación de poderes.•For granting, substitution, waiveror renewal of powers.

•Por Cesión de los derechosderivados de los actos y contratos de mutuoentre particulares.•For Assigment of rights resultingfrom the acts and contractsby mutual between individuals.

•Por Contratos de mutuo entreparticulares, con garantíaprendaría o hipotecaria.•For Contracts by mutual betweenindividuals, with collateral or mortgage.

•Por Modificación a EscriturasConstitutivas de Sociedades.•For Modifications to Corporate Deeds.

•Por Disolución y Liquidaciónde Sociedades.•For Termination and Liquidationof Business Partnerships.

•Por Aumentos de Capital de Sociedades Civiles y Mercantiles.•For Capital Increases in Partnershipsand Corporations.

•Por Fusión de SociedadesCiviles y Mercantiles.•For Merging Partnerships and Corporations.

•Por Constitución de SociedadesCiviles y Mercantiles.•For Constitution of Partnershipsand Corporations.

•Por la Adquisicion de VehículosAutomotores Usados.•For Acquisition of Used Motor Vehicles.

•Por Rectificaciones o ratificacionesde cualquier acto o contrato.•Por Rectification or ratificationof any legal acts or contracts.

TASA ó TARIFARATE OR TARIFF

Un día de salariomínimo generalde la zona,por cada otorgante.One day’s general minimumwage in the area,per grantor.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

Un día de salario mínimo general de la zona, por foja.One day’s general minimumwage in the area, per page.

Un día de salariomínimo generalen la zona,por cada una.One day’s generalminimum wage in thearea, for each.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

1.5 %1.5 %

Un día de salariomínimo general de la zona por foja. One day’s general minimumwage in the area, per page.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre cada otorgante.Based on each grantor.

Sobre el monto de los actosjurídicos y con garantíaprendaría o hipotecaria.Based on the legal actswith collateral and mortgage.

Sobre el importe del contrato.Based on the amount of the contract.

Sobre el número de fojasdel documento donde constela modificación.Based on the number of pagesof the document holding suchmodifications.

Sobre el número de fojasdel instrumento.Based on the number ofpages of the document.

Sobre el importe del capitalaumentado.Based on the amount ofcapital increase.

Sobre la diferencia entreel capital social de la fusionante,antes y después de la fusión.Based on the difference in capitalstock of the merging companybefore and after the merge.

Sobre el capital de la sociedad.Based on the capital of the company.

Sobre el valor de la facturase aplicará el factor señaladoen el Art. 6° de acuerdoal año de antigüedadde la unidad y se obtendrála base del impuesto. 1_/Based on the value of the invoicein accordance withArticle 6 and considering the ageof the vehicle. 1_/

Sobre cada foja.Based on each page.

San Luis Potosí. Sistema Fiscal Estatal y MunicipalSan Luis Potosí. State and Municipal Tax System

120 www.sdeslp.gob.mx

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

ESTATALES / STATE

CONCEPTOCONCEPT

•Por Otorgamiento,sustitución, renunciao renovación de poderes.•For granting, substitution, waiveror renewal of powers.

•Por Cesión de los derechosderivados de los actos y contratos de mutuoentre particulares.•For Assigment of rights resultingfrom the acts and contractsby mutual between individuals.

•Por Contratos de mutuo entreparticulares, con garantíaprendaría o hipotecaria.•For Contracts by mutual betweenindividuals, with collateral or mortgage.

•Por Modificación a EscriturasConstitutivas de Sociedades.•For Modifications to Corporate Deeds.

•Por Disolución y Liquidaciónde Sociedades.•For Termination and Liquidationof Business Partnerships.

•Por Aumentos de Capital de Sociedades Civiles y Mercantiles.•For Capital Increases in Partnershipsand Corporations.

•Por Fusión de SociedadesCiviles y Mercantiles.•For Merging Partnerships and Corporations.

•Por Constitución de SociedadesCiviles y Mercantiles.•For Constitution of Partnershipsand Corporations.

•Por la Adquisicion de VehículosAutomotores Usados.•For Acquisition of Used Motor Vehicles.

•Por Rectificaciones o ratificacionesde cualquier acto o contrato.•Por Rectification or ratificationof any legal acts or contracts.

TASA ó TARIFARATE OR TARIFF

Un día de salariomínimo generalde la zona,por cada otorgante.One day’s general minimumwage in the area,per grantor.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

Un día de salario mínimo general de la zona, por foja.One day’s general minimumwage in the area, per page.

Un día de salariomínimo generalen la zona,por cada una.One day’s generalminimum wage in thearea, for each.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

1.5 %1.5 %

Un día de salariomínimo general de la zona por foja. One day’s general minimumwage in the area, per page.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre cada otorgante.Based on each grantor.

Sobre el monto de los actosjurídicos y con garantíaprendaría o hipotecaria.Based on the legal actswith collateral and mortgage.

Sobre el importe del contrato.Based on the amount of the contract.

Sobre el número de fojasdel documento donde constela modificación.Based on the number of pagesof the document holding suchmodifications.

Sobre el número de fojasdel instrumento.Based on the number ofpages of the document.

Sobre el importe del capitalaumentado.Based on the amount ofcapital increase.

Sobre la diferencia entreel capital social de la fusionante,antes y después de la fusión.Based on the difference in capitalstock of the merging companybefore and after the merge.

Sobre el capital de la sociedad.Based on the capital of the company.

Sobre el valor de la facturase aplicará el factor señaladoen el Art. 6° de acuerdoal año de antigüedadde la unidad y se obtendrála base del impuesto. 1_/Based on the value of the invoicein accordance withArticle 6 and considering the ageof the vehicle. 1_/

Sobre cada foja.Based on each page.

San Luis Potosí. Sistema Fiscal Estatal y MunicipalSan Luis Potosí. State and Municipal Tax System

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

ESTATALES / STATE

CONCEPTOCONCEPT

•Por Otorgamiento,sustitución, renunciao renovación de poderes.•For granting, substitution, waiveror renewal of powers.

•Por Cesión de los derechosderivados de los actos y contratos de mutuoentre particulares.•For Assigment of rights resultingfrom the acts and contractsby mutual between individuals.

•Por Contratos de mutuo entreparticulares, con garantíaprendaría o hipotecaria.•For Contracts by mutual betweenindividuals, with collateral or mortgage.

•Por Modificación a EscriturasConstitutivas de Sociedades.•For Modifications to Corporate Deeds.

•Por Disolución y Liquidaciónde Sociedades.•For Termination and Liquidationof Business Partnerships.

•Por Aumentos de Capital de Sociedades Civiles y Mercantiles.•For Capital Increases in Partnershipsand Corporations.

•Por Fusión de SociedadesCiviles y Mercantiles.•For Merging Partnerships and Corporations.

•Por Constitución de SociedadesCiviles y Mercantiles.•For Constitution of Partnershipsand Corporations.

•Por la Adquisicion de VehículosAutomotores Usados.•For Acquisition of Used Motor Vehicles.

•Por Rectificaciones o ratificacionesde cualquier acto o contrato.•Por Rectification or ratificationof any legal acts or contracts.

TASA ó TARIFARATE OR TARIFF

Un día de salariomínimo generalde la zona,por cada otorgante.One day’s general minimumwage in the area,per grantor.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

Un día de salario mínimo general de la zona, por foja.One day’s general minimumwage in the area, per page.

Un día de salariomínimo generalen la zona,por cada una.One day’s generalminimum wage in thearea, for each.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

1.5 %1.5 %

Un día de salariomínimo general de la zona por foja. One day’s general minimumwage in the area, per page.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre cada otorgante.Based on each grantor.

Sobre el monto de los actosjurídicos y con garantíaprendaría o hipotecaria.Based on the legal actswith collateral and mortgage.

Sobre el importe del contrato.Based on the amount of the contract.

Sobre el número de fojasdel documento donde constela modificación.Based on the number of pagesof the document holding suchmodifications.

Sobre el número de fojasdel instrumento.Based on the number ofpages of the document.

Sobre el importe del capitalaumentado.Based on the amount ofcapital increase.

Sobre la diferencia entreel capital social de la fusionante,antes y después de la fusión.Based on the difference in capitalstock of the merging companybefore and after the merge.

Sobre el capital de la sociedad.Based on the capital of the company.

Sobre el valor de la facturase aplicará el factor señaladoen el Art. 6° de acuerdoal año de antigüedadde la unidad y se obtendrála base del impuesto. 1_/Based on the value of the invoicein accordance withArticle 6 and considering the ageof the vehicle. 1_/

Sobre cada foja.Based on each page.

San Luis Potosí. Sistema Fiscal Estatal y MunicipalSan Luis Potosí. State and Municipal Tax System

San Luis Potosí. Sistema �scal estatal y municipalSan Luis Potosí. State and municipal tax system

CONCEPTOCONCEPT

ESTATALES / STATE

•Por Cualquier otro tipo de actoo contrato que representeo no intereses pecuniarios para los otorgantes. 2_/•For any other type of legal actor agreement whether or not theyrepresent the financial interestsof the grantors. 2_/

•Por Cualquier acto o contratootorgado fuera del Estadoque produzca o pueda producirefectos dentro del territoriode éste. 3_/•For any legal act or contract awardedoutside the State that may have legaleffects within the territoryof such State. 3_/

•Por Resoluciones o mandatosjudiciales que representen o nointereses pecuniariospara los involucrados,pero que tengan efectoscontractuales.•For resolutions or court orderswhether or not representing financialinterests for those involvedhowever having contractual effects.

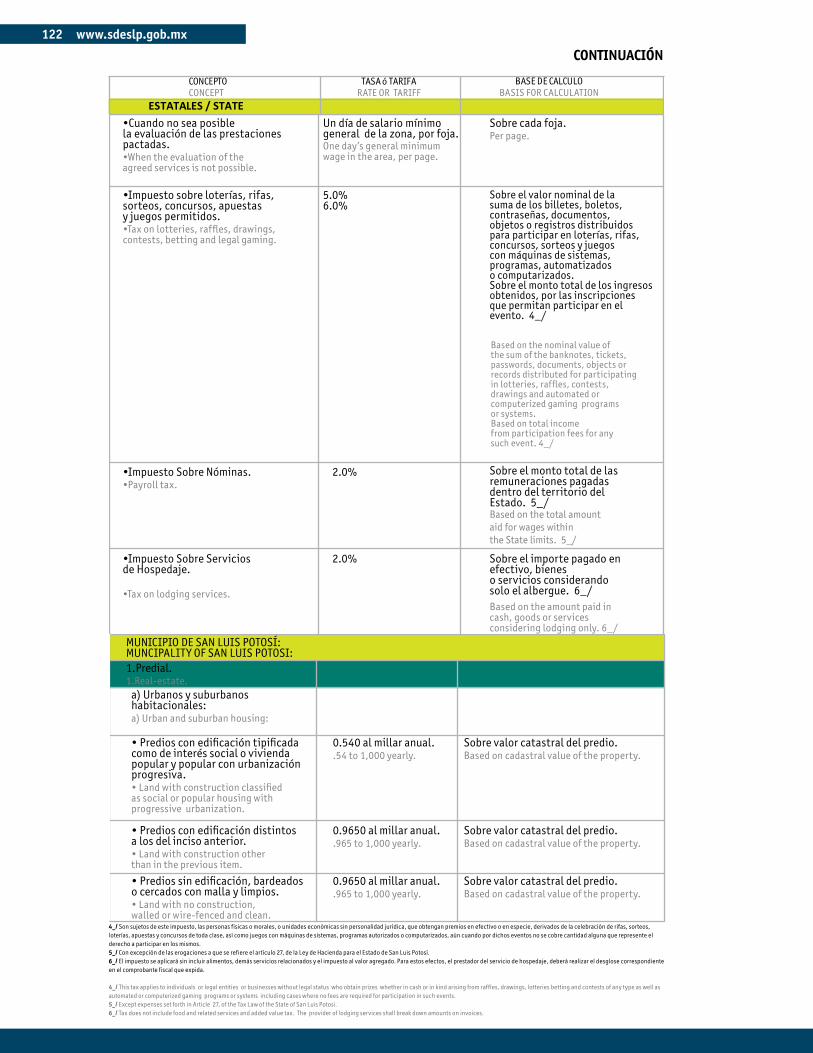

•Cuando no sea posiblela evaluación de las prestacionespactadas.•When the evaluation of theagreed services is not possible.

•Impuesto sobre loterías, rifas,sorteos, concursos, apuestasy juegos permitidos.•Tax on lotteries, raffles, drawings,contests, betting and legal gaming.

•Impuesto Sobre Nóminas.•Payroll tax.

•Impuesto Sobre Serviciosde Hospedaje.

•Tax on lodging services.

•Por Celebración de contratosde arrendamiento financieroen todas sus modalidades,entre particulares o institucionesde crédito.•For holding leasing agreementsof any type, between individualsor credit institutions.

•Por Celebraciónde instrumentos privados.•For private legal instruments.

TASA ó TARIFARATE OR TARIFF

Un día de salario mínimogeneral de la zona, por foja.One day’s general minimumwage in the area, per page.

3 al millar en caso de quehaya capital, y si no lo hubiere será de un día desalario mínimogeneral de la zona, por foja.3 to 1,000 in case of capitalotherwise one day’s generalminimum wage in the area,per page.

Un día de salario mínimogeneral de la zona, porcada particular involucrado.One day’s general minimumwage in the area, perparticipating individual.

Un día de salario mínimogeneral de la zona, por foja.One day’s general minimumwage in the area, per page.

5.0%6.0%

2.0%

2.0%

3 al millar.3 to 1,000.

20.0% del salario mínimogeneral de la zona, porcada otorgante.20% of the general minimumwage in the area per grantor.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre el número de fojas.Based on the number of pages.

Sobre el capital o por foja.Based on capital or by pages.

Sobre cada particularinvolucrado.Based on each participatingindividual .

Sobre cada foja.Per page.

Sobre el valor nominal de lasuma de los billetes, boletos,contraseñas, documentos,objetos o registros distribuidospara participar en loterías, rifas,concursos, sorteos y juegoscon máquinas de sistemas,programas, automatizadoso computarizados.Sobre el monto total de los ingresosobtenidos, por las inscripcionesque permitan participar en elevento. 4_/

Based on the nominal value ofthe sum of the banknotes, tickets,passwords, documents, objects orrecords distributed for participatingin lotteries, raffles, contests,drawings and automated orcomputerized gaming programsor systems.Based on total incomefrom participation fees for any such event. 4_/

Sobre el monto total de lasremuneraciones pagadas dentro del territorio delEstado. 5_/Based on the total amount aid for wages withinthe State limits. 5_/

Sobre el importe pagado enefectivo, bienes o servicios considerandosolo el albergue. 6_/Based on the amount paid incash, goods or servicesconsidering lodging only. 6_/

Based on the amount ofthe contract.

Sobre el monto del contrato.

Sobre cada otorgante.Based on each grantor.

2_/ Siempre que el acto contenido en éstos no esté gravado por otro impuesto estatal, así como las actas notariales que contengan certificación de hechos.3_/ También cuando señale algún punto del Estado para el cumplimiento de las obligaciones estipuladas. 2_/ Provided that the act contained in these is not taxed by another state tax, as well as official notarized acts containing certification of facts.3_/ Also when the State is referred to in order to comply with the stipulated obligations.

CONTINUACIóNBUSINESS GUIDE 2011 121

San Luis Potosí. Sistema �scal estatal y municipalSan Luis Potosí. State and municipal tax system

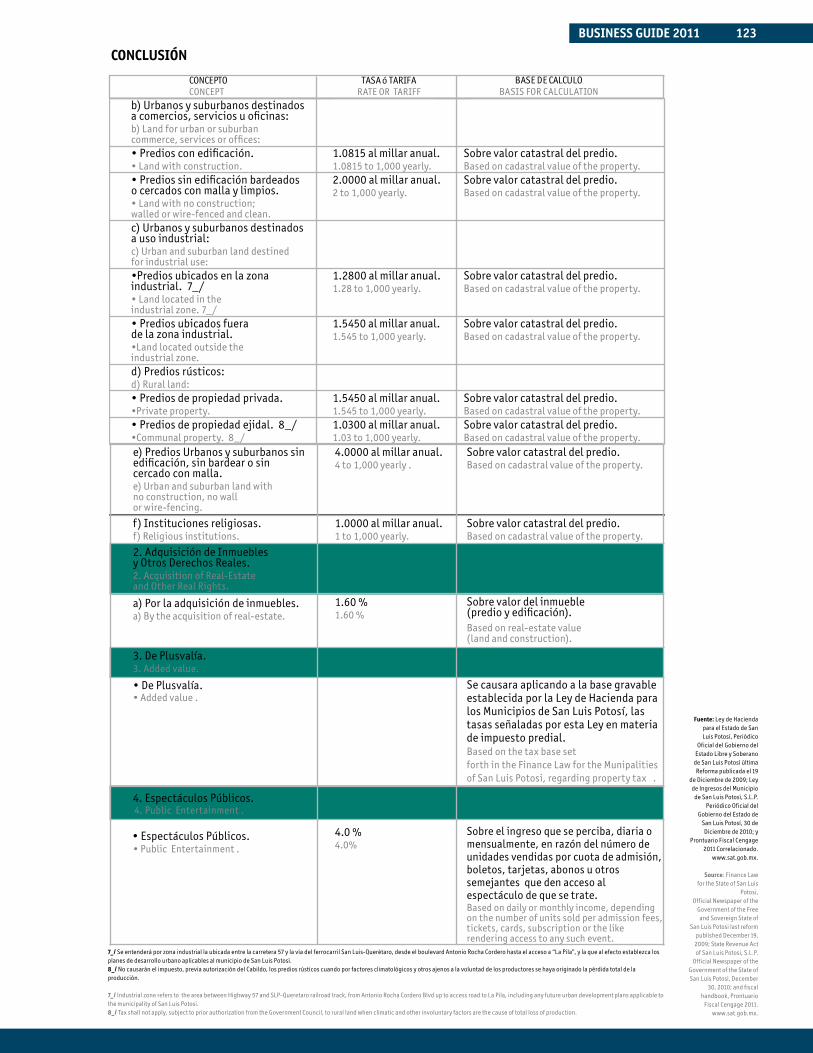

7_/ Se entenderá por zona industrial la ubicada entre la carretera 57 y la vía del ferrocarril San Luis-Querétaro, desde el boulevard Antonio Rocha Cordero hasta el acceso a “La Pila”, y la que al efecto establezca los planes de desarrollo urbano aplicables al municipio de San Luis Potosí.8_/ No causarán el impuesto, previa autorización del Cabildo, los predios rústicos cuando por factores climatológicos y otros ajenos a la voluntad de los productores se haya originado la pérdida total de la producción.

7_/ Industrial zone refers to the area between Highway 57 and SLP-Queretaro railroad track, from Antonio Rocha Cordero Blvd up to access road to La Pila, including any future urban development plans applicable tothe municipality of San Luis Potosi. 8_/ Tax shall not apply, subject to prior authorization from the Government Council, to rural land when climatic and other involuntary factors are the cause of total loss of production.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.Sobre valor catastral del predio.Based on cadastral value of the property.

TASA ó TARIFARATE OR TARIFF

0.540 al millar anual..54 to 1,000 yearly.

0.9650 al millar anual..965 to 1,000 yearly.

0.9650 al millar anual..965 to 1,000 yearly.

1.0815 al millar anual.1.0815 to 1,000 yearly.2.0000 al millar anual.2 to 1,000 yearly.

1.2800 al millar anual.1.28 to 1,000 yearly.

1.5450 al millar anual.1.545 to 1,000 yearly.

1.5450 al millar anual.1.545 to 1,000 yearly.1.0300 al millar anual.1.03 to 1,000 yearly.

CONCEPTOCONCEPT

MUNICIPIO DE SAN LUIS POTOSÍ:MUNCIPALITY OF SAN LUIS POTOSI:1.Predial.1.Real-estate.

a) Urbanos y suburbanoshabitacionales:a) Urban and suburban housing:

• Predios con edificación tipificadacomo de interés social o viviendapopular y popular con urbanizaciónprogresiva.• Land with construction classifiedas social or popular housing withprogressive urbanization.

• Predios con edificación distintosa los del inciso anterior.• Land with construction otherthan in the previous item.

• Predios sin edificación, bardeadoso cercados con malla y limpios.• Land with no construction,walled or wire-fenced and clean.b) Urbanos y suburbanos destinadosa comercios, servicios u o�cinas:b) Land for urban or suburbancommerce, services or of�ces:• Predios con edificación.• Land with construction.• Predios sin edificación bardeadoso cercados con malla y limpios.• Land with no construction;walled or wire-fenced and clean.c) Urbanos y suburbanos destinadosa uso industrial:c) Urban and suburban land destinedfor industrial use:•Predios ubicados en la zonaindustrial. 7_/• Land located in theindustrial zone. 7_/• Predios ubicados fuerade la zona industrial.•Land located outside theindustrial zone.d) Predios rústicos:d) Rural land:• Predios de propiedad privada.•Private property.• Predios de propiedad ejidal. 8_/•Communal property. 8_/

San Luis Potosí. Sistema �scal estatal y municipalSan Luis Potosí. State and municipal tax system

CONCEPTOCONCEPT

ESTATALES / STATE

•Por Cualquier otro tipo de actoo contrato que representeo no intereses pecuniarios para los otorgantes. 2_/•For any other type of legal actor agreement whether or not theyrepresent the financial interestsof the grantors. 2_/

•Por Cualquier acto o contratootorgado fuera del Estadoque produzca o pueda producirefectos dentro del territoriode éste. 3_/•For any legal act or contract awardedoutside the State that may have legaleffects within the territoryof such State. 3_/

•Por Resoluciones o mandatosjudiciales que representen o nointereses pecuniariospara los involucrados,pero que tengan efectoscontractuales.•For resolutions or court orderswhether or not representing financialinterests for those involvedhowever having contractual effects.

•Cuando no sea posiblela evaluación de las prestacionespactadas.•When the evaluation of theagreed services is not possible.

•Impuesto sobre loterías, rifas,sorteos, concursos, apuestasy juegos permitidos.•Tax on lotteries, raffles, drawings,contests, betting and legal gaming.

•Impuesto Sobre Nóminas.•Payroll tax.

•Impuesto Sobre Serviciosde Hospedaje.

•Tax on lodging services.

•Por Celebración de contratosde arrendamiento financieroen todas sus modalidades,entre particulares o institucionesde crédito.•For holding leasing agreementsof any type, between individualsor credit institutions.

•Por Celebraciónde instrumentos privados.•For private legal instruments.

TASA ó TARIFARATE OR TARIFF

Un día de salario mínimogeneral de la zona, por foja.One day’s general minimumwage in the area, per page.

3 al millar en caso de quehaya capital, y si no lo hubiere será de un día desalario mínimogeneral de la zona, por foja.3 to 1,000 in case of capitalotherwise one day’s generalminimum wage in the area,per page.

Un día de salario mínimogeneral de la zona, porcada particular involucrado.One day’s general minimumwage in the area, perparticipating individual.

Un día de salario mínimogeneral de la zona, por foja.One day’s general minimumwage in the area, per page.

5.0%6.0%

2.0%

2.0%

3 al millar.3 to 1,000.

20.0% del salario mínimogeneral de la zona, porcada otorgante.20% of the general minimumwage in the area per grantor.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre el número de fojas.Based on the number of pages.

Sobre el capital o por foja.Based on capital or by pages.

Sobre cada particularinvolucrado.Based on each participatingindividual .

Sobre cada foja.Per page.

Sobre el valor nominal de lasuma de los billetes, boletos,contraseñas, documentos,objetos o registros distribuidospara participar en loterías, rifas,concursos, sorteos y juegoscon máquinas de sistemas,programas, automatizadoso computarizados.Sobre el monto total de los ingresosobtenidos, por las inscripcionesque permitan participar en elevento. 4_/

Based on the nominal value ofthe sum of the banknotes, tickets,passwords, documents, objects orrecords distributed for participatingin lotteries, raffles, contests,drawings and automated orcomputerized gaming programsor systems.Based on total incomefrom participation fees for any such event. 4_/

Sobre el monto total de lasremuneraciones pagadas dentro del territorio delEstado. 5_/Based on the total amount aid for wages withinthe State limits. 5_/

Sobre el importe pagado enefectivo, bienes o servicios considerandosolo el albergue. 6_/Based on the amount paid incash, goods or servicesconsidering lodging only. 6_/

Based on the amount ofthe contract.

Sobre el monto del contrato.

Sobre cada otorgante.Based on each grantor.

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

ESTATALES / STATE

CONCEPTOCONCEPT

•Por Otorgamiento,sustitución, renunciao renovación de poderes.•For granting, substitution, waiveror renewal of powers.

•Por Cesión de los derechosderivados de los actos y contratos de mutuoentre particulares.•For Assigment of rights resultingfrom the acts and contractsby mutual between individuals.

•Por Contratos de mutuo entreparticulares, con garantíaprendaría o hipotecaria.•For Contracts by mutual betweenindividuals, with collateral or mortgage.

•Por Modificación a EscriturasConstitutivas de Sociedades.•For Modifications to Corporate Deeds.

•Por Disolución y Liquidaciónde Sociedades.•For Termination and Liquidationof Business Partnerships.

•Por Aumentos de Capital de Sociedades Civiles y Mercantiles.•For Capital Increases in Partnershipsand Corporations.

•Por Fusión de SociedadesCiviles y Mercantiles.•For Merging Partnerships and Corporations.

•Por Constitución de SociedadesCiviles y Mercantiles.•For Constitution of Partnershipsand Corporations.

•Por la Adquisicion de VehículosAutomotores Usados.•For Acquisition of Used Motor Vehicles.

•Por Rectificaciones o ratificacionesde cualquier acto o contrato.•Por Rectification or ratificationof any legal acts or contracts.

TASA ó TARIFARATE OR TARIFF

Un día de salariomínimo generalde la zona,por cada otorgante.One day’s general minimumwage in the area,per grantor.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

Un día de salario mínimo general de la zona, por foja.One day’s general minimumwage in the area, per page.

Un día de salariomínimo generalen la zona,por cada una.One day’s generalminimum wage in thearea, for each.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

1.5 %1.5 %

Un día de salariomínimo general de la zona por foja. One day’s general minimumwage in the area, per page.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre cada otorgante.Based on each grantor.

Sobre el monto de los actosjurídicos y con garantíaprendaría o hipotecaria.Based on the legal actswith collateral and mortgage.

Sobre el importe del contrato.Based on the amount of the contract.

Sobre el número de fojasdel documento donde constela modificación.Based on the number of pagesof the document holding suchmodifications.

Sobre el número de fojasdel instrumento.Based on the number ofpages of the document.

Sobre el importe del capitalaumentado.Based on the amount ofcapital increase.

Sobre la diferencia entreel capital social de la fusionante,antes y después de la fusión.Based on the difference in capitalstock of the merging companybefore and after the merge.

Sobre el capital de la sociedad.Based on the capital of the company.

Sobre el valor de la facturase aplicará el factor señaladoen el Art. 6° de acuerdoal año de antigüedadde la unidad y se obtendrála base del impuesto. 1_/Based on the value of the invoicein accordance withArticle 6 and considering the ageof the vehicle. 1_/

Sobre cada foja.Based on each page.

San Luis Potosí. Sistema Fiscal Estatal y MunicipalSan Luis Potosí. State and Municipal Tax System

4_/ Son sujetos de este impuesto, las personas físicas o morales, o unidades económicas sin personalidad jurídica, que obtengan premios en efectivo o en especie, derivados de la celebración de rifas, sorteos, loterías, apuestas y concursos de toda clase, así como juegos con máquinas de sistemas, programas autorizados o computarizados, aún cuando por dichos eventos no se cobre cantidad alguna que represente el derecho a participar en los mismos.5_/ Con excepción de las erogaciones a que se refiere el artículo 27, de la Ley de Hacienda para el Estado de San Luis Potosí.6_/ El impuesto se aplicará sin incluir alimentos, demás servicios relacionados y el impuesto al valor agregado. Para estos efectos, el prestador del servicio de hospedaje, deberá realizar el desglose correspondiente en el comprobante fiscal que expida.

4_/ This tax applies to individuals or legal entities or businesses without legal status who obtain prizes whether in cash or in kind arising from raffles, drawings, lotteries betting and contests of any type as well as automated or computerized gaming programs or systems including cases where no fees are required for participation in such events. 5_/ Except expenses set forth in Article 27, of the Tax Law of the State of San Luis Potosi. 6_/ Tax does not include food and related services and added value tax. The provider of lodging services shall break down amounts on invoices.

CONTINUACIóN122 www.sdeslp.gob.mx

San Luis Potosí. Sistema �scal estatal y municipalSan Luis Potosí. State and municipal tax system

7_/ Se entenderá por zona industrial la ubicada entre la carretera 57 y la vía del ferrocarril San Luis-Querétaro, desde el boulevard Antonio Rocha Cordero hasta el acceso a “La Pila”, y la que al efecto establezca los planes de desarrollo urbano aplicables al municipio de San Luis Potosí.8_/ No causarán el impuesto, previa autorización del Cabildo, los predios rústicos cuando por factores climatológicos y otros ajenos a la voluntad de los productores se haya originado la pérdida total de la producción.

7_/ Industrial zone refers to the area between Highway 57 and SLP-Queretaro railroad track, from Antonio Rocha Cordero Blvd up to access road to La Pila, including any future urban development plans applicable tothe municipality of San Luis Potosi. 8_/ Tax shall not apply, subject to prior authorization from the Government Council, to rural land when climatic and other involuntary factors are the cause of total loss of production.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.Sobre valor catastral del predio.Based on cadastral value of the property.

TASA ó TARIFARATE OR TARIFF

0.540 al millar anual..54 to 1,000 yearly.

0.9650 al millar anual..965 to 1,000 yearly.

0.9650 al millar anual..965 to 1,000 yearly.

1.0815 al millar anual.1.0815 to 1,000 yearly.2.0000 al millar anual.2 to 1,000 yearly.

1.2800 al millar anual.1.28 to 1,000 yearly.

1.5450 al millar anual.1.545 to 1,000 yearly.

1.5450 al millar anual.1.545 to 1,000 yearly.1.0300 al millar anual.1.03 to 1,000 yearly.

CONCEPTOCONCEPT

MUNICIPIO DE SAN LUIS POTOSÍ:MUNCIPALITY OF SAN LUIS POTOSI:1.Predial.1.Real-estate.

a) Urbanos y suburbanoshabitacionales:a) Urban and suburban housing:

• Predios con edificación tipificadacomo de interés social o viviendapopular y popular con urbanizaciónprogresiva.• Land with construction classifiedas social or popular housing withprogressive urbanization.

• Predios con edificación distintosa los del inciso anterior.• Land with construction otherthan in the previous item.

• Predios sin edificación, bardeadoso cercados con malla y limpios.• Land with no construction,walled or wire-fenced and clean.b) Urbanos y suburbanos destinadosa comercios, servicios u o�cinas:b) Land for urban or suburbancommerce, services or of�ces:• Predios con edificación.• Land with construction.• Predios sin edificación bardeadoso cercados con malla y limpios.• Land with no construction;walled or wire-fenced and clean.c) Urbanos y suburbanos destinadosa uso industrial:c) Urban and suburban land destinedfor industrial use:•Predios ubicados en la zonaindustrial. 7_/• Land located in theindustrial zone. 7_/• Predios ubicados fuerade la zona industrial.•Land located outside theindustrial zone.d) Predios rústicos:d) Rural land:• Predios de propiedad privada.•Private property.• Predios de propiedad ejidal. 8_/•Communal property. 8_/

7_/ Se entenderá por zona industrial la ubicada entre la carretera 57 y la vía del ferrocarril San Luis-Querétaro, desde el boulevard Antonio Rocha Cordero hasta el acceso a “La Pila”, y la que al efecto establezca los planes de desarrollo urbano aplicables al municipio de San Luis Potosí.8_/ No causarán el impuesto, previa autorización del Cabildo, los predios rústicos cuando por factores climatológicos y otros ajenos a la voluntad de los productores se haya originado la pérdida total de la producción.

7_/ Industrial zone refers to the area between Highway 57 and SLP-Queretaro railroad track, from Antonio Rocha Cordero Blvd up to access road to La Pila, including any future urban development plans applicable to the municipality of San Luis Potosi. 8_/ Tax shall not apply, subject to prior authorization from the Government Council, to rural land when climatic and other involuntary factors are the cause of total loss of production.

Fuente: Ley de Hacienda para el Estado de San Luis Potosí, Periódico O�cial del Gobierno del Estado Libre y Soberano de San Luis Potosí última Reformapublicada el 19 de Diciembre de 2009; Ley de Ingresos del Municipio de San Luis Potosí, S.L.P. Periódico O�cial del Gobierno del Estado de San Luis Potosí,30 de Diciembre de 2010; y Prontuario Fiscal Cengage 2011 Correlacionado. www.sat.gob.mx.

Source: Finance Law for the State of San Luis Potosi, Official Newspaper of the Government of the Free and Sovereign State of San Luis Potosi last reform publishedDecember 19, 2009; State Revenue Act of San Luis Potosi, S.L.P. Official Newspaper of the Government of the State of San Luis Potosi, December 30, 2010; and fiscalhandbook, Prontuario Fiscal Cengage 2011. www.sat.gob.mx.

4.0000 al millar anual.4 to 1,000 yearly .

1.0000 al millar anual.1 to 1,000 yearly.

1.60 %1.60 %

4.0 %4.0%

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor catastral del predio.Based on cadastral value of the property.

Sobre valor del inmueble(predio y edi�cación).Based on real-estate value(land and construction).

Se causara aplicando a la base gravableestablecida por la Ley de Hacienda paralos Municipios de San Luis Potosí, lastasas señaladas por esta Ley en materiade impuesto predial.Based on the tax base set forth in the Finance Law for the Munipalitiesof San Luis Potosi, regarding property tax .

Sobre el ingreso que se perciba, diaria omensualmente, en razón del número de unidades vendidas por cuota de admisión,boletos, tarjetas, abonos u otrossemejantes que den acceso alespectáculo de que se trate.Based on daily or monthly income, dependingon the number of units sold per admission fees,tickets, cards, subscription or the likerendering access to any such event.

e) Predios Urbanos y suburbanos sinedi�cación, sin bardear o sin cercado con malla.e) Urban and suburban land withno construction, no wallor wire-fencing.

f) Instituciones religiosas.f) Religious institutions.

2. Adquisición de Inmueblesy Otros Derechos Reales.2. Acquisition of Real-Estateand Other Real Rights.

a) Por la adquisición de inmuebles.a) By the acquisition of real-estate.

3. De Plusvalía.3. Added value.

• De Plusvalía.• Added value .

• Espectáculos Públicos.• Public Entertainment .

4. Espectáculos Públicos.4. Public Entertainment .

Fuente: Ley de Hacienda para el Estado de San Luis Potosí, Periódico

Oficial del Gobierno del Estado Libre y Soberano

de San Luis Potosí última Reforma publicada el 19

de Diciembre de 2009; Ley de Ingresos del Municipio

de San Luis Potosí, S.L.P. Periódico Oficial del

Gobierno del Estado de San Luis Potosí, 30 de Diciembre de 2010; y

Prontuario Fiscal Cengage 2011 Correlacionado.

www.sat.gob.mx.

Source: Finance Law for the State of San Luis

Potosi, Official Newspaper of the

Government of the Free and Sovereign State of

San Luis Potosi last reform published December 19, 2009; State Revenue Act of San Luis Potosi, S.L.P.

Official Newspaper of the Government of the State of San Luis Potosi, December

30, 2010; and fiscal handbook, Prontuario

Fiscal Cengage 2011. www.sat.gob.mx.

1_/ Los vehículos con antigüedad mayor de diez años y hasta veinte pagarán únicamente el equivalente a tres días de salario mínimo general vigente en el Estado. Quedan exceptuados del pago de este impuesto la Federación, el Estado, los municipios y sus respectivos organismos descentralizados. Artículo 6° de la Ley de Hacienda para el Estado.

1_/ vehicles over 10 years and up to 20 pay only the equivalent of three days of minimum wage in force in the State. Exempt from this tax are the Federation, State, municipalities and their respective decentralized agencies. Article 6 of the Finance Act for the State.

ESTATALES / STATE

CONCEPTOCONCEPT

•Por Otorgamiento,sustitución, renunciao renovación de poderes.•For granting, substitution, waiveror renewal of powers.

•Por Cesión de los derechosderivados de los actos y contratos de mutuoentre particulares.•For Assigment of rights resultingfrom the acts and contractsby mutual between individuals.

•Por Contratos de mutuo entreparticulares, con garantíaprendaría o hipotecaria.•For Contracts by mutual betweenindividuals, with collateral or mortgage.

•Por Modificación a EscriturasConstitutivas de Sociedades.•For Modifications to Corporate Deeds.

•Por Disolución y Liquidaciónde Sociedades.•For Termination and Liquidationof Business Partnerships.

•Por Aumentos de Capital de Sociedades Civiles y Mercantiles.•For Capital Increases in Partnershipsand Corporations.

•Por Fusión de SociedadesCiviles y Mercantiles.•For Merging Partnerships and Corporations.

•Por Constitución de SociedadesCiviles y Mercantiles.•For Constitution of Partnershipsand Corporations.

•Por la Adquisicion de VehículosAutomotores Usados.•For Acquisition of Used Motor Vehicles.

•Por Rectificaciones o ratificacionesde cualquier acto o contrato.•Por Rectification or ratificationof any legal acts or contracts.

TASA ó TARIFARATE OR TARIFF

Un día de salariomínimo generalde la zona,por cada otorgante.One day’s general minimumwage in the area,per grantor.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

Un día de salario mínimo general de la zona, por foja.One day’s general minimumwage in the area, per page.

Un día de salariomínimo generalen la zona,por cada una.One day’s generalminimum wage in thearea, for each.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

3 al millar.3 to 1,000.

1.5 %1.5 %

Un día de salariomínimo general de la zona por foja. One day’s general minimumwage in the area, per page.

BASE DE CALCULOBASIS FOR CALCULATION

Sobre cada otorgante.Based on each grantor.

Sobre el monto de los actosjurídicos y con garantíaprendaría o hipotecaria.Based on the legal actswith collateral and mortgage.

Sobre el importe del contrato.Based on the amount of the contract.

Sobre el número de fojasdel documento donde constela modificación.Based on the number of pagesof the document holding suchmodifications.

Sobre el número de fojasdel instrumento.Based on the number ofpages of the document.

Sobre el importe del capitalaumentado.Based on the amount ofcapital increase.

Sobre la diferencia entreel capital social de la fusionante,antes y después de la fusión.Based on the difference in capitalstock of the merging companybefore and after the merge.

Sobre el capital de la sociedad.Based on the capital of the company.

Sobre el valor de la facturase aplicará el factor señaladoen el Art. 6° de acuerdoal año de antigüedadde la unidad y se obtendrála base del impuesto. 1_/Based on the value of the invoicein accordance withArticle 6 and considering the ageof the vehicle. 1_/

Sobre cada foja.Based on each page.

San Luis Potosí. Sistema Fiscal Estatal y MunicipalSan Luis Potosí. State and Municipal Tax SystemCONCLUSIóN

BUSINESS GUIDE 2011 123