perspectivas y tendencias en infraestructura · autopistas de peaje, servicios públicos regulados...

TRANSCRIPT

Perspectivas y Tendencias en Infraestructura

Junio 2017

2Moody’s Chile Briefing 2017

Agenda1. Desafíos para la inversión de infraestructura en la

región

2. Desarrollos recientes en autopistas chilenas

3. Mercado eléctrico chileno: Retos y oportunidades

4. ¿Boom en energías renovables?

3Moody’s Chile Briefing 2017

Financiamiento de infraestructuraregional – Desafíos1

4Moody’s Chile Briefing 2017

Desafíos en el sector de Infraestructura

Perspectivas de menorcrecimiento económico

Falta de proyectosfinanciables

Casos de corrupción

Gap infraestructura

Restricciones fiscales; Ratings soberanos

En el corto plazo

» Desafíos actuales y demoras asociadas a casos de corrupción

En el mediano-largo plazo

Latinoamérica se beneficiará de: – Compromiso a impulsar el

crecimiento vía la inversión en infraestructura

– Mayor desarrollo de APPs

– Marcos regulatorios fortalecidos

Infraestructura Regional

5Moody’s Chile Briefing 2017

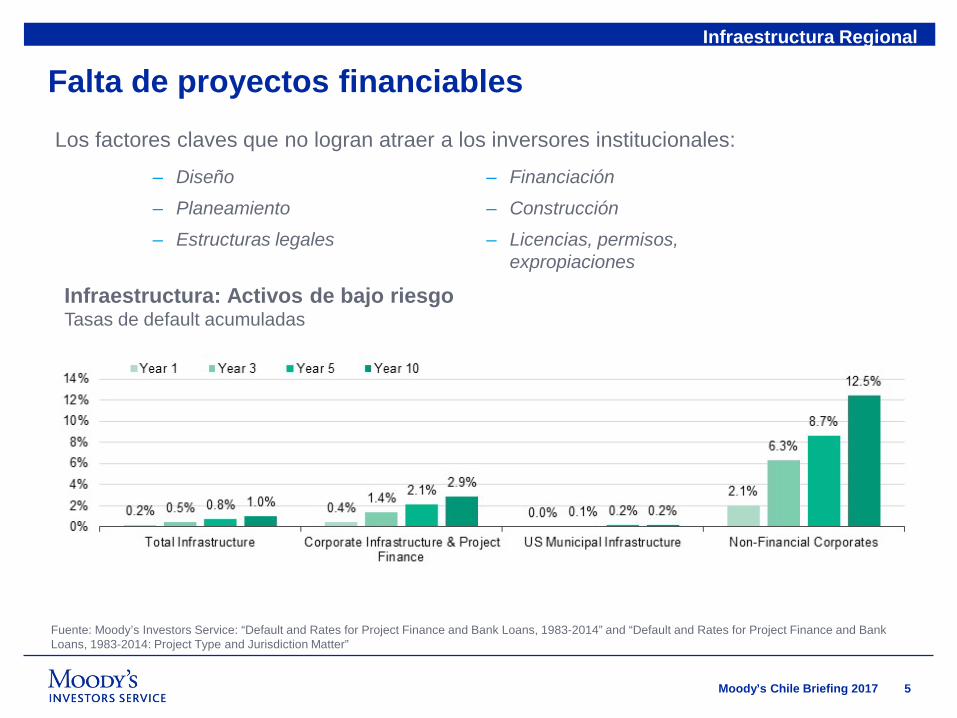

Falta de proyectos financiablesLos factores claves que no logran atraer a los inversores institucionales:

– Diseño

– Planeamiento

– Estructuras legales

– Financiación

– Construcción

– Licencias, permisos, expropiaciones

Infraestructura: Activos de bajo riesgoTasas de default acumuladas

Fuente: Moody’s Investors Service: “Default and Rates for Project Finance and Bank Loans, 1983-2014” and “Default and Rates for Project Finance and Bank Loans, 1983-2014: Project Type and Jurisdiction Matter”

Infraestructura Regional

6Moody’s Chile Briefing 2017

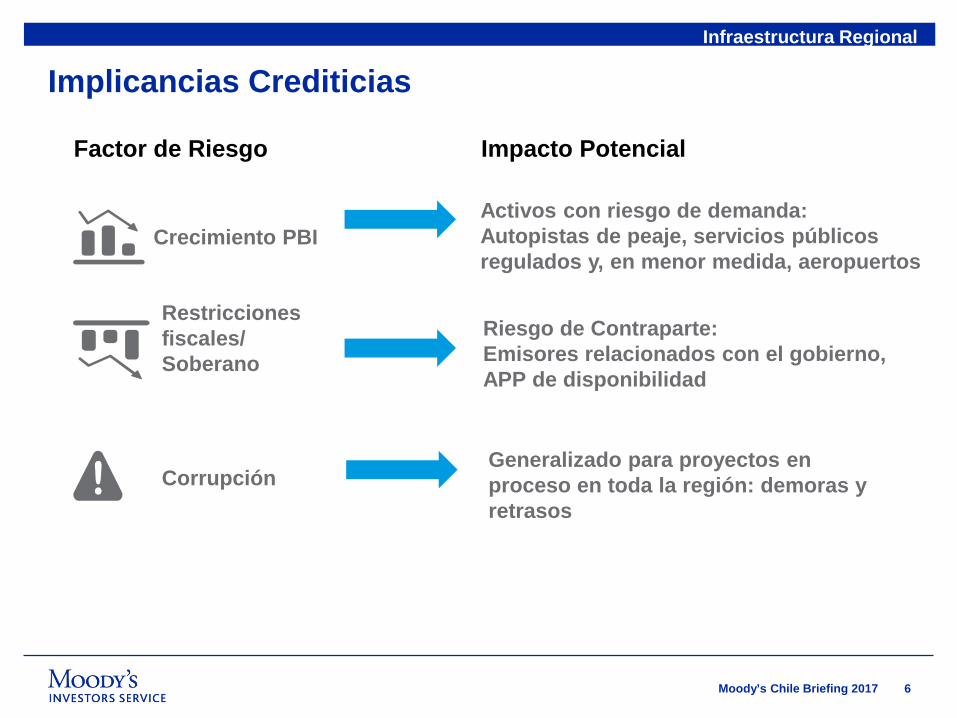

Implicancias Crediticias

Crecimiento PBI

Restriccionesfiscales/ Soberano

Corrupción

Activos con riesgo de demanda:Autopistas de peaje, servicios públicosregulados y, en menor medida, aeropuertos

Factor de Riesgo Impacto Potencial

Riesgo de Contraparte:Emisores relacionados con el gobierno, APP de disponibilidad

Generalizado para proyectos en proceso en toda la región: demoras y retrasos

Infraestructura Regional

7Moody’s Chile Briefing 2017

Desarrollos recientes en autopistaschilenas2

8Moody’s Chile Briefing 2017

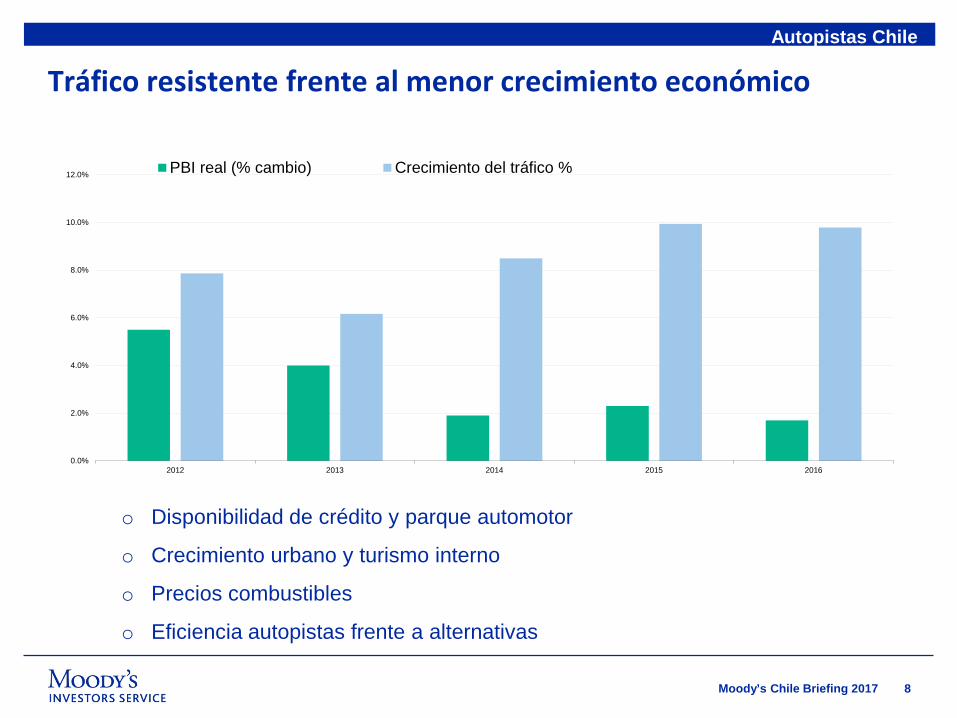

Tráfico resistente frente al menor crecimiento económico

o Disponibilidad de crédito y parque automotor

o Crecimiento urbano y turismo interno

o Precios combustibles

o Eficiencia autopistas frente a alternativas

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2012 2013 2014 2015 2016

PBI real (% cambio) Crecimiento del tráfico %

Autopistas Chile

9Moody’s Chile Briefing 2017

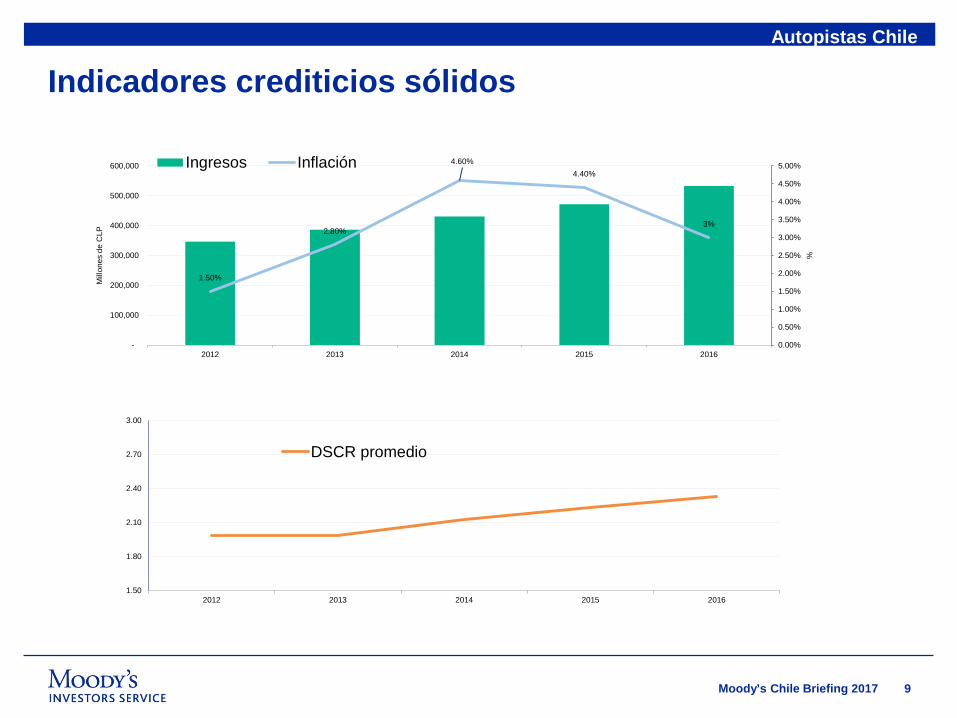

Indicadores crediticios sólidos

1.50%

2.80%

4.60%4.40%

3%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

-

100,000

200,000

300,000

400,000

500,000

600,000

2012 2013 2014 2015 2016

%

Mill

ones

de

CLP

Ingresos Inflación

1.50

1.80

2.10

2.40

2.70

3.00

2012 2013 2014 2015 2016

DSCR promedio

Autopistas Chile

10Moody’s Chile Briefing 2017

Inversiones en el sector lentas y limitadas

• Expansión de concesiones actuales

Vía extensión de los contratos o peajes adicionales

Limitado espacio para incrementar tarifas

• Pocas oportunidades de inversión en el corto/mediano plazo

Concesión AVO, USD 800 millones

Segunda Concesión Rutas del Loa, USD 190 millones

Ruta Nahuelbuta (Ruta 180), USD 160 millones

Autopistas Chile

11Moody’s Chile Briefing 2017

Tendencias en el mercado eléctricochileno3

12Moody’s Chile Briefing 2017

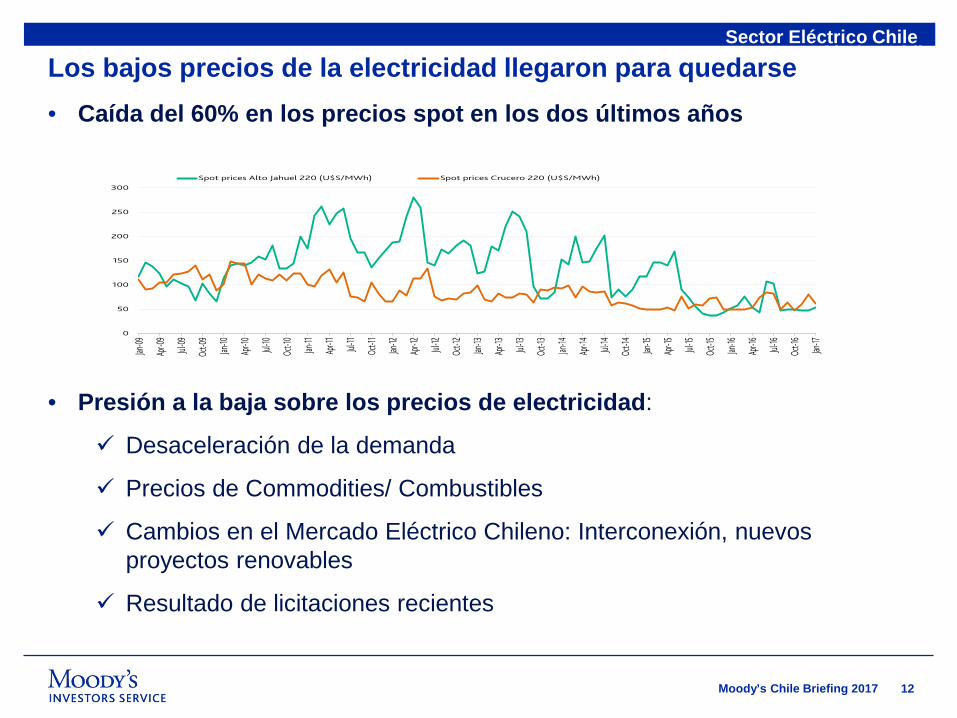

Los bajos precios de la electricidad llegaron para quedarse• Caída del 60% en los precios spot en los dos últimos años

• Presión a la baja sobre los precios de electricidad:

Desaceleración de la demanda

Precios de Commodities/ Combustibles

Cambios en el Mercado Eléctrico Chileno: Interconexión, nuevosproyectos renovables

Resultado de licitaciones recientes

0

50

100

150

200

250

300

Jan-09

Apr-0

9

Jul-09

Oct-0

9

Jan-10

Apr-1

0

Jul-10

Oct-1

0

Jan-11

Apr-1

1

Jul-11

Oct-1

1

Jan-12

Apr-1

2

Jul-12

Oct-1

2

Jan-13

Apr-1

3

Jul-13

Oct-1

3

Jan-14

Apr-1

4

Jul-14

Oct-1

4

Jan-15

Apr-1

5

Jul-15

Oct-1

5

Jan-16

Apr-1

6

Jul-16

Oct-1

6

Jan-17

Spot prices Alto Jahuel 220 (U$S/MWh) Spot prices Crucero 220 (U$S/MWh)

Sector Eléctrico ChileSector Eléctico Chile

13Moody’s Chile Briefing 2017

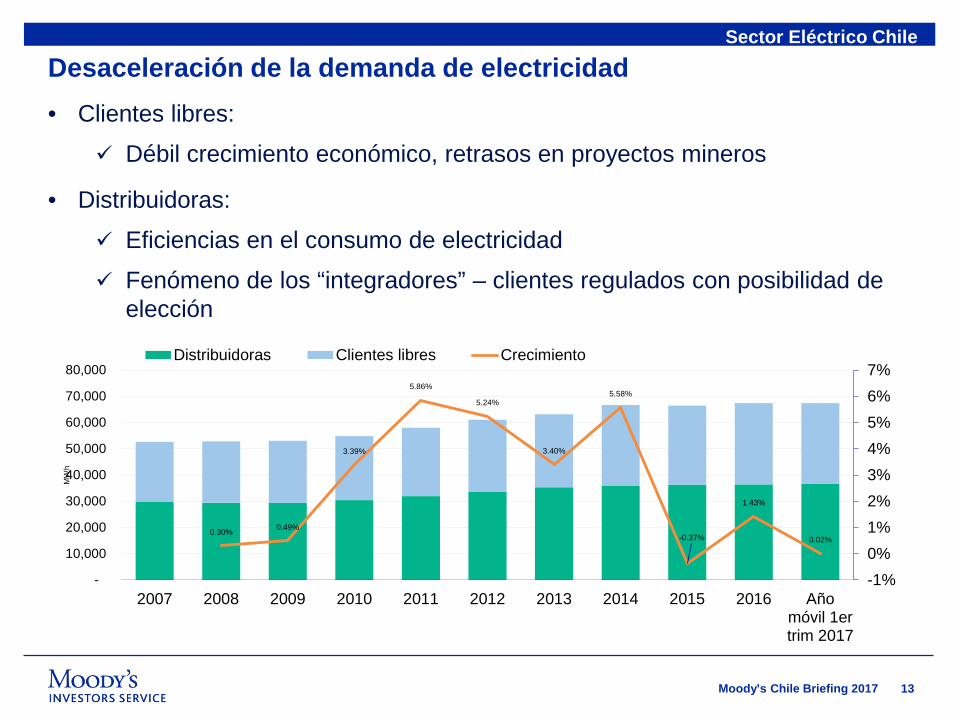

Desaceleración de la demanda de electricidad• Clientes libres:

Débil crecimiento económico, retrasos en proyectos mineros

• Distribuidoras:

Eficiencias en el consumo de electricidad

Fenómeno de los “integradores” – clientes regulados con posibilidad de elección

0.30% 0.49%

3.39%

5.86%

5.24%

3.40%

5.58%

-0.37%

1.43%

0.02%

-1%0%1%2%3%4%5%6%7%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Añomóvil 1ertrim 2017

MW

h

Distribuidoras Clientes libres Crecimiento

Sector Eléctrico Chile

14Moody’s Chile Briefing 2017

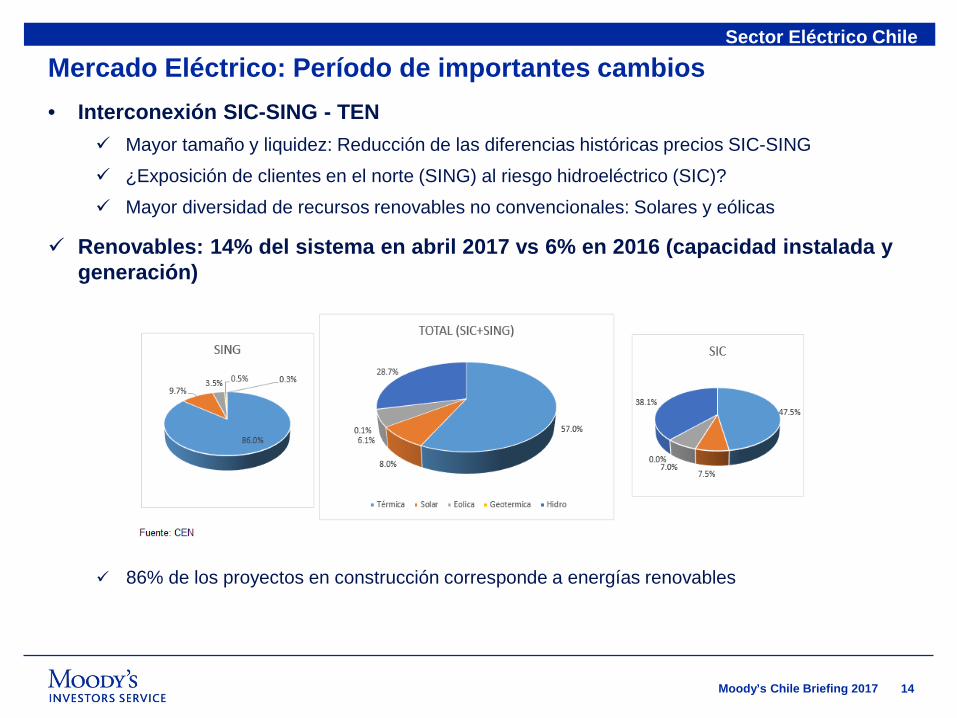

Mercado Eléctrico: Período de importantes cambios• Interconexión SIC-SING - TEN

Mayor tamaño y liquidez: Reducción de las diferencias históricas precios SIC-SING

¿Exposición de clientes en el norte (SING) al riesgo hidroeléctrico (SIC)?

Mayor diversidad de recursos renovables no convencionales: Solares y eólicas

Renovables: 14% del sistema en abril 2017 vs 6% en 2016 (capacidad instalada y generación)

86% de los proyectos en construcción corresponde a energías renovables

Sector Eléctrico Chile

15Moody’s Chile Briefing 2017

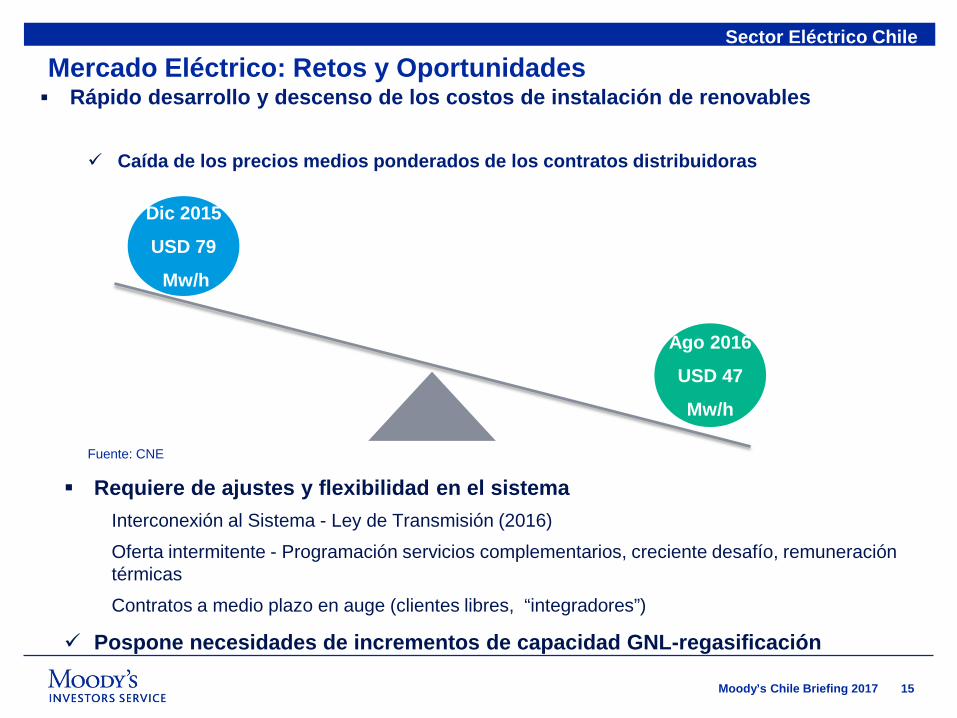

Mercado Eléctrico: Retos y Oportunidades Rápido desarrollo y descenso de los costos de instalación de renovables

Caída de los precios medios ponderados de los contratos distribuidoras

Fuente: CNE

Requiere de ajustes y flexibilidad en el sistemaInterconexión al Sistema - Ley de Transmisión (2016)

Oferta intermitente - Programación servicios complementarios, creciente desafío, remuneración térmicas

Contratos a medio plazo en auge (clientes libres, “integradores”)

Pospone necesidades de incrementos de capacidad GNL-regasificación

Ago 2016

USD 47

Mw/h

Dic 2015

USD 79

Mw/h

Sector Eléctrico Chile

16Moody’s Chile Briefing 2017

Generadores convencionales: Impacto Financiero• Impacto a Corto y Medio plazo: LimitadoCaída de precios spot: limitado; alto nivel de contratación

Sin embargo, desaceleración de la demanda afecta: Mayoría de los contratos sin cláusulas “Take or Pay”

• Creciente Incertidumbre a partir del 2023 Resultado de las próximas licitaciones distribuidoras – volumen y precios

Financiación y comisión exitosa de los proyectos renovables (ERNC)

Requiere estructura de capital prudente

Empresa Tecnología % contratado

Vencimiento post 2021

AES Gener Térmica 94% 76%Angamos Carbón 99% 100%

Enel Generación Chile Hidro/Térmica 100% 86%

Sector Eléctrico Chile

17Moody’s Chile Briefing 2017

Tendencia a la baja en precios renovables es regional USD/ MWh

2012• 120

2016• 53

2010• 98

2012• 63

2016 1ra. subasta

• 42

2016 2da. subasta

• 33

Argentina Uruguay México

Adjudicaciones de energías renovables

Sector Eléctrico Chile

18Moody’s Chile Briefing 2017

¿Boom en energías renovables?

4

19Moody’s Chile Briefing 2017

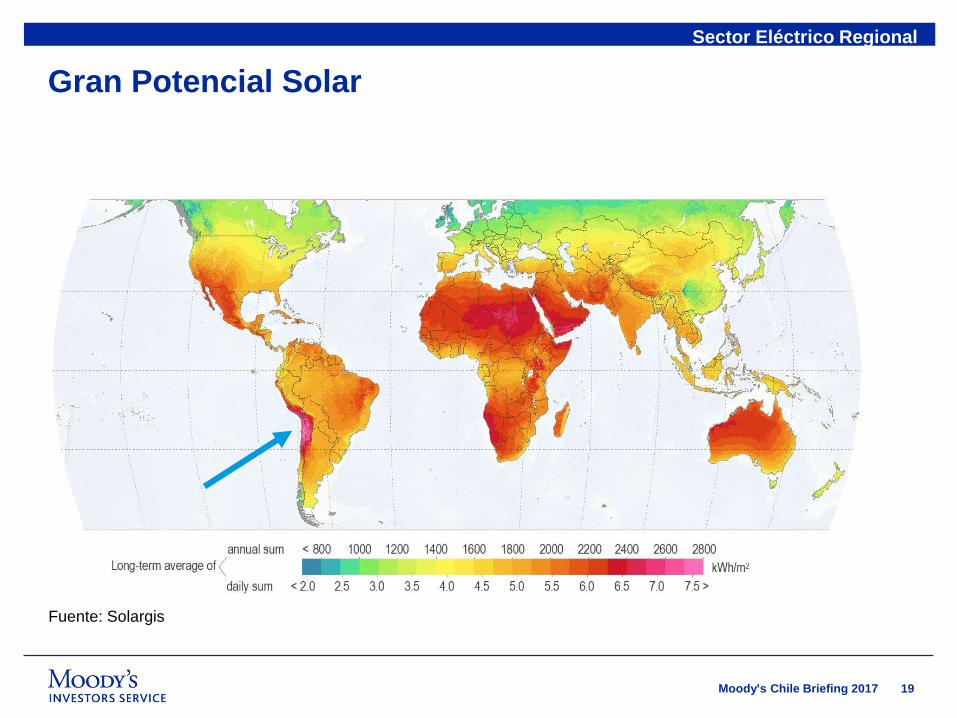

Gran Potencial Solar

Fuente: Solargis

Sector Eléctrico Regional

20Moody’s Chile Briefing 2017

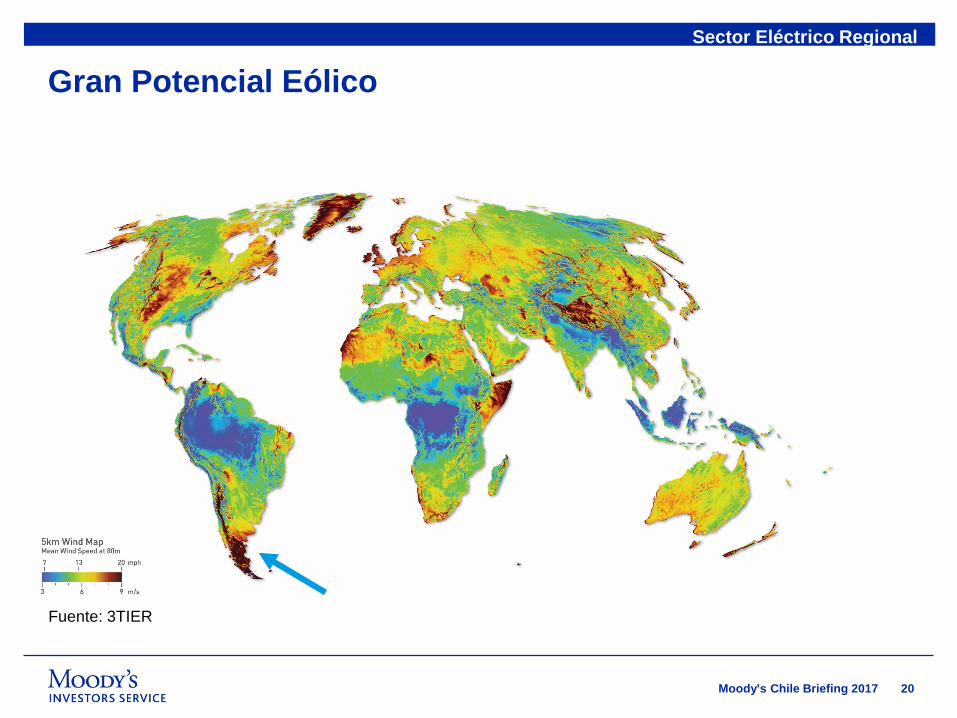

Gran Potencial Eólico

Fuente: 3TIER

Sector Eléctrico Regional

21Moody’s Chile Briefing 2017

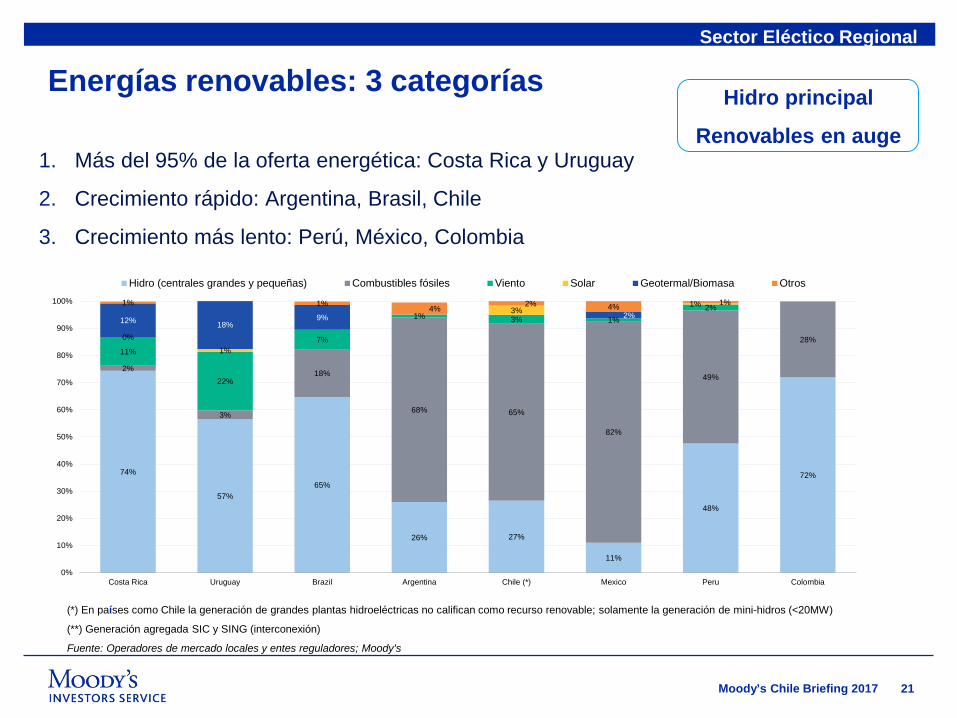

Energías renovables: 3 categorías

1. Más del 95% de la oferta energética: Costa Rica y Uruguay

2. Crecimiento rápido: Argentina, Brasil, Chile

3. Crecimiento más lento: Perú, México, Colombia

(*) En países como Chile la generación de grandes plantas hidroeléctricas no califican como recurso renovable; solamente la generación de mini-hidros (<20MW)

(**) Generación agregada SIC y SING (interconexión)

Fuente: Operadores de mercado locales y entes reguladores; Moody's

74%

57%65%

26% 27%

11%

48%

72%

2%

3%

18%

68% 65%

82%

49%

28%11%

22%

7%

1% 3% 1%2%

0%

1%

3%1%

12% 18%9% 2%

1% 1% 4% 2% 4% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Costa Rica Uruguay Brazil Argentina Chile (*) Mexico Peru Colombia

Hidro (centrales grandes y pequeñas) Combustibles fósiles Viento Solar Geotermal/Biomasa Otros

Hidro principal

Renovables en auge

Sector Eléctico Regional

22Moody’s Chile Briefing 2017

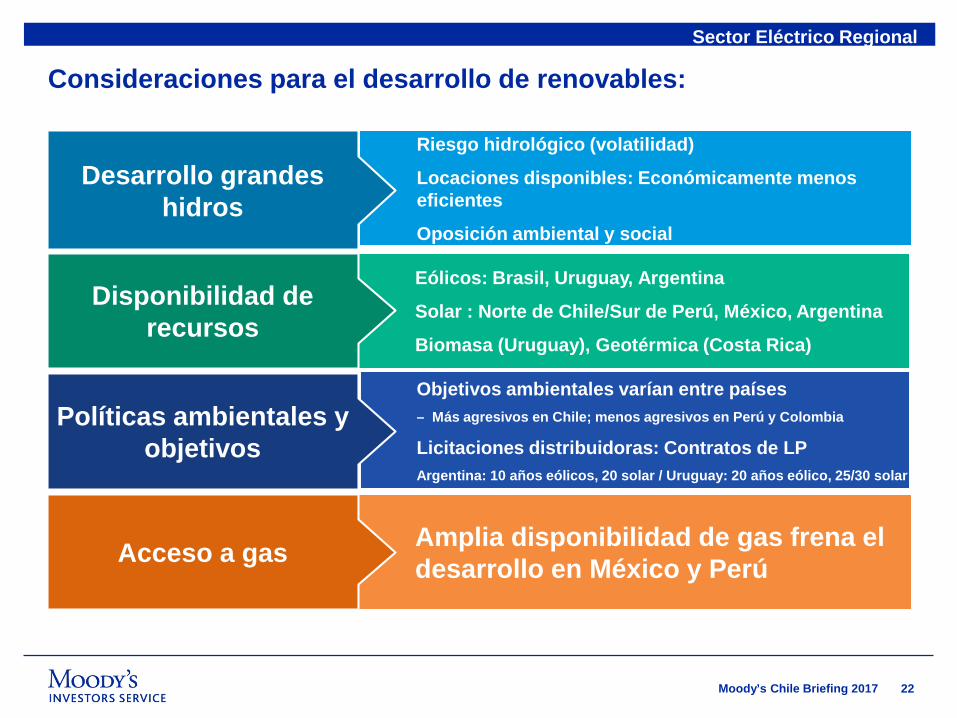

Consideraciones para el desarrollo de renovables:

Eólicos: Brasil, Uruguay, Argentina

Solar : Norte de Chile/Sur de Perú, México, Argentina

Biomasa (Uruguay), Geotérmica (Costa Rica)

Objetivos ambientales varían entre países– Más agresivos en Chile; menos agresivos en Perú y Colombia

Licitaciones distribuidoras: Contratos de LP Argentina: 10 años eólicos, 20 solar / Uruguay: 20 años eólico, 25/30 solar

Amplia disponibilidad de gas frena el desarrollo en México y Perú

Disponibilidad de recursos

Políticas ambientales y objetivos

Acceso a gas

Riesgo hidrológico (volatilidad)

Locaciones disponibles: Económicamente menoseficientes

Oposición ambiental y social

Desarrollo grandeshidros

Sector Eléctrico Regional

23Moody’s Chile Briefing 2017

Licitaciones distribuidoras: Clave para desarrollo de renovables

Centralizadas: Todos exceptoColombia

Text

Depreciación Acelerada

Excepción IVA/ I. Ingresos

Imp. Carbono (Chile)

Objetivos medioambientales Incentivos Fiscales

Subastas Públicas

Perú

Tarifa preferencial (feed-in)

Políticas de Incentivos hacia Renovables

Argentina 20% 2025Brasi 86% 2023Chile 20% 2025Colombia No NAC. Rica 97% 2018México 50% 2050Perú 6% 2018Uruguay 90% 2015

Fuente: International Renewable Energy Agency, National legislation

Sector Eléctrico Regional

24Moody’s Chile Briefing 2017

Desafíos en el desarrollo de ERNC

Cuellos de botella: Retrasos en la conexión de proyectos

Plazo contratos

Precios agresivos y nuevas tecnologías

Garantías

Tortuosa gestión ambiental y social

Transmisión

Comisión y Financiación

Oposición social y retos ambientales

Chile: Demanda sector minero, servicios auxiliares

Costa Rica: Embalses de hidroeléctricas para compensar Oferta intermitente -

recursos de respaldo

Sector Eléctrico Regional

25Moody’s Chile Briefing 2017

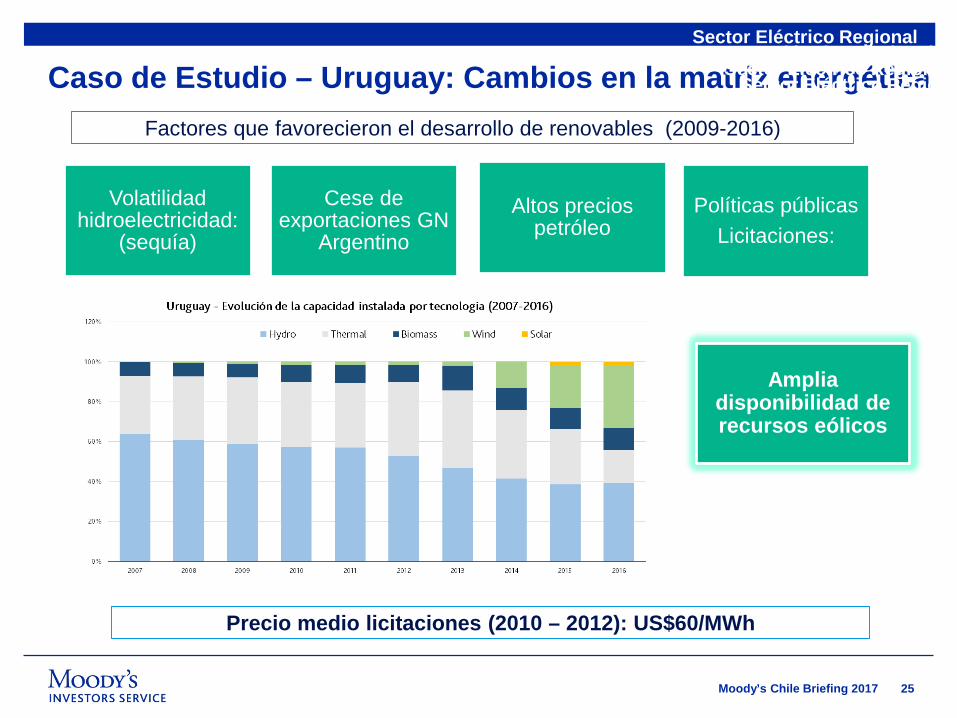

Caso de Estudio – Uruguay: Cambios en la matriz energética

Volatilidadhidroelectricidad:

(sequía)

Cese de exportaciones GN

Argentino

Altos precios petróleo

Políticas públicasLicitaciones:

Factores que favorecieron el desarrollo de renovables (2009-2016)

Precio medio licitaciones (2010 – 2012): US$60/MWh

Ampliadisponibilidad de recursos eólicos

Sector Eléctrico RegionalSector Eléctrico Regional

Sector Eléctrico RegionalSector Eléctrico Regiona

Alejandro OlivoAssociate Managing Director

Tel: [email protected]

Natividad Martel, CFAVP – Senior AnalystTel: +1.212.553.4561

Daniela CuanVP – Senior Analyst

Tel: [email protected]

Bernardo CostaVP – Senior Analyst

Tel: [email protected]

27Moody’s Chile Briefing 2017

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.