revista espacios - vol. 38 (nº 29) año 2017. pág. …issn 0798 1015 home revista espacios !...

TRANSCRIPT

ISSN 0798 1015

HOME Revista ESPACIOS ! ÍNDICES ! A LOS AUTORES !

Vol. 38 (Nº 29) Año 2017. Pág. 33

The current state of the credit marketof the Republic of KazakhstanEl estado actual del mercado crediticio de la República deKazajstánMakpal Tokanovna ZHOLAMANOVA 1; Aktolkyn Turlukanovna KULSARIYEVA 2; AssylbekOrinshaikhovitch BAZARBAYEV 3; Raigul Dukenbaykyzy DOSZHAN 4

Recibido: 08/01/2017 • Aprobado: 09/02/2017

ABSTRACT:In the state of the national address "Kazakhstan in aNew Global Reality: Growth. Reforms. Development"delivered on November 30, 2015, the PresidentNursultan Nazarbayev defined one of the five directionsof anti-crisis and structural reforms - stabilization of thefinancial sector. The research shows the growingdynamics of loans provided by banks to customers.There were also calculated volumes of long-term andshort-term loans, the volume of loans to legal entitiesand credit activity of the banks. Key words credit market, the Republic of Kazakhstan,financial system, banking sector, loans

RESUMEN:En "Kazajstán en una Nueva Realidad Global:Crecimiento, Reformas y Desarrollo", presentado el 30de noviembre de 2015, por el presidente NursultanNazarbayev éste definió que una de las cincodirecciones de las reformas anti-crisis y estructuralesera la estabilización de la economía financiera y lareforma del sector. La investigación muestra la crecientedinámica de los préstamos otorgados por los bancos alos clientes. También se han calculado volúmenes depréstamos a largo y corto plazo, volumen de préstamosa entidades jurídicas y actividad crediticia de losbancos. Palabras claves Mercado crediticio, República deKazajstán, sistema financiero, sector bancario,préstamos

The President of the Republic of Kazakhstan Nursultan Nazarbayev defined the direction ofreforms: "Our most important task is to quickly stabilize the financial system, bring it in linewith the new global reality. First, it is necessary to ensure the effective functioning of thefinancial sector in conditions of a floating exchange rate of tenge. The principal point is thatthere will not be a return to the practice of the endless maintenance of the national currency atthe expense of the National Fund. The National Bank needs to conduct stress testing of allsubjects of the banking sector for non-performing loans. According to its results, it is necessaryto take measures to recognize them and write-off them. Banks that failed to solve the problemof capitalization must "leave" the financial system. Kazakhstan banks must comply with allinternational standards, including the Basel Committee and the International Monetary Fund. Itis important to build confidence in the national currency through the expansion of instrumentsof "de-dollarization" (State of the Nation Address by President of Kazakhstan Nursultan

Nazarbayev.., 2015).- Quickly stabilize the financial system, bring it into line with the new global reality;- It is necessary to ensure the effective functioning of the financial sector in conditions of afloating exchange rate of tenge. The principal point is that there will not be a return to thepractice of maintaining the national currency rate at the expense of the National Fund;- The National Bank should reduce the level of inflation to 4% in the medium term;- The National Bank needs to conduct stress testing of all subjects of the banking sector fornon-performing loans. Based on its results, measures should be taken to recognize them andwrite-off them;- The National Bank should regularly provide the society and financial institutions withcomprehensive information on its activities;- Banks that failed to solve the problem of capitalization must leave the financial system.Kazakhstani banks must comply with all international standards, including the Basel Committeeof the International Monetary Fund;- The Unified Pension Fund, the Problem Loan Fund and other financial institutions should beremoved from the control of the National Bank;- The use of the National Fund for current expenses should be discontinued. The onlymechanism for the National Fund's participation is an annual fixed transfer to the nationalbudget.In general, 7.5 trillion tenge is allocated for the implementation of projects of the state of thenational address (State of the Nation Address by President of Kazakhstan NursultanNazarbayev.., 2015).One of the main functions of banks is lending to the economy. Bank credit is the most commonform of credit relations in the economy. Currently, the main risk factors for banks associatedwith lending to the population are general economic shocks that could lead to a decrease in thesolvency of the population, a decline in property prices and the instability of exchange rates. Asfor the corporate sector, the risks here are primarily due to the high proportion of loans directedto the economy, whose businesses, in the event of a decline in business activity, are moremobile, which could lead to increased bankruptcies and a deterioration in the quality of the loanportfolio. Because a slowdown in the growth of the economy may lead to a decrease in theability of borrowers to repay loans, it is necessary for banks to reorient lending from thebranches of trade and real estate in the manufacturing, transport, and agricultural industries.In the current situation, one of the most successful opportunities for reaching a fundamentallynew level of business and gaining competitive advantages for banks is the creation of abalanced analytical system for managing financial flows (Money, credit, banks, 2006).In the structure of aggregate assets of the banking sector of the Republic of Kazakhstan (Table1), overall, the positive dynamics of development is observed: the assets of credit organizationsincreased by 30.4% to KZT 23,784.4 billion as of January 1, 2016, by 18.0% - up toKZT18,239.00 billion as of 01.01.2015. In the structure of assets, the largest share (60.6%) isoccupied by the loan portfolio (principal debt) in the amount of KZT15,553.7 billion (at thebeginning of 2015 - 14 184,4 billion tenge), increase for 2015 is 9,7%.In general, the banking sector of Kazakhstan functions in equal competitive conditions. Theshare of the loan portfolio in assets of 60-70% is most likely to be optimal for maintainingnormal banking activity in Kazakhstan.

Table 1. Structure of total assets of the banking sector of the Republic of KazakhstanBillion tenge

Indicator /date

2013 2014Growth,

2015Growth,

billiontenge

In % oftotal

billiontenge

In % oftotal

in% to2013

billiontenge

In % oftotal

in% to2014

Cash, refinedpreciousmetals andcorrespondentaccounts

1 953,6 9,5% 2 446,7 10,9% 25,2% 3 969,2 15,5% 62,2%

Depositsplaced withother banks

465,0 2,3% 382,3 1,7% -0,8% 692,0 2,7% 81,0%

Securities 1 916,6 9,3% 2 075,4 9,3% 8,3% 56,3 0,2% -97,3%

Bank loansand reverserepurchasetransactions

13 348,2 64,6% 14 184,4 63,4% 6,3% 15 553,7 60,6% 9,7%

Investments incapital

351,7 1,7% 486,9 2,2% 38,4% 479,3 1,9% -1,6%

Other assets 2 623,8 12,7% 2794,0 12,5% 0,6% 4 908,2 19,1% 75,7%

Total assets(excludingprovisions(provisions)

20 659,0 100,0% 22 369,7 100,0% 8,3% 25 658,7 100,0% 14,7%

Provisions(provisions) inaccordancewith IFRS,including:

-5 197,3 -25,2% -4 130,7 -18,5% -20,5% -1 874,3 -7,3% -54,6%

Provisions(provisions)forcorrespondentaccounts anddeposits withother banks

-3,6 0,0% -1,9 0,0% -0,5% -0,1 0,0% -94,6%

Provisions(provisions)for securities

-54,9 -0,3% -63,8 -0,3% -83,8% -10,3 0,0% -83,9%

Provisions(provisions)for bank loans

-4 643,9 -22,5% -3 569,8 -16,0% -23,1% -1 642,4 -6,4% -54,0%

and operations"ReverseREPO"

Provisions(provisions)for coveringlosses oninvestments insubsidiariesand associates

-116,0 -0,6% -123,1 -0,6% 0,6% -175,8 -0,7% 42,8%

Provisions(provisions)for otherbankingactivities andreceivables

-378,9 -1,8% -372,2 -1,7% -0,2% -45,8 -0,2% -87,7%

Total assets 15 461,7 18 239,0 18,0% 23 784,4 30,4%

Note: Compiled from the National Bank of the Republic of Kazakhstan (The official website of the NationalBank of the Republic of Kazakhstan)

Consider the dynamics of assets and loan portfolio of the banking sector of the Republic ofKazakhstan for the period from 2013 to 2015. The dynamics of assets and loan portfolio of thebanking sector of the Republic of Kazakhstan as of 01.01.2016 (figure) are as follows:

Figure 1. Dynamics of assets and loan portfolio of the banking sector of the Republic of Kazakhstan

In accordance with Figure 1, a slight increase in the loan portfolio in banks' assets can benoted, as on 01.01.2014 the share of the loan portfolio in assets was 86.3%, as of 01.01.2015- 77.8%, as of 01.01.2016 - 65.4%. In 2015, a relatively large increase in assets was due toother items: cash, refined precious metals and correspondent accounts (an increase of 62.2%);Deposits placed with other banks (an increase of 81.0%). Thus, for the period 2013 – 2014there was a change in the structure of assets of the banking sector of the Republic ofKazakhstan, not in favor of the loan portfolio.The content of the loan portfolio depends on the liquidity and profitability of banks, and their

very existence. In 2015, lending was quite stable, even with a certain growth, so the growth inthe loan portfolio in 2015 was 9.7% versus 2014.

Table 2. Structure of the loan portfolio of the banking sector of the RK for the period 2013-2015.Billion tenge

Indicator /date

2013 2014Growth,%to 2013

2015Growth,%to 2014billion

tengeIn % oftotal

billiontenge

In % oftotal

billiontenge

In % oftotal

Carryingamount ofloansincluding:

14 582,5 100,0% 15 357,7 100,0% 5,4% 16 711,3 100,0% 8,8%

Main debt 13 348,2 91,5% 14 184,4 92,4% 6,3% 15 553,7 93,1% 9,7%

Discount,premium

-47,7 -0,3% -37,0 -0,2% -22,4% -14,0 -0,1% -62,0%

Accruedcompensation

1 282,0 8,8% 1 212,3 7,9% -5,4% 1 174,6 7,0% -3,1%

Positive /NegativeAdjustment

0,1 0,0% -2,0 0,0% -20% -2,9 0,0% 45%

IFRSProvisions

4 643,9 31,8% 3 569,8 23,2% -23,1% 1 642,4 9,8% -54,0%

The carryingamount ofloans, net ofprovisions(net value ofloans)

9 938,6 68,2% 11 787,9 76,8% 18,6% 15 069,0 90,2% 27,8%

Loan portfolio(main debt),including:

13 348,2 100,0% 14184,4 100,0% 6,3% 15 553,7 100,0% 9,7%

Loans tobanks andorganizationsengaged incertain typesof bankingoperations

121,1 0,9% 102,1 0,7% -15,7 62,2 0,3% -39,1%

Loans to legalentities

7 666,0 57,5% 8 091,0 57,1% 5,5% 8 511,0 54,8% 5,2%

Loans toindividuals

3 626,0 27,1% 4 015,0 28,2% 10,7% 4 163,0 26,8% 3,7%

Loans tosmall andmedium-sizedenterprises(residents ofthe RepublicofKazakhstan)

1 283,0 9,7% 1 788,0

12,6% 39,4% 2 060,0

13,3% 15,2%

Other loans 537,8 3,9% 78,8 0,6% -85,3% 688,2 4,4% 873,3%

Reverse repotransactions

114,3 0,9% 109,5 0,8% -4,2% 69,3 0,4% -36,7%

Note: Compiled from the National Bank of the Republic of Kazakhstan (The official website of the NationalBank of the Republic of Kazakhstan)

According to Table 2, the volume of the loan portfolio of borrowers in the Republic ofKazakhstan is equal to KZT15,553.7 billion, which exceeds the volumes of 2013 by 16.5%(KZT845.0 billion), in 2014 by 9.7% (420, 0 billion KZT).Crediting of legal entities in the amount of 54.8% in 2015 continues to lead in the total volumeof the loan portfolio of the Republic of Kazakhstan. Loans to legal entities in 2015 increased by5.2% and amounted to KZT 8,511.0 billion (in 2013 - KZT 7,666.0 billion or 57.5% of the loanportfolio, in 2014 - 8,091 , 0 billion tenge or 57.1% of the loan portfolio).Loans to individuals amount to KZT4,163.0 billion with a 26.8% share of the loan portfolio (atthe beginning of 2015 - KZT4,015.0 billion or 28.2% of the loan portfolio). The growth of loansto individuals in 2015 was 3.7%, less than in 2014 - 10.7%.By the subjects of small and medium-sized businesses, there was a tendency for an annualincrease in the volume of issued loans. For the needs of the subjects of this direction, aboutKZT 2,060 billion was granted in 2015, which is 15.2% higher than the previous year's figure(KZT1,788.0 billion). By volume of crediting, small and medium-sized business occupies 13.3%of the loan portfolio of the banking sector of the Republic of Kazakhstan. A very large increaseis observed in 2014 - 39.4%.In connection with the concern over the quality of the loan portfolio, Kazakh banks tightenedtheir credit policy in 2015. Restraint of banks in lending is explained by low availability ofliquidity and high credit risk. According to the estimates of banks, the additional factors thatcontributed to the tightening of the credit policy are the economic uncertainty in the country,the risk of deterioration in the cost of collateral, and fears of deterioration in the risk profile ofborrowers.

Figure 2. Dynamics of the loan portfolio of the banking sector of the Republic of Kazakhstan for 2013-2015 (The official website of the National Bank of the Republic of Kazakhstan)

From 2013 to 2015, the prevailing type of active operations in commercial banks is the lendingof legal entities from 57.5% to 54.8% in the loan portfolio. Also in the loan portfolio of thebanking sector as of 01.01.2016, a high proportion of loans accounted for loans to individuals -26.8%. There is a tendency to increase the demand for consumer lending. Consumer lendingpermits the needs of the population in necessary items and equipment in installments.

Table 2. Credits of second-tier banks of Kazakhstan for 2011-2015.billion tenge

Credits to the economy of Kazakhstan, including

Total

by currency type by date on subjects of crediting

In nationalcurrency

In foreigncurrency

Short-term

Long-term Non-banklegalentities

Individuals

2012 11 623 8 393 3 230 2 486 9 137 8 448 3 175

2013 13 348 9 633 3 715 3 102 10 246 9 398 3 950

Growth,% 14,8% 14,8% 15,0% 24,8% 12,1% 11,2% 24,4%

2014 14 184 10 124 4 060 3 179 11 005 9 860 4 324

Growth,% 6,3% 5,1% 9,3% 2,5% 7,4% 4,9% 9,5%

2015 15 554 10 608 4 946 3 365 12 189 11 108 4 446

Growth,% 9,7% 4,8% 21,8% 5,8% 10,8% 12,7% 2,8%

Note: Compiled from the National Bank of the Republic of Kazakhstan (The official website of the NationalBank of the Republic of Kazakhstan)

As of January 2016, the following situation was observed in the credit market of Kazakhstan. Asa result of 2015, the volume of loans reached KZT15,554 billion, having increased by 9.7%compared to 2014, and by 16.5% since 2013. In general, the data in Table 3 confirm that thecredit activity of Kazakhstan's economy is growing. The loan portfolio as of the end of 2013amounted to KZT13,348 billion, having increased by KZT1,725 billion or by 14.8% compared tothe beginning of the year. The growth in 2014 was insignificant - 6.3%, decreased by 8.5%compared to 2013. In 2015 - 9.7% there is an increase in comparison with 2014, but thisindicator is lower than the increase in 2013 (14.8%) by 5.1% (Table 2).

Figure 3. Credits to the economy of Kazakhstan (by types of currencies)

Loans in national currency from 2013 to 2015 tend to increase in nominal terms (Table 2), butin terms of growth there is a decrease from 14.8% (9 633 billion tenge) in 2013 to 4.8% (10608 billion KZT) in 2015. But for the same period there is an outstripping growth in loans inforeign currency. Increased from 15.0% (KZT3,715 billion) to 21.8% (KZT4,946 billion) in 2015(Table 2, Figure 3).In the total volume of loans for 2013, the share of loans in the national currency - 9 633 billiontenge was - 72.2%, in foreign currency - 3,715 billion tenge - 27.8%; For the year 2014 theshare of loans in the national currency - KZT10,124 billion was - 71.4%, in foreign currency -KZT4,060 billion - 28.6%; For 2015, the share of loans in the national currency amounted to 10608 billion tenge - 68.2%, in foreign currency 4 946 billion tenge - 31.8%. As a result, theshare of loans in national currency decreased from 72.2% in 2013 to 68.2% by the end of2015, while in foreign currency it increased from 27.8% in 2013 to 31.8% in 2015 (Figure 3).The transition to a freely floating exchange rate led to a weakening of the tenge. Thedevaluation is predetermined by the decision of the National Bank of Kazakhstan to stopsupporting the exchange rate of the tenge, the country is unable to maintain its currency, thatis, to keep the tenge rate at the expense of state subsidies. This measure also became areaction to the reduction of the cost of oil on the world market. The floating exchange rateshould correspond to the economic situation in the world. This will allow the state budget notjust to save money on keeping its own currency, but also to replenish the state budget. Inconnection with the current economic situation in 2015, Kazakhstan banks tightened their creditpolicy, which is dictated by low liquidity availability and high credit risk.As we see, the issuance of loans in tenge is not entirely beneficial to second-tier banks. But thistrend is influenced by state support for lending, which is implemented through state programsof industrial and innovative development of the state, programs for supporting small andmedium-sized businesses, agricultural development programs, etc. Lending to the economythrough state-owned resources through second-tier banks is made in national currency.Analysis of the country's credit market by types of currencies is indicative of the upward trendin the share of loans in the national currency, however, the decline in the share of loans inforeign currency is not observed, which is more closely related to the resource base of

commercial banks, which is more formed from deposits in foreign currency, as well as thegrowth of the exchange rate on the market.The growth in the share of loans in foreign currency is associated with an increase in the shareof liabilities in the structure of the resource base, expressed in foreign currency. In theconditions of inflow of deposits mainly in foreign currency, banks, in order to minimize currencyrisks, are also forced to issue loans mainly in foreign currency (Table 2, figure 3).The observed growth of the dollar to the tenge became the main factor influencing the changingsituation in the financial and money market. On the other hand, the growth of the dollar willaffect the rise in price of imports, which, naturally, will affect the price increase.The second-tier banks are practical to ensure their profit on short-term loans due to turnoverwithin one year. In general, short-term loans are directed to the trade sector, as the turnoverand profitability of trade operations are much higher than in the manufacturing sector. Also, theoutstripping growth of long-term loans is mainly due to the increase in the volume of termdeposits and the gradual extension of their terms of attraction.The banking system of Kazakhstan retains a significant number of banks that do not havesufficient funds for long-term lending. The banks 'investments in long-term projects areincreasing, but not at the expense of the banks' own funds. As practice shows, the main sourceof financing for the real sector of the economy, the state itself becomes the source of long-termloans necessary to stimulate the growth of the country's economy.In order to analyze the credit market of the Republic of Kazakhstan, we will consider thestructure of loans issued by second-tier banks in terms of credit terms, which was reflected inTable 2, in Figure 4.As it can be seen from Table 10, from 2013 to 2015, the volume of issued long-term loans ismore than short-term. So in the total volume of loans for 2013, the share of long-term loans -10,246 billion tenge - 76.8%, short-term - 3,102 billion tenge - 23.2%; In 2014, the share oflong-term loans - 11,005 billion tenge of components - 77.6%, short-term loans - KZT 3,179billion - 22.4%; In 2015, the share of long-term loans.

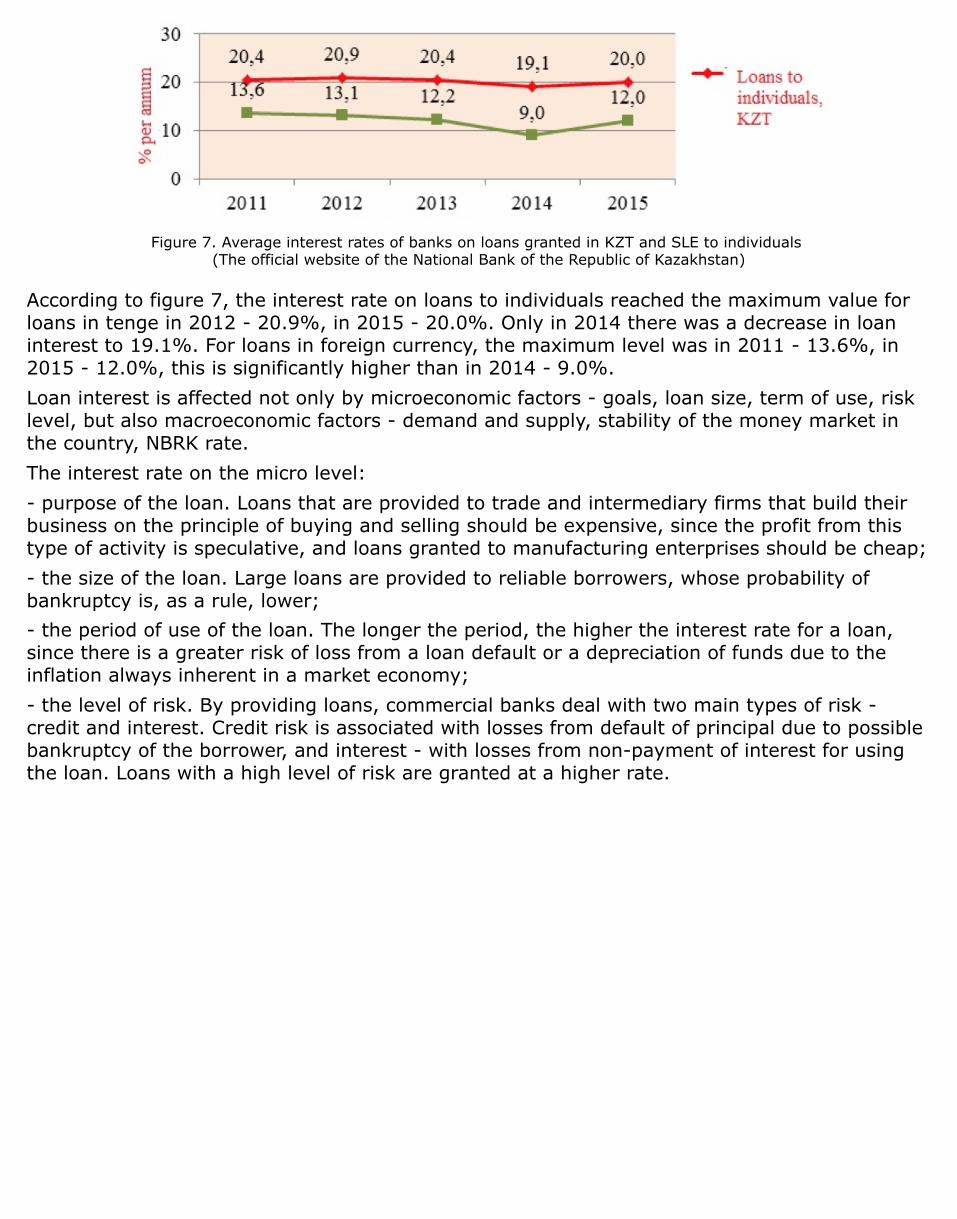

Figure 4. Credits of the peoples of the world (by maturity) (The official website of the National Bank of the Republic of Kazakhstan)

- 12 189 billion tenge was equal to 78.4%, short-term - 3,365 billion tenge - 21.6%, thegrowth trend of long-term loans (Figure 4) continues in comparison with the short-term ones,as a result of which the share of the first until 2015 increased by 10.7% to KZT12,189 billioncompared to 2014 - KZT11,005 billion. The growth of short-term loans for the same periodamounted to 5.8% from KZT3,179 billion in 2014 to KZT3,365 billion in 2015 (Figure 4).

Figure 5. Credits in the euro area (by lending entities) (The official website of the National Bank of the Republic of Kazakhstan)

If we pay attention to the fact that loans are provided for bank loans (Figure 5), then we seethat most of the bank loans are used by non-bank legal entities. In the total volume of loans for2013, the ratio of loans to non-bank legal entities and individuals is: in 2013, 70.4% - 29.6%;In 2014, 69.5% - 30.5%; In 2015, 71.4% - 28.6%. For the period from 2013 to 2014, thevolume of lending to legal entities is increasing. According to Table 3 in 2014, for non-banklegal entities, the growth was 4.9%, which is 6.3% less than the increase in 2013. Only in 2015crediting of legal entities has significantly increased to 11,108 billion tenge, an increase was12.7%. In the period from 2013 to 2015, In nominal terms, the volume of loans issued growsfrom KZT 3,950 billion to KZT4,446 billion, but the growth rate steadily decreases from 24.4%in 2013 to 9.5% in 2014 and to 2.8% in 2015.Currently, according to banks, the current level of credit risk on the retail portfolio is high,which is explained by the instability of the country's economy, the decrease in the solvency ofborrowers and the decrease in consumer demand of the population.According to comparable data on the maturity of loans in 2013-2015, we can conclude that asignificant increase in the volume of long-term loans in comparison with the short-term. This isa positive factor. Corrective impact on the market, as a rule, affects the increase in the volumeof investments directed to production purposes.When considering the credit activity of banks, loan interest plays an important role. It is themain source of profit for banks.In the theory of J.M. Keynes, interest is an autonomous factor, its level is determined by theinteraction of supply and demand for money balances, i.e. Not on all savings, but only on theirmonetary part. In his opinion, interest is a purely monetary phenomenon reflecting the game ofmarket forces in the money market (Tavasiev, 2008).In A. Marshall’s theory, the interest rate is regarded as a factor that leads to a balance in thedesire to invest and save. According to A. Marshall, interest, being the price paid in any marketfor the use of capital, tends to an equilibrium level at which the aggregate demand for capital inthis market at a given rate of interest equals the total capital flowing into the market at thesame rate of interest (Tavasiev, 2008).The policy of the state is important, which manifests itself in regulating the rate of loan interestthrough the discount rate, as well as the provision of credit funds through second-tier banks toregulate the financial market.The main regulator in approving interest rates for second-tier banks, both on deposits and onloans granted, is the discount rate set by the NBRK. The higher the official discount rate, thehigher the cost of loans of second-tier banks and, accordingly, the loans for the ultimateborrower are also more expensive. At the same time, with an increase in the refinancing rate,the rates on deposits of both the population and enterprises also increase.

With a decrease in the official discount rate, the credit resources of the National Bank of theRepublic of Kazakhstan become cheaper, respectively, the second-tier banks reduce the interestrate on loans, which increases the supply in the credit market. There is also a reduction indeposit rates, and the money market may lose some of its funds, which will go to othermarkets in case of more favorable conditions offered on them. Thus, through the policy ofchanging the discount rate, the NBRK regulates the money market and the cost of bank loans.The interest rate depends on the size of the loan. This is because the issuance of large loansincreases the risk of loss of the lender due to the possibility of insolvency of the borrower. Atthe same time, issuing loans to several borrowers reduces price, because excludes thesimultaneous bankruptcy of several borrowers. In this regard, in banks, the interest rate isdifferentiated for small and large loans, depending on the size of the loan.Also, the value of the interest rate depends on the security of the loan. As a rule, rates onunsecured loans are high, since the risk is high. For loans with security, the interest rate islower.Depending on the purpose of using the loan, the interest rate will also be different. Increasedrisk is available to loans issued for the elimination of financial difficulties for the implementationof investment projects.As a market value, the interest rate depends on the demand and supply of money, thedevelopment of the money market, the sources of free money, borrowers of funds (theircreditworthiness, reliability in repayment of borrowed funds) and other factors.Table 12 shows that the interest on loans depends on the timeframe for which the economy isready to take out a loan, so that the demand for credit is divided into short, medium and long-term. The loan interest rate is related to the term of the loans. As we can see, in 2015, not onlythe requirements for the financial position of the borrower, but also interest rates on loans wereraised.The market rate of loan interest is determined by the interaction of supply and demand in thecredit market. With a high interest rate, the capital productivity of the enterprise is relativelylow, the demand decreases accordingly, and the loan offer increases. When the interest ratedecreases, the profitability for the enterprise grows, it makes sense to borrow money. And thepopulation makes a choice in favor of using a loan in order to meet their needs at the expenseof borrowed funds. A decrease in interest rates on loans leads to an increase in demand forcredit. In this connection, the process of changing interest rates on loans will be constantly onthe move.Within the framework of the thesis, we will examine the interest rates of second-tier banks(Table 3) in Kazakhstan for 2011-2015.

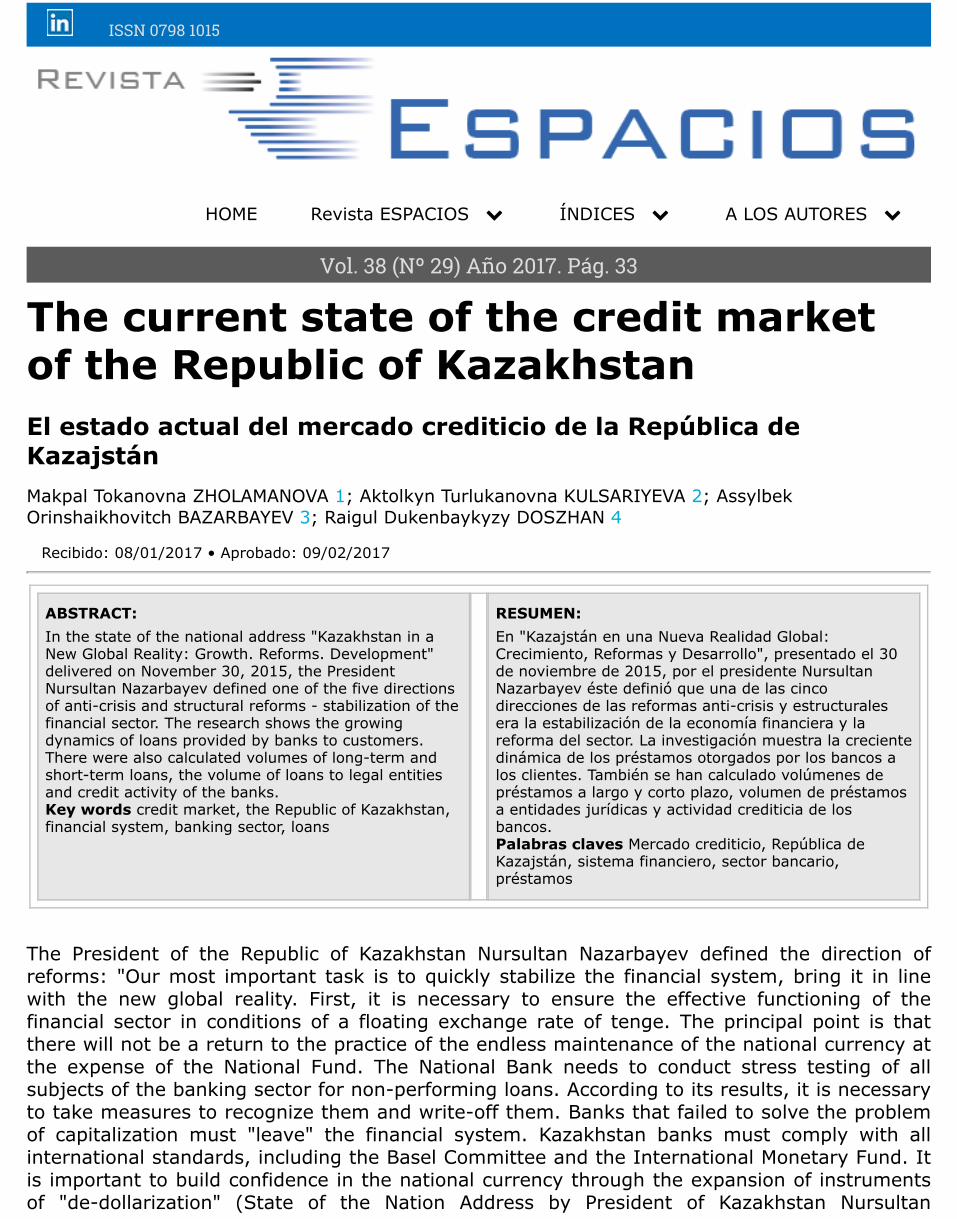

Table 3. Average interest rates of banks on loans granted (by years, by maturities and currencies).

2011 2012 2013 2014 2015

Loans to non-bank legal entities, KZT 11,9 11,0 10,6 10,8 15,7

From 3 months to 1 year, KZT 12,4 11,5 11,0 11,3 14,0

From 1 year to 5 years, KZT 11,6 11,7 11,2 11,1 13,2

Over 5 years, KZT 10,8 10,0 11,2 10,3 10,8

Loans to non-bank legal entities, hard currency 8,8 8,3 7,9 7,8 7,3

From 3 months to 1 year, hard currency 10,2 9,0 7,9 8,1 7,6

From 1 year to 5 years, hard currency 8,0 9,7 10,0 9,6 8,6

Over 5 years, hard currency 8,8 10,0 10,2 8,8 9,0

Loans to individuals, KZT 20,4 20,9 20,4 19,1 20,0

From 3 months to 1 year, KZT 24,4 21,9 19,9 18,8 18,6

From 1 year to 5 years, KZT 22,5 23,3 22,4 20,9 19,0

Over 5 years, KZT 12,9 13,3 14,1 13,7 13,0

Loans to individuals, hard currency 13,6 13,1 12,2 9,0 12,0

From 3 months to 1 year, hard currency 13,5 15,3 12,2 9,0 10,6

From 1 year to 5 years, hard currency 13,4 12,4 11,8 11,0 10,3

Over 5 years, hard currency 13,5 12,5 13,3 12,7 12,2

Note: Compiled from the National Bank of the Republic of Kazakhstan (The official website of the NationalBank of the Republic of Kazakhstan)

In the period that is shown under review, the minimum loan interest is observed in 2013 -10.6%. In 2013, there is a relative rise in the country's economy. The increase in loans grantedreached a maximum size of 14.8% (Table 3). Accordingly, a decrease in loan interestcontributed to an increase in the volume of loans issued. According to figure 6, the interest rateon loans in tenge to non-bank legal entities reached a maximum in 2015 - 15.7%. The increasein demand for loans in tenge by non-bank legal entities enables banks to raise interest rates.Also, the unstable economic situation in the country, the drop in the price of oil and theunstable situation in the world as a whole (the conflict in Ukraine, the depreciation of theRussian ruble, the imposition of sanctions, etc.) led to a significant decrease in the supply ofloans from banks.

Figure 6. Average interest rates of banks on loans extended to KZT and SLE to non-bank legal entities (The official website of the National Bank of the Republic of Kazakhstan)

For loans in foreign currency, the maximum level was in 2011 - 8.8%. From 2011 to 2015,there is a tendency to decrease the loan interest, so the loan interest on loans granted to non-bank legal entities in 2015 amounted to 7.3%.

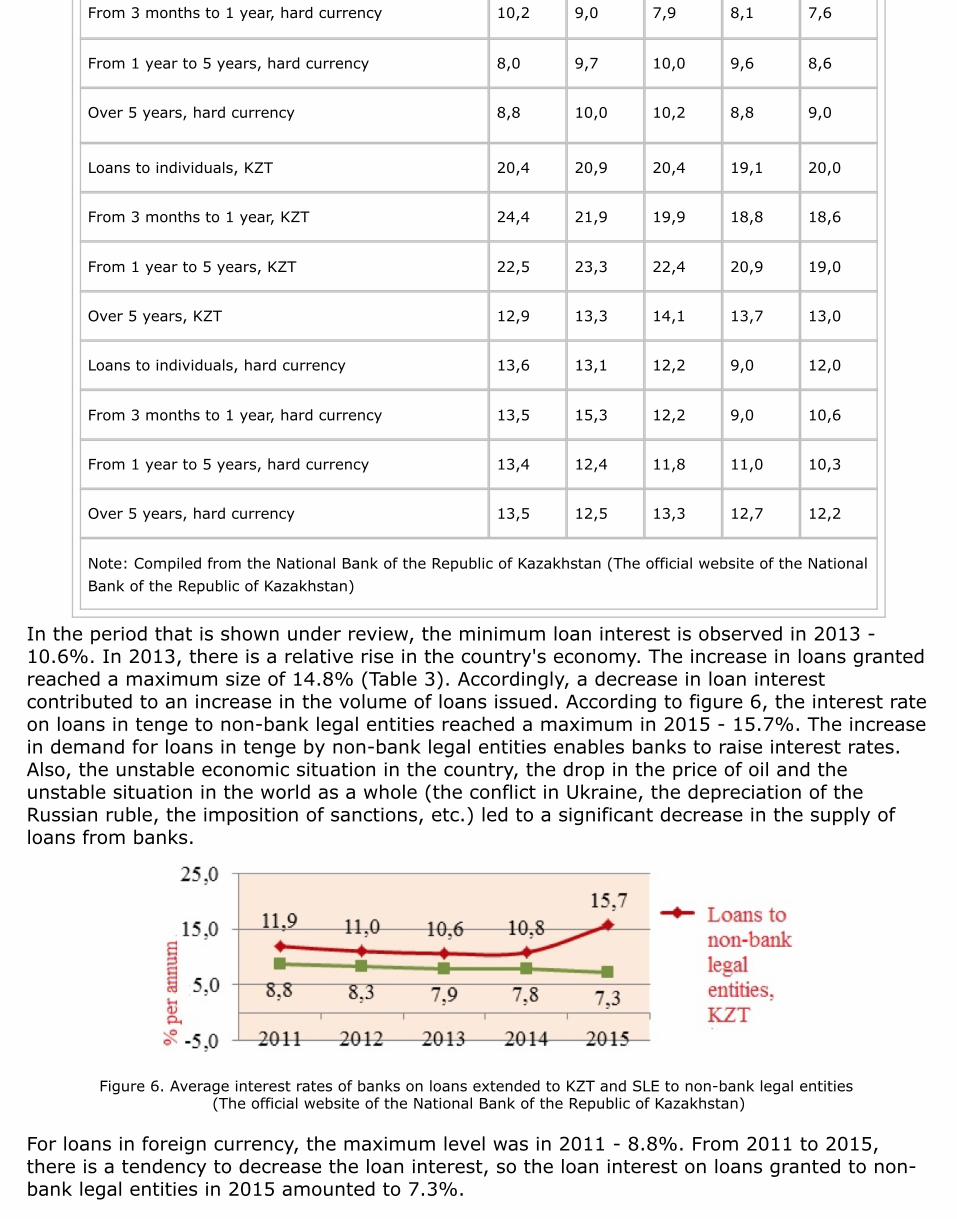

Figure 7. Average interest rates of banks on loans granted in KZT and SLE to individuals (The official website of the National Bank of the Republic of Kazakhstan)

According to figure 7, the interest rate on loans to individuals reached the maximum value forloans in tenge in 2012 - 20.9%, in 2015 - 20.0%. Only in 2014 there was a decrease in loaninterest to 19.1%. For loans in foreign currency, the maximum level was in 2011 - 13.6%, in2015 - 12.0%, this is significantly higher than in 2014 - 9.0%.Loan interest is affected not only by microeconomic factors - goals, loan size, term of use, risklevel, but also macroeconomic factors - demand and supply, stability of the money market inthe country, NBRK rate.The interest rate on the micro level:- purpose of the loan. Loans that are provided to trade and intermediary firms that build theirbusiness on the principle of buying and selling should be expensive, since the profit from thistype of activity is speculative, and loans granted to manufacturing enterprises should be cheap;- the size of the loan. Large loans are provided to reliable borrowers, whose probability ofbankruptcy is, as a rule, lower;- the period of use of the loan. The longer the period, the higher the interest rate for a loan,since there is a greater risk of loss from a loan default or a depreciation of funds due to theinflation always inherent in a market economy;- the level of risk. By providing loans, commercial banks deal with two main types of risk -credit and interest. Credit risk is associated with losses from default of principal due to possiblebankruptcy of the borrower, and interest - with losses from non-payment of interest for usingthe loan. Loans with a high level of risk are granted at a higher rate.

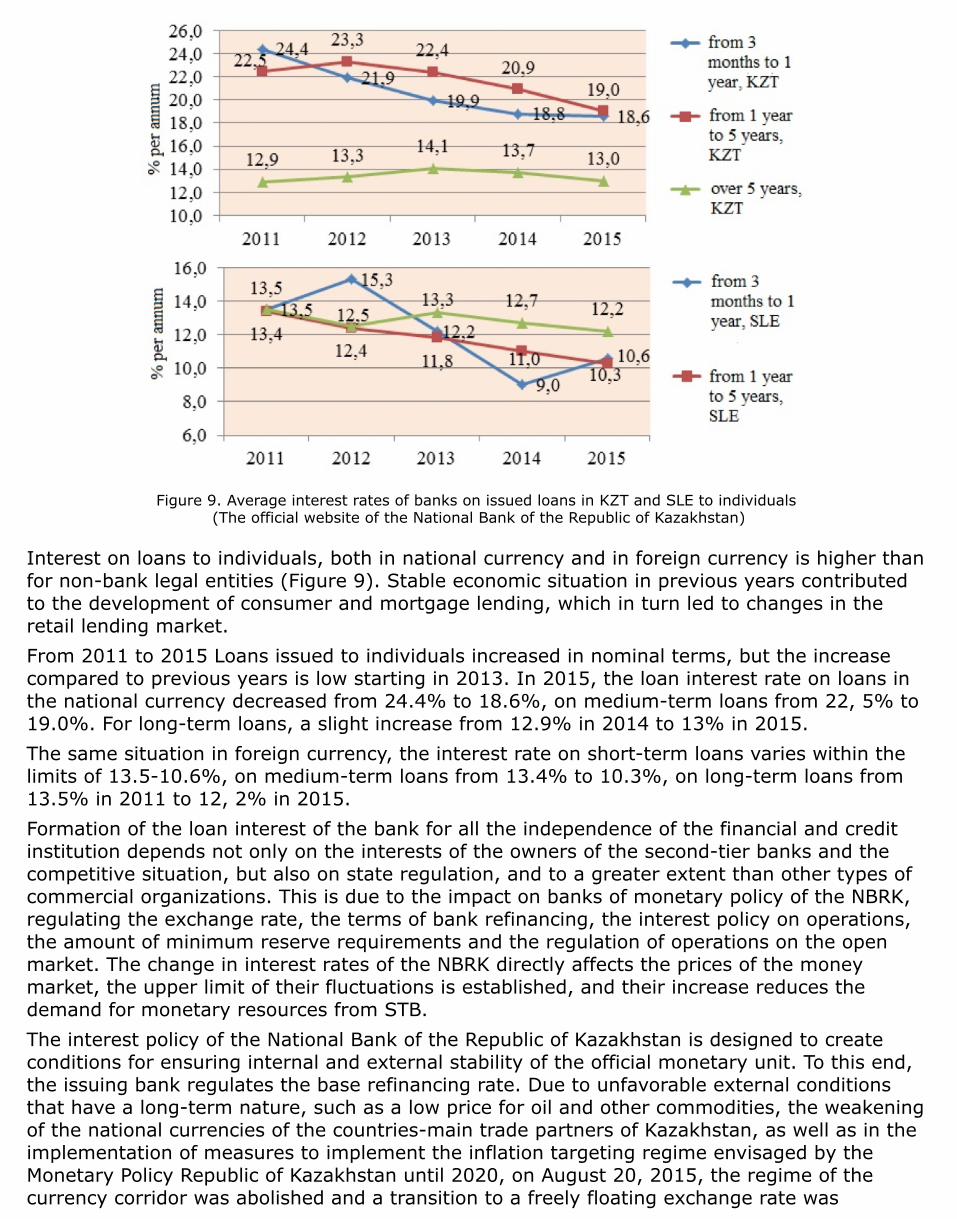

Figure 8. Average interest rates of banks on loans extended to KZT and SLE to non-bank legal entities (The official website of the National Bank of the Republic of Kazakhstan)

Consider the loan interest in terms of currencies for the period from 2011 to 2015 on non-banklegal entities (Figure 8). Interest rates on loans to non-bank legal and natural persons are notstable. In 2011, the weighted average interest rate on short-term loans extended to non-banklegal entities in tenge decreased to 11.0% in 2013.But already in 2015, it reached the maximum size of 14.0%. The loan interest rate of medium-term loans up to 2015 was relatively stable in the range of 11.6-11.1%, in 2015 it increased to13.2%, and demand decreased accordingly. Loan percent of long-term loans for this period isstable. In 2013 interest rates on short-term, medium-term and long-term loans were practicallyleveled to 11.0%, 11.2%.On interest rates for loans in foreign currency, we see a relatively moderate growth in medium-term loans from 8.0% in 2011 to 8.6% in 2015. Interest on long-term loans, respectively, isfrom 8.8% to 9.0%. Rates on short-term loans decreased from 10.2% to 7.3%.As the analysis of figures in Figure 5 shows, there are proposals from banks, but there is nodemand for foreign currency loans, although interest on loans in the national currency is higher.The slowdown in the growth of the segment of foreign currency lending is due to a decrease ininterest in this type of loans. Borrowers do not want to take on the risks of exchange ratefluctuations during the period of uncertainty in the rates of world currencies.

Figure 9. Average interest rates of banks on issued loans in KZT and SLE to individuals (The official website of the National Bank of the Republic of Kazakhstan)

Interest on loans to individuals, both in national currency and in foreign currency is higher thanfor non-bank legal entities (Figure 9). Stable economic situation in previous years contributedto the development of consumer and mortgage lending, which in turn led to changes in theretail lending market.From 2011 to 2015 Loans issued to individuals increased in nominal terms, but the increasecompared to previous years is low starting in 2013. In 2015, the loan interest rate on loans inthe national currency decreased from 24.4% to 18.6%, on medium-term loans from 22, 5% to19.0%. For long-term loans, a slight increase from 12.9% in 2014 to 13% in 2015.The same situation in foreign currency, the interest rate on short-term loans varies within thelimits of 13.5-10.6%, on medium-term loans from 13.4% to 10.3%, on long-term loans from13.5% in 2011 to 12, 2% in 2015.Formation of the loan interest of the bank for all the independence of the financial and creditinstitution depends not only on the interests of the owners of the second-tier banks and thecompetitive situation, but also on state regulation, and to a greater extent than other types ofcommercial organizations. This is due to the impact on banks of monetary policy of the NBRK,regulating the exchange rate, the terms of bank refinancing, the interest policy on operations,the amount of minimum reserve requirements and the regulation of operations on the openmarket. The change in interest rates of the NBRK directly affects the prices of the moneymarket, the upper limit of their fluctuations is established, and their increase reduces thedemand for monetary resources from STB.The interest policy of the National Bank of the Republic of Kazakhstan is designed to createconditions for ensuring internal and external stability of the official monetary unit. To this end,the issuing bank regulates the base refinancing rate. Due to unfavorable external conditionsthat have a long-term nature, such as a low price for oil and other commodities, the weakeningof the national currencies of the countries-main trade partners of Kazakhstan, as well as in theimplementation of measures to implement the inflation targeting regime envisaged by theMonetary Policy Republic of Kazakhstan until 2020, on August 20, 2015, the regime of thecurrency corridor was abolished and a transition to a freely floating exchange rate was

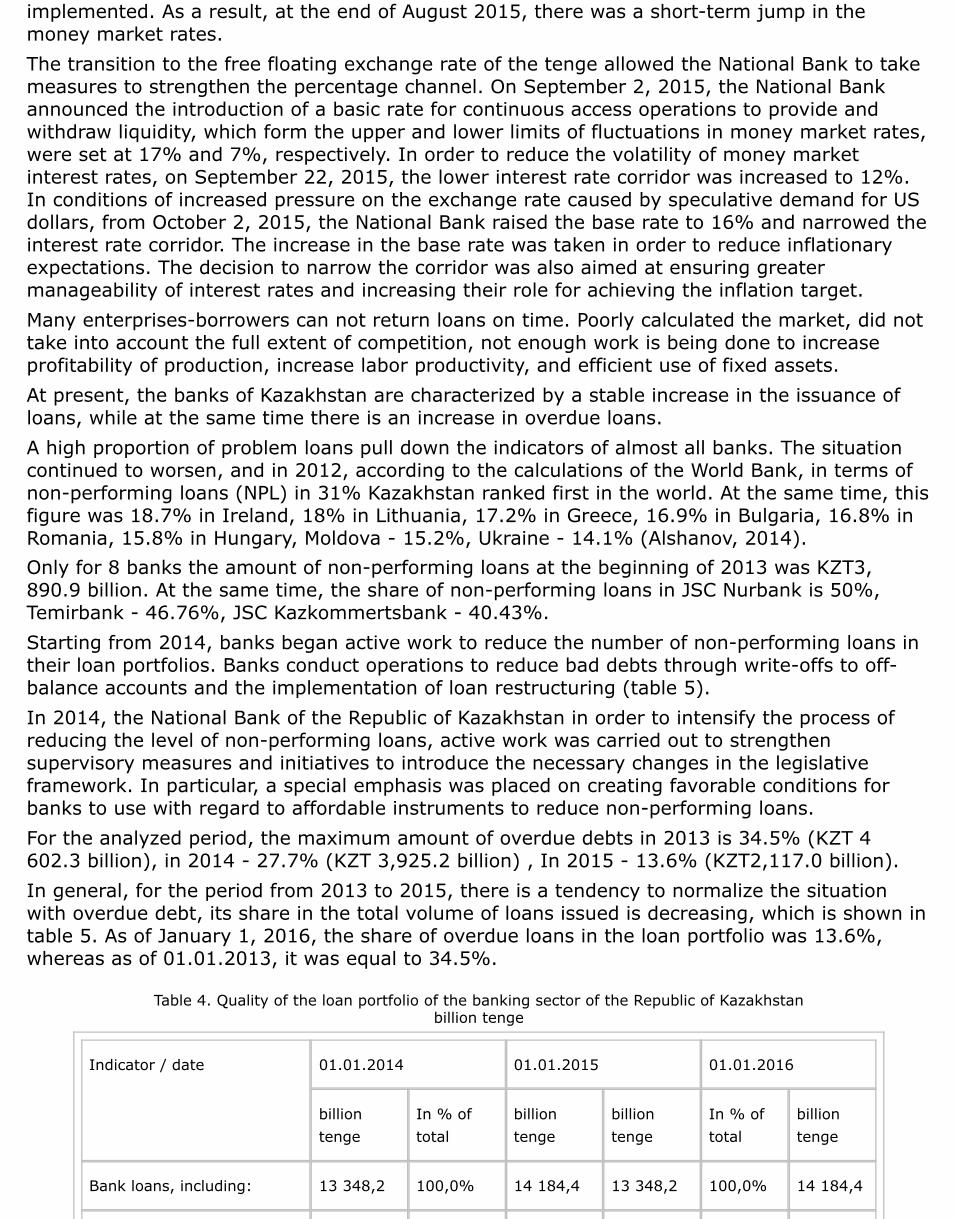

implemented. As a result, at the end of August 2015, there was a short-term jump in themoney market rates.The transition to the free floating exchange rate of the tenge allowed the National Bank to takemeasures to strengthen the percentage channel. On September 2, 2015, the National Bankannounced the introduction of a basic rate for continuous access operations to provide andwithdraw liquidity, which form the upper and lower limits of fluctuations in money market rates,were set at 17% and 7%, respectively. In order to reduce the volatility of money marketinterest rates, on September 22, 2015, the lower interest rate corridor was increased to 12%.In conditions of increased pressure on the exchange rate caused by speculative demand for USdollars, from October 2, 2015, the National Bank raised the base rate to 16% and narrowed theinterest rate corridor. The increase in the base rate was taken in order to reduce inflationaryexpectations. The decision to narrow the corridor was also aimed at ensuring greatermanageability of interest rates and increasing their role for achieving the inflation target.Many enterprises-borrowers can not return loans on time. Poorly calculated the market, did nottake into account the full extent of competition, not enough work is being done to increaseprofitability of production, increase labor productivity, and efficient use of fixed assets.At present, the banks of Kazakhstan are characterized by a stable increase in the issuance ofloans, while at the same time there is an increase in overdue loans.A high proportion of problem loans pull down the indicators of almost all banks. The situationcontinued to worsen, and in 2012, according to the calculations of the World Bank, in terms ofnon-performing loans (NPL) in 31% Kazakhstan ranked first in the world. At the same time, thisfigure was 18.7% in Ireland, 18% in Lithuania, 17.2% in Greece, 16.9% in Bulgaria, 16.8% inRomania, 15.8% in Hungary, Moldova - 15.2%, Ukraine - 14.1% (Alshanov, 2014).Only for 8 banks the amount of non-performing loans at the beginning of 2013 was KZT3,890.9 billion. At the same time, the share of non-performing loans in JSC Nurbank is 50%,Temirbank - 46.76%, JSC Kazkommertsbank - 40.43%.Starting from 2014, banks began active work to reduce the number of non-performing loans intheir loan portfolios. Banks conduct operations to reduce bad debts through write-offs to off-balance accounts and the implementation of loan restructuring (table 5).In 2014, the National Bank of the Republic of Kazakhstan in order to intensify the process ofreducing the level of non-performing loans, active work was carried out to strengthensupervisory measures and initiatives to introduce the necessary changes in the legislativeframework. In particular, a special emphasis was placed on creating favorable conditions forbanks to use with regard to affordable instruments to reduce non-performing loans.For the analyzed period, the maximum amount of overdue debts in 2013 is 34.5% (KZT 4602.3 billion), in 2014 - 27.7% (KZT 3,925.2 billion) , In 2015 - 13.6% (KZT2,117.0 billion).In general, for the period from 2013 to 2015, there is a tendency to normalize the situationwith overdue debt, its share in the total volume of loans issued is decreasing, which is shown intable 5. As of January 1, 2016, the share of overdue loans in the loan portfolio was 13.6%,whereas as of 01.01.2013, it was equal to 34.5%.

Table 4. Quality of the loan portfolio of the banking sector of the Republic of Kazakhstanbillion tenge

Indicator / date 01.01.2014 01.01.2015 01.01.2016

billiontenge

In % oftotal

billiontenge

billiontenge

In % oftotal

billiontenge

Bank loans, including: 13 348,2 100,0% 14 184,4 13 348,2 100,0% 14 184,4

Loans for which there is nooverdue debt on principaland / or accrued interest

8 745,9 65,5% 10 259,2 8 745,9 65,5% 10 259,2

Loans with overdue debtsfrom 1 to 30 days

209,90 1,6% 357,2 209,90 1,6% 357,2

Loans with overdue debtsfrom 31 to 60 days

91,5 0,7% 158,4 91,5 0,7% 158,4

Loans with overdue debtsfrom 61 to 90 days

142,7 1,1% 69,4 142,7 1,1% 69,4

Loans with overdue debts ofmore than 90 days

4 158,2 31,2% 3 340,2 4 158,2 31,2% 3 340,2

IFRS Provisions 4 643,9 34,8% 3 569,8 4 643,9 34,8% 3 569,8

Coefficient of covering byprovisions under IFRS ofloans with overdue debtsover 90 days

111,7% 106,9% 111,7% 106,9%

Note: Based on the materials of the National Bank of the Republic of Kazakhstan (The official website ofthe National Bank of the Republic of Kazakhstan)

It should be noted that the debt on loans for the period under review is growing (Table 4). So,as of 01.01.2015, arrears on loans increased by 6.3%, and the growth of overdue loansamounted to 17.3%; As of 01.01.2016, arrears on loans increased by 9.7%, and the growth ofoverdue loans amounted to 31.0%. Average annual increase on overdue loans as of 01.01.2016amounted to 13.7% compared to 17.3% as of 01.01.2015 with the growth of debt on loans by3.4%.Consequently, the improvement in the situation with arrears is mainly due to the growth in theportfolio of loans issued.Consider the dynamics of the loan portfolio and loans with overdue debts of the banking sectorof the Republic of Kazakhstan for the period from 2013 to 2015 (Figure 10).

Figure 10. The share of overdue loans in the total volume of loans extended to the banking sector of the Republic ofKazakhstan

(The official website of the National Bank of the Republic of Kazakhstan)

As a result, the share of overdue loans decreased significantly and amounted to 2 117 billiontenge as of January 1, 2015 against 4,602.3 billion tenge as of 01.01.2014 and 3 925.2 billiontenge as of 01.01.2015 (figure 10). With a slowdown in the growth of the loan portfolio, theshare of overdue debt is likely to start rising after three years of decline. In this case, mostlikely, the situation will not be of a critical nature.In May 2014, the Commission for Evaluation and Control over Activities to Reduce OverdueLoans was established by National Bank of the Republic of Kazakhstan, which individuallymonitors the effectiveness of the measures taken by banks to improve the loan portfolio. Thebasic principles, instruments and measures necessary to manage overdue loans have beendefined in the adopted Unified Policy on reducing overdue loans in second-tier banks (Akkozov,2016).In order to effectively reduce non-performing loans and stimulate the solution of the NBRKproblem, certain work has been done to optimize tax legislation and reduce administrativebarriers for banks in the following areas:- extension until 2016. Tax benefits for forgiving bad debts (in the amount of not more than10% of the loan portfolio);- recognition in the tax accounting of losses from writing off from the balance of banks of badloans;- recognition in the tax accounting of losses from the transfer with a discount of problem assetsin the WSE, which has a temporary preferential tax treatment (tax privilege is effective fromJanuary 1, 2012 to January 1, 2018);- exemption from taxation of income of individuals when writing off bad debts for the balancesheet, as well as forgiving the debt in a number of cases;- granting tax benefits to banks that have undergone restructuring, in order to facilitate theresolution of the problem of non-performing loans;- expansion of the powers of the OASA to conduct all activities to improve the quality ofdistressed assets.- optimization of the criteria for forgiving bad debts.In addition, from January 1, 2016, it provides for the introduction of a prudential standard forthe maximum share of non-performing loans in the loan portfolio of the bank at a level of notmore than 10%.

To activate the activity of JSC "Fund for Problem Loans", a new Concept of functioning of the"Problem Loan Fund" was adopted, aimed at a more active and diversified interaction of theFund with banks through mechanisms for equitable distribution of risks when buying out badloans. "Implementation of the measures envisaged by this Concept is expected to increase theeffectiveness of the Fund, in particular:- considering the increase in the Fund's resources, the availability of a list of flexiblemechanisms for working with banks, a significant contribution will be made to the target levelof "non-performing" loans (no more than 10%) both by individual banks and the bankingsystem as a whole;- assistance in improving the practice of determining the value of distressed assets;3) assistance in forming a benchmark in the pricing of financial instruments in the securitizationof the asset portfolio;- assistance in the formation of the circulation market for "non-performing" loans (Stateprogram of industrial and innovative development of the Republic of Kazakhstan for 2015 –2019).In conditions of increasing consumer activity, growth of incomes of the population and slowingof industrial production, banks have become more preferable to give short-term consumerloans. The current level of credit risks associated with this is insignificant. The economic environment in which the financial sector functions continues to be characterizedby high credit risks of borrowers. The share of "non-performing" loans of banks is graduallydecreasing, thanks to measures taken by the State and the National Bank of the Republic ofKazakhstan. The active write-off of non-performing loans by banks resulted in a significantdecrease in their level to a minimum of 23.5% over the past five years.As a whole for 2015, the credit activity of banks in the issue of issuing new loans hasmoderately increased. At the same time, growth was ensured by almost all groups of banks,who received support from the state, so they independently attracted the necessary resources.Adjusting the exchange rate of the national currency, reducing world oil prices, depreciating theRussian ruble, the difficult geopolitical situation in the world and the slowdown in worldeconomic growth since the second half of 2014 have had an impact on the financial stability ofthe banking sector. The result was a decrease in the lending activity of banks and a reduction inthe growth rate of the loan portfolio. The loan portfolio growth slowed not only due to adecrease in overall lending activity, but also due to active write-off by banks of non-performingloans primarily in the corporate sector.An analysis of Kazakhstan's credit market shows the growing dynamics of loans provided bybanks to customers. The volume of banks lending to the economy at the end of 2015 was15,554 billion tenge, an increase of 9.7% over the year. The volume of loans in nationalcurrency amounted to 10,608 billion tenge (since the beginning of the year the increase was4.8%), in foreign currency - 4,946 billion tenge (since the beginning of the year growth by21.8%). The share of loans in tenge was 68.2%.The volume of long-term loans at the end of 2015 amounted to KZT12,189 billion, an increaseof 10.7% over the year, and a short-term level of KZT3,365 billion (an increase of 5.8% overthe year).The volume of loans to legal entities at the end of 2015 increased by 12.7% to KZT 11,108billion, individuals increased by 2.8% to KZT4,446 billion. The share of loans to individuals was28.6%.

Bibliographic referencesAkkozov, B. (2016). Clearing of "bad" loans in banks of the RK. What will happen in a year?Recovered from: http://www.afk.kz/index.php/en/bankovsky-sektor/ (reference date is January

25, 2016)Alshanov, R. (2014). Doctor of Economics, Rector of the University "Turan", Economic Policy ofKazakhstan at the present stage. Recovered from: http://www.nomad.su/?a=4-201403260022(accessed: 10.03.2016)Money, credit, banks: Textbook (2006). In Prof. G. N. Beloglazova (ed.). Moscow: Yurayt, p.208.State of the Nation Address by President of Kazakhstan Nursultan Nazarbayev «Kazakhstan ina new global reality: Growth. Reforms. Development» (Astana, November 30, 2015).Recovered from: http://online.zakon.kz/ accessed 12.02. 2016State program of industrial and innovative development of the Republic of Kazakhstan for 2015– 2019. Official website of the President of the Republic of Kazakhstan N.Nazarbayev. Recovered from: http://akorda.kz.Tavasiev V. M. (2008). Banking. M .: UNITY-DANA, 528s.The official website of the National Bank of the Republic of Kazakhstan. Recovered from:http://www.nationalbank.kz

1. Associate Professor, Department of Finance, Al-Farabi Kazakh National University2. Professor, Vice Rector for Academic Affairs, Department of Creative Specialties, Abai Kazakh National PedagogicalUniversity3. Candidate of Economic Sciences, Associate Professor, Department of Finance and Statistics, NARXOZ University4. Senior Lecturer, Department of Finance, Al-Farabi Kazakh National University

Revista ESPACIOS. ISSN 0798 1015Vol. 38 (Nº 29) Año 2017

[Índice]

[En caso de encontrar algún error en este website favor enviar email a webmaster]

©2017. revistaESPACIOS.com • Derechos Reservados