institutul na•ional de statistic† revista român! de …...ca reper cazuistic, vom porni cu...

TRANSCRIPT

Revista Român! de Statistic!

Supliment

Romanian Statistical Review Supplement

2/2017

Institutul Na�ional de Statistic�

National Institute of Statistics

www.revistadestatistic .ro/supliment

COLEGIUL !TIIN"IFIC

EMILIAN DOBRESCU - academician, Academia Român!

AUREL IANCU - academician, Academia Român!

MARIUS IOSIFESCU - academician, Academia Român!

LUCIAN ALBU - academician, Academia Român!

GHEORGHE ZAMAN � Prof. univ. dr., membru corespondent al Academiei Române

TUDOREL ANDREI - Prof. univ. dr., Academia de Studii Economice

DAN GHERGU" - Lect. univ. dr. , Universitatea Titu Maiorescu, Bucure"ti

KONRAD PASENDORFER � PhD, Director General al Statistics Austria

MARIANA MIHAILOVA KOTZEVA - EUROSTAT

CONSTANTIN MITRU" � Prof. univ. dr., Pre"edinte al Societ!#ii Române de Statistic!

CONSTANTIN ANGHELACHE � Prof. univ. dr., Vicepre"edinte al Societ!#ii Române de Statistic!

NICOLAE ISTUDOR � Prof. univ. dr., Rector al Academiei de Studii Economice, Bucure"ti

VERGIL VOINEAGU � Prof. univ. dr., Academia de Studii Economice, Bucure"ti

TIBERIU POSTELNICU � Prof. univ. dr., Institutul �Gheorghe Mihoc-Caius Iacob�

BOGDAN OANCEA � Prof. univ. dr., Universitatea Bucure"ti

GHEORGHE S#VOIU - Conf. univ. dr., Universitatea Pite"ti

IRINA-VIRGINIA DRAGULANESCU - Prof. univ. dr., University Messina, Italia

DANIELA ELENA !TEF#NESCU - Conf. univ. dr., Institutul Na#ional de Statistic!

ELISABETA JABA � Prof. univ. dr., Universitatea �Alexandru Ioan Cuza� University

EUGENIA HARJA - Prof. univ. dr., Universitatea Vasile Alecsandri, Bac!u

!TEFAN-ALEXANDRU IONESCU - Lect. univ. dr. Universitatea Româno-American!

CLAUDIU HER"ELIU - Prof. univ. dr., Academia de Studii Economice

ION GHIZDEANU - Dr., cercet!tor "tiin#i$ c gradul I, Comisia Na#ional! de Prognoz!

ILIE DUMITRESCU - Institutul Na#ional de Statistic!

SILVIA PISIC# - Dr., Institutul Na#ional de Statistic!

ADRIANA CIUCHEA - Institutul Na#ional de Statistic!

Revista Română de Statistică - Supliment nr. 2 / 2017

SUMAR / CONTENTS 2/2017REVISTA ROMÂNĂ DE STATISTICĂ SUPLIMENT

ASPECTE SEMNIFICATIVE PRIVIND CONSUMUL ŞI ECONOMISIREA 3SIGNIFICANT ISSUES ON CONSUMPTION AND SAVING 12Prof. univ. dr. Alexandru MANOLEConf. univ. dr. Madalina-Gabriela ANGHELDrd. Georgiana NIȚU

PRECAUŢIUNEA ECONOMISIRII ÎN CONDIŢII DE INCERTITUDINE 21PRECAUTION OF SAVINGS UNDER UNCERTAIN CIRCUMSTANCES 30Prof. univ. dr. Constantin ANGHELACHEConf. Univ. Dr. Aurelian DIACONU Drd. Emilia STANCIU

ELEMENTE TEORETICE PRIVIND MANAGEMENTUL DE PORTOFOLIU DINAMIC 38THEORETICAL ASPECTS OF THE DYNAMIC PORTFOLIO MANAGEMENT 47Conf. univ. dr. Madalina-Gabriela ANGHELConf. univ. dr. Mirela PANAITProf. univ. dr. Alexandru MANOLEDrd. Marius POPOVICI

DIVERSIFICAREA TEMPORALĂ ÎN CONSUM ŞI ECONOMISIRE 56TIME DIVERSIFICATION IN CONSUMPTION AND SAVING 64Prof. univ. dr. Constantin ANGHELACHEProf. univ. dr. Radu Titus MARINESCU Asistent univ dr. Diana Valentina DUMITRESCU

MODEL DE ANALIZĂ A CORELAŢIEI DINTRE PRODUSUL INTERN BRUT ŞI COMPONENTELE CONSUMULUI FINAL 71MODEL ANALYSIS OF THE CORRELATION BETWEEN GDP AND FINAL CONSUMPTION COMPONENTS 84Prof. univ. dr. Constantin ANGHELACHEDrd. Andreea Ioana MARINESCUDrd. Doina AVRAMDrd. Doina BUREADrd. Gyorgy BODO

MODEL DE ANALIZĂ A CORELAŢIEI DINTRE CONSUMUL FINAL ŞI COMPONENTELE ACESTUIA 96MODEL ANALYSIS OF THE CORRELATION BETWEEN FINAL CONSUMPTION AND ITS COMPONENTS 105Prof. univ. dr. Alexandru MANOLE Lector univ. dr. Mariana BUNEA Lector univ. dr. Ana CARPAsist. Univ. Dr. Diana-Valentina SOAREDrd. Maria MIREA

www.revistadestatistica.ro/supliment

Romanian Statistical Review - Supplement nr. 2 / 20172

MODEL ECONOMETRIC DE ANALIZĂ A CORELAŢIEI DINTRE PRODUSUL INTERN BRUT ŞI CONSUMUL FINAL 114ANALYSIS OF THE ECONOMETRIC MODEL OF THE CORRELATION BETWEEN GDP AND FINAL CONSUMPTION 122Conf. univ. dr. Mădălina-Gabriela ANGHELDrd. Radu STOICADrd. Tudor SAMSONDrd. Alexandru BADIU

THE CONTRIBUTION OF HIGHER EDUCATION TO THE ACCUMULATION OF HUMAN CAPITAL IN THE ROMANIAN ARCHITECTURE FIELD DURING COMMUNISM 130Valentin Maier

METHODOLOGICAL AND APPLICATIVE PROBLEMS OF USING PEARSON CORRELATION COEFFICIENT IN THE ANALYSIS OF SOCIO-ECONOMIC VARIABLES 148Daniela-Emanuela Dănăcică

THE INFLUENCE OF THE MARKETING COMMUNICATION ON CONSUMER BEHAVIOR 164Gheorghe ORZANRaluca-Florentina TIŢA Raluca-Giorgiana CHIVU Ștefan-Ilie OANȚĂ Cristian Ionuț COMAN

Revista Română de Statistică - Supliment nr. 2 / 2017 3

Aspecte semnifi cative privind consumul şi economisirea

Prof. univ. dr. Alexandru MANOLEUniversitatea „ARTIFEX” din BucureștiConf. univ. dr. Madalina-Gabriela ANGHELUniversitatea „ARTIFEX” din BucureștiDrd. Georgiana NIȚU

Academia de Studii Economice din București

Abstract

In acest articol, autorii analizează unele aspecte privind corelaţia dintre consum şi economisire. Sunt abordate consumul şi economisirea în condiţii certe, fl uctuaţia în timp a consumului, posibilităţile de creştere a consumului în mod optim în condiţii de certitudine. Modelele prezentate sunt descrise în detaliu şi comentate. Între economisire și consum se derulează întreaga dinamică subiectivă a comportamentului uman care pendulează între achiziționare de bunuri și hârtii de valoare și păstrarea într-o formă sau alta a banilor. Într-o formă sau alta, pentru că achiziția de titluri de valoare sau acțiuni, dincolo de caracterul comercial al acțiunii, semnifi că totuși o investiție în hârtii cu valoare corespunzătoare banilor, care, în fi nal, reprezintă și ei hârtii investite cu o anumită valoare și, inevitabil, și semnifi cație. Aceste două ipostaze ale dinamicii decidentului fac parte din elementele arcului de timp important important în modelarea comportamentului subiectiv al decidentului. Scoțând inițial actul de modelare în afara timpului, prin considerarea demersului decizional ca derulat într-o singură perioadă de timp, s-au stabilit regulile modelării matematice a comportamentului decizional într-un cadru static, supus doar acțiunii unui anumit număr de variabile, afl ate cât mai puțin sub imperiul subiectivității și cât mai mult sub cel al obictivității. Cuvinte cheie : certitudine, decizie, consum, economisire, resurse Clasifi care JEL : E20, E21

Introducere

Până acum, am asumat faptul de decidentul acoperă doar un singur ciclu. Aceasta perspectivă obscurizează dimensiunea intertemporală importantă a riscului. În viața reală, agenții pot amâna riscul pentru mai târziu. Într-adevăr, abilitatea de a amâna alegerile riscante crește valoarea propriei

Romanian Statistical Review - Supplement nr. 2 / 20174

alegeri, de obicei numită ”valoare alegerii reale”. Decidenții pot alege să împartă câștigurile și pierderile posibile în alegerile curente pe care le au de făcut în mai multe perioade de timp și cicluri, care devine astfel un tip de diversifi care temporală a efectelor riscului cu privire la consumul fi nal. Alternativ, ei pot spera să recupereze unele dintre pierderile curente asumându-și riscuri suplimentare în viitor. În extrem, acest tip poate conduce la strategia ”asumă-ți pierderea totală”, precum un jucător la Las Vegas care pariază puținii bani de care dispune într-un pariu fi nal și ultim în speranța de a recupera pierderile masive suferite. În fi nal, agenții pot schimba nivelele de consum și economisire planifi cate în așteptarea confruntării viitoare cu incertitudinea, precum și să economisească un pic mai mult în fazele anterioare ca un gen de protecție față de riscuri viitoare. Vom analiza în continuare relația dintre risc și timp. Ne vom concentra pentru mment pe impactul riscului asupra organizării judicioase a consumului și economisirii.

Literature review Înțelegerea comportamentului de consum este probabil una dintre cele mai importante provocări ale macroeconomiei moderne. În acest domeniu s-au înregistrat abordări nenumărate începând cu lucrările lui Modigliani și Brumberg(1954) și Friedman(1957). Aceste dezvoltări se referă la teoria ciclurilor reale de afaceri. Estimările relative la gradul de rezistență la fl uctuațiile consumului pot fi menționate în diferite lucrări. Hall(1988) a menționat o estimare în jurul valorii 10, în timp ce Epstein și Zin (1991) au descoperit valori cuprinse între 1,25 și 5. Un experiment în acest sens a fost realizat de Barsky, Juster, Kimball și Shapiro(1997). Prima analiza formală a economisirilor precuate este datorată lui Leland(1968), Sandmo(1970) și Dreze și Modigliani(1972). Kimball (1990) a fasonat termenul de prudență examinând proprietățile primei de precauție. De-a lungul timpului s-a consolidat o literatură importantă asupra efectului limitărilor de lichiditate în cadrul ratelor optime de economisire. Strotz (1956) a fost primul care a pus în discuție problema consistenței temporale în cazul consumatorilor care folosesc un factor de reducere care nu descrește exponențial cu orizontul de timp. Pollack (1968) a rezolvat problema consistenței temporale utilizând o abordare din teoria jocurilor în care diferiți jucători reprezintă sivariante diferite ale aceluiasi consumator în perioade de timp diferite. Laibson (1997) reexaminează această chestiune pentru a explica diferite aspecte ale piețelor de credit astfel că avem astăzi o vastă literatură asupra “reducerii hiperbolice”. Anghelache şi Anghel (2016, 2014) prezintă instrumentele econometrice utile în analize la nivel micro şi macroeconomic şi instrumentele modelării economico-fi nanciare. Anghelache (2008)este o lucrare de referinţă

Revista Română de Statistică - Supliment nr. 2 / 2017 5

în statistica economică. Anghelache, Anghelache şi Sacală (2016) analizează evoluţia investiţiilor de capital în România. Anghelache, Manole şi Anghel (2015) studiază, prin regresie unifactorială, caracteristicile consumului fi nal, Anghelache, Manole şi Anghel (2015) analizează efectul dinamicii consumului fi nal şi investiţiilor asupra Produsului Intern Brut al României. Anghelache, Manole şi Dumitrescu (2015) evaluează corelaţiile dintre consumul fi nal, venitul brut disponibil şi investiţii.

Metodologie şi date

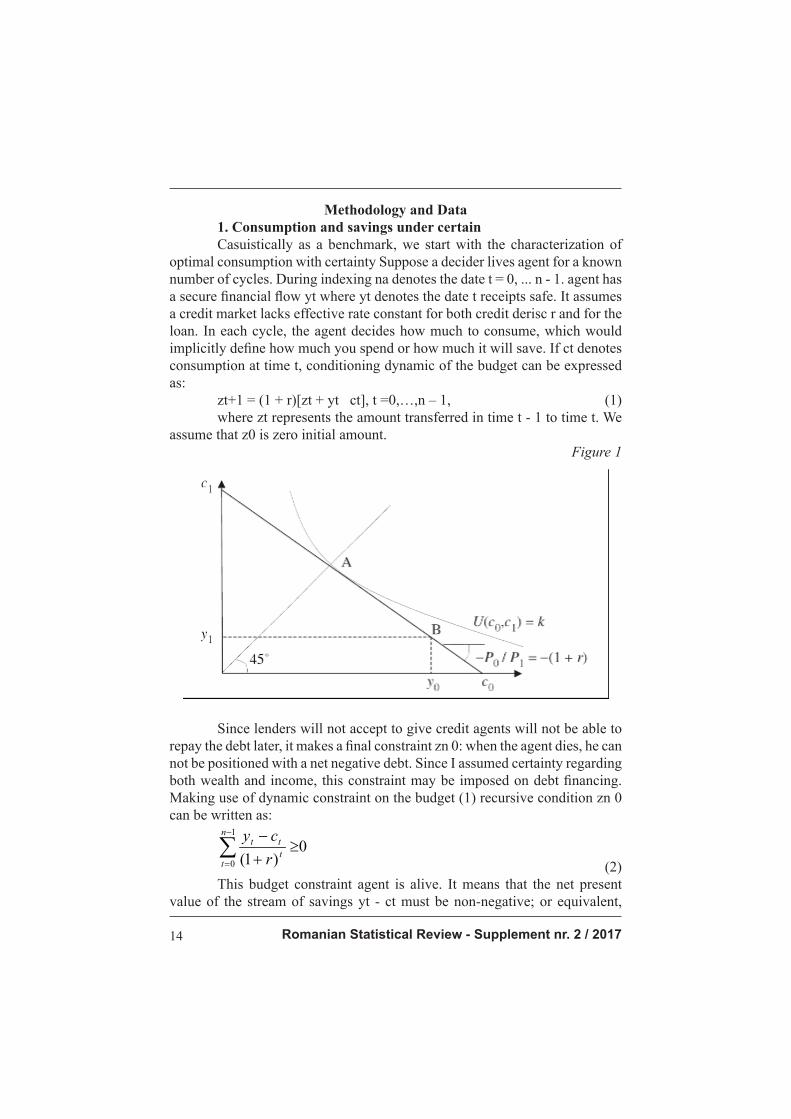

1. Consumul și economisirea în condiții certe

Ca reper cazuistic, vom porni cu caracterizarea consumului optim în condiții de certitudine Să presupunem că un agent decident trăiește pentru un număr cunoscut de cicluri. Denotăm timpul prin indexarea n a datei t = 0,…n - 1. Agentul dispune de un fl ux fi nanciar sigur yt, unde yt denotă încasări sigure la data t. Se presupune existența unei pieți de credit efi ciente cu rată constantă lipsită derisc r atât pentru credit, cât și pentru împrumut. În fi ecare ciclu, agentul decide cât de mult va consuma, ceea ce va defi ni implicit cât de mult va cheltui sau cât va economisi. Dacă ct denotă consumul la data t, condiționarea dinamică a bugetului poate fi exprimată astfel:

zt+1 = (1 + r)[zt + yt ct], t =0,…,n – 1, (1) unde zt reprezintă suma transferată din data t – 1 la data t. Presupunem că suma inițială z0 este zero.

Figura 1

Întrucât împrumutătorii nu vor accepta să acorde credit agenților care nu vor fi în stare să restituie datoria mai târziu, se formulează o constrângere

Romanian Statistical Review - Supplement nr. 2 / 20176

fi nală zn ≥ 0: în cazul în care agentul moare, el nu se poate poziționa cu o datorie negativă netă. Întrucât am asumat certitudinea cu privire atât la avere cât și la venit, această constrângere poate fi impusă pe datoria de fi nanțare. Făcând uz de constrângerea dinamică pe buget în mod (1) recursiv, condiția zn ≥ 0 poate fi scrisă astfel :

0

)1(

1

0∑−

=

≥+

−n

tttt

r

cy (2)

Această constrângere a bugetului agentului este pe viață. Ea semnifi că faptul că valoare netă prezentă a fl uxului de economii yt – ct trebuie să fi e non-negativă ; sau echivalent, că valoarea prezentă a consumului pe viață nu poate depăși valoarea actuală a venitului de-a lungul vieții. Mai direct, putem scrie

∑−

=

Π1

0

n

ttt c

(3)

unde П (1 + r)-t și w0 Пt yt este averea pe viață, de exemplu, valoarea netă prezentă a fl uxului veniturilor. De observat că Пt unui cupon cu valoare zero al unei acțiuni cu scadență la data t, de exemplu, un bun care generează o unitate de lichidități numai la data t. Pentru o valoare dată w0, obiectivul agentului este să aleagă calea de consum optimă (care, la rândul său, va defi ni planul optim de economisire) de-a lungul timpului. Vom descrie în continuare preferințele unui consumator tânăr față de setul tuturor lichidităților posibile de-a lungul vieții. Fie U (c0,c1,…,cn-1) denotând utilitatea pe viață în cazul în care agentul alege planul de consum c = (c0,c1,…,cn-1). Presupunem că funcția U este crescătoare și concavă. Consumul optim se obține prin rezolvarea următorului program:

),...,,(max 110 −n

ccccU . (4)

Această problematică decizională este descrisă în Figura 1 pentru două cicluri investiționale. Acest plan de consum optim este caracterizat în punctul ”A”, unde curba de indiferențăa este tangentă la linia AB a bugetului. Înaintea oricărei discuții privind soluționarea cât mai analitică a acestei probleme, să presupunem că agentul va alege un profi l de venituri (y0,…,yn-1) într-un anume context de oportunitate. Această situație investițională este tipică, având un investitor cu mai multe șanse investiționale, fi ecare cu un fl ux de câștiguri diferit. Structura problemei (4) implică în mode vident faptul că profi lul optim de încasări este cel care maximizează propria valoare netă prezentă (NPV) w0= Пt yt, indiferent de preferințele de consum temporale care îl caraxcterizează pe decident. Acest rezultat este cunoscut ca Teorema Separației a lui Fisher.

Revista Română de Statistică - Supliment nr. 2 / 2017 7

Aceasta susține regula NPV, care este una dintre cele mai importante reguli din ștințele economice : Orice investitor ar trebui să aleagă o investiție care maximizează valoare netă prezentă ΣПt (1 + r)-t a fl uxului fi nanciar. Problema (4) nu este prea diferită de problema deciziei statice a unui agent care consumă n bunuri fi zice într-o teorie clasică a cererii. Proprietățile generale ale acestor funcții sunt binecunoscute. Modelul poate fi îmbogățit cu o propunere legată de preferințele temporale, respectiv introducerea unei axiome care asumă că ordinul preferinței deasupra perechii (c0, c1) nu depinde de modalitatea de consum pentru cele două cicluri n-2, adică, dacă (a,b,c2, …,cn-

1) este preferat lui (d, e,c2, … , cn-1), atunci (a, b, x2, … , xn-1) este preferat lui (d, e, x2, … , xn-1) pentru toți (x2, …, xn-1). Aceasta exclude fenomene precum formarea obiceiurilor de consum. Această presupunere de independență implică faptul că utilitatea funcției U trebuie să fi e separabil, U(c) t (ct), unde ut este utilitatea (intraperioadă) a consumului în momentul t. Pentru a distinge între funcția de utilitate intertemporală U, pe care o numim ut ca ”funcție a fericirii” a consumului la momentul t. O presupunere comună este aceea că funcțiile de fericire sunt echivalente: ut(·)= pt u(·), pentru unele funcții crescătoare și concave u și pentru un scalar pt > 0. Cei mai mulți cercetători au adoptat acest set de presupuneri în ultimii 50 de ani. Păstrând caracterul de generalitate, considerăm p0 ca unitate. Astfel p poate fi interpretat ca o reducere a factorului de fericire u(ct) la momentul t. Dacă pt este mai mic decât unitatea, poate fi interpretat ca pierdere proporțională a utilității cauzată de amânarea consumului, de exemplu, acesta indică o preferință pentru a consuma mai devreme decât mai târziu. Este important să disociem pt, un parametru psihologic, de r, o variabilă fi nanciară. Parametrul pt este folosit ca factor de reducere a fericirii, în timpp ce rata dobânzii r este utilă doar în reducerea fl uxurilor monetare, așa cum s-a văzut anterior. Folosind aceste restricții, putem rescrie problema consumului astfel:

∑−

=

1

0

)(maxn

ttt

ccup subject to 0

1

0

ω=Π∑−

=

n

ttt c

(5)

Condițiile de prim ordin pentru această problem pot fi scrise ca ptu̕ (ct) = ξ Пt pentru t = 0, … n-1 (6) laolaltă cu restrângerea bugetului, unde ξ este multiplicatorul Lagrange asociat cu problema (6.5). Multiplicatorul Lagrage ξ este pur și simplu utilitatea marginal pe viață a unei creșteri a valorii actuale a bunăstării. Această problemă este formal echivalentă cu problema portofoliului static Arrow-Debreu. Înlocuim doar ”stări de natură” cu date, probabilități cu factori de reducere, și ”titluri de valoare” Arrow-Debreu cu cupoane – obligațiuni cu valoare zero. Echivalența are numeroase consecințe pentru ipotezele de lucru.

Romanian Statistical Review - Supplement nr. 2 / 20178

2. Consideraţii privind fl uctuațiile consumului în timp

În primul rând, putem interpreta concavitatea funcției de fericire u în contextul problemei consum-economisire într-o anumită perioadă de timp. Faptul că utilitatea marginală este descrescătoare cu privire la consum generează stimulente pentru decident în sensul unui consum constant în timp. Să considerăm cazul special unde pt = 1 pentru toți t, și cu r = 0, ceea ce implică Пt = 1 pentru toți t. Din condițiile de prim-ordin (6.6) rezultă că u̕ (ct) = ξ pentru fi ecare perioadă, astfel încât calea consumului optim nu manifestă nicio fl uctuație în consum de la o perioadă la alta : ct = w0/n pentru toate valorile lui t. Aceasta este o împrejurare canâplanul de consum optim A este într-o linie de 45° în Figura 6.1.Dacă veniturile fl uctuează de-a lungul vieții consumatorului, strategia optimă de economisire constă în a economisi orice venit suplimentar peste w0/n, sau să împrumute bani în cazurile în care câștigurile din ciclu sunt mai mici decât w0/n. Concavitatea lui u implică faptul că condițiile de ordin secund sunt satisfăcute, astfel că utilitatea de-a lungul întregii vieți este maximizată prin consumul unei cantități egale în fi ecare perioadă. Astfel, dacă u ar fi convex, această soluție ar genera o utilitate minimă pe viață și este ușor de arătat că utilitatea maximă este realizată prin consumul dintr-un singur ciclu investițional. Concluzionăm că atunci când nu există nerăbdare (pt = 1), și rata dobânzii este zero (r = 0), fi ind situația optimă când poți uniformiza consumul dacă funcția de fericire este concavă. Astfel, presupunerea u̕ ̕ < 0 exprimă o aversiune față de fl uctuațiile consumului de-a lungul ”stărilor naturale” din problema portofoliului static Arrow-Debreu. În ultimul model, acesta implică faptul că asigurarea completă este optimă când prețurile bunurilor egalează probabilitatea fi ecărei stări. Se poate măsura intensitatea dorinței de a uniformiza consumul în timp considerând situația în care nu există o piață de credite, astfel că ct = yt. Să presupunem că venitul y0 la momentul 0 este strict mai mic decât venitul y1 la momentul 1. Întrucât utilitatea marginală a consumului este mai mare la termenul 0 decât la momentul 1, u̕ (y0) 1), știm că agentul nu va dori să schimbe o unitate de consum de astăzi pe o unitate de consum de mâine. Acordul privind un asemena model de înțeleger, ar duce la creșterea diferenței dintre consumul la moment 0 și momentul 1, și i-ar reduce utilitatea generală. Interogat în legătură cu sacrifi carea unei unități de consum în acest moment, agentul decident va cere mâine mai mult decât o unitate de consum pentru ziua următoare în calitate de compensație. O modalitate de a măsura intensitatea acestei rezistențe pentru a negocia consumul actual pentru consumul următor constă în defi nirea unei compensații suplimentare k > 0, consum care ar trebui acordat agentului la momentul 1 cu scopul de a micșora pierderea în consum la momentul zero. Considerând pierderile în consum ca fi ind sufi cient de mici, k este defi nit astfel

Revista Română de Statistică - Supliment nr. 2 / 2017 9

u̕(y0) = (1 + k)u̕ ( y1). Partea stânga a acestei egalități reprezintă costul marginal al reducerii consumului astăzi, în timp ce partea dreaptă reprezintă benefi ciul marginal al creșterii viitoare a consumului prin factorul 1 + k. Altfel spus, k poate fi defi nit astfel încât pierderea de utilitate marginalăprin renunțarea la o unitate de consum la momentul 0 trebuie să egaleze creșterea marginală a utilității prin adăugarea lui 1+k unități de consum la momentul 1.Dacă y1 este apropiat de y0,am putea folosi expansiunea Taylor de prim-ordin u̕ (y0) apropiată de y1 pentru a obține

−−≅

)('

)(''

1

11

1

01

yu

yuy

y

yyk

(7).

Rezistența față de substituirea intertemporală este aproximativ proporțională cu rata de creștere a consumului. Factorul de multiplicare, (y) = -yu̕̕ ̕(y)/u̕(y) mai este numit și măsura aversiunii față de fl uctuația relativă, sau grad relativ de rezistență la substituirea intertemporală a consumului. Evident,

(y) este similare cu măsura aversiunii relative față de risc a modelului Arrow –Pratt. Ambele evaluează descreșterea procentului utilității marginale privitoare la o minoră creștere procentuală a bunăstării, respectiv a consumului. În mod curent, o putem considera o măsură locală a aversiunii consumatorului față de amânarea consumului de la o dată sau moment cu consum scăzut către una cu consum ușor mărit. În acest sens, trebuie acordată o atenție mai mare estimărilor empirice ale lui (y), considerat undeva între 1 și 5.

3. Consumul în condiții de certitudine – sporirea optimă

În principiu, rata reală a dobânzii nu este zero, ceea ce alimentează neliniștea agenților decidenți. Să presupunem că consumatorii fac apel la principiu de discount exponențial, p1 =

t, pentru scalarul mai mic decât 1. Aceasta presupune un randament al ratei preferinței pure la momentul prezent de

(1 / pozitiv ca valoare. Altfel spus, -1 și rata fericirii u(ct) multiplicată cu t este echivalent cu scăderea fericirii la o rată constantă pentru perioada de timp respectivă. Utilizarea unei rate constante a reducerilor ulterioare ale utilităților este importantă pentru deciziile consumatorului privind consistența temporală, așa cum se va vedea în continuare. Nerăbdarea și un profi t pozitiv în economisire are două rațiuni echilibrante astfel încât să nu se uniformizeze consumul de-a lungul timpului. Un nivel înalt de nerăbdare, sau un mai înalt, provoacă agenților nevoia de a consuma mai devreme ca timp. Cu alte cuvinte, nerăbdarea tinde să pună la îndoială preferințele în favoarea căilor de consum care descresc în timp. Aceste două efecte contradictorii trebuie combinate cu aversiunea față de

Romanian Statistical Review - Supplement nr. 2 / 201710

fl uctuațiile consumului, în scopul obținerii unei caracterizări optime a creșterii consumului în condiții de siguranță. Exemplifi căm rezolvând analitic această problemă în cazul special în care funcția de fericire prezintă un grad relativ constant de aversiune față de fl uctuațiile consumului. Folosind analogia cu modelul Arrow-Debreu, obținem soluția ct = c0 a

t (8) unde

γ

δ

/1

1

1

++

=r

a

iar c0 este un consum inițial ales pentru a satisface constrângeri ale bugetului la nivelul întregii vieți. Astfel, când reducerea psihologică este exponențială, iar aversiunea relativă este constantă, pentru consumator este cel mai bine să mențină creșterea consumului la o rată constant g, unde

γδ

δ

γ−

≅−

++

≡rr

g 11

1/1

(9)

Aproximarea este mai apropiată când nu diferă prea mult de r. Rata de creștere optimă a consumului este pozitivă atunci când este mai mare decât . Această proprietate se menține independent de precizarea funcției de fericire. Acesta este cazul în caremotivul speculativ în facvoarea economisirii domină efectul de nerăbdare. Observă aici și efectul intuitiv al aversiunii față de fl uctuații : o creștere a lui reduce rata creșterii optime a consumului în timp. Dar, este optim Pentru echilibrarea completă a consumului de-a lungul întregii vieți numai atunci când r= , așa cum s-a întâmplat atunci când am avut r = .

Concluzii

În lumea reală, creșterea consumului este arondată ciclurilor de afaceri, care pun presiune pe fl uctuația consumului în timp. Acesta a fost subiect de dezbatere în ultimii 30 ani. Acest ciclu s-a dovedit a avea impact negativ asupra bunăstării. Obligând-o să se restrângă, prin egalizarea ciclurilor productive, am avantaja consumatorul căruia îi displac oricum fl uctuațiile consumului de la rata de creștere optimă g. In 1987, Lucas arata ca importanta efectului indus de ciclul de afaceri asupra bunastarii a fost mult supraevaluata de specialisti. Se poate masura costul ciclului de afaceri prin reducerea ratei de crestere a consumului pe care reprezentantul agentului ar accepta-o in schimbul eliminarii complete a ciclului de afeceri. Utilizand informatiile privitoare la fl uctuatiile consumului din SUA, Lucas arata ca ”pretul” ciclurilor de afaceri consta intr-o reducere cu mult mai putin decat o zecime dintr-un procent al ratei de crestere anuala a economiei SUA, ceea ce este total nesemnifi cativ.

Revista Română de Statistică - Supliment nr. 2 / 2017 11

Motivul este simplu : la fel ca si in cazul aversiunii fata de risc avem de a face cu un efect de ordin secund al modelului aditional EU, aversiunea fata de fl uctuatiile consumului fi ind un efect de ordin secund prezent in modelul care

se adauga in dimensiunea temporala a modelului. Cu alte cuvinte consumatorii

au o aversiune extrem de scazuta fata de fl uctuatiile mici ale consumului.

Lucas concluziona ca economistii ar trebui sa se preocupe, mai degraba, de

caracteristicile cresterii pe termen lung decat de reducerea volatilitatii.

Bibliografi e

1. Anghelache, C., Anghel, M.G. (2016). Econometrie generală. Concepte, teorie şi

studii de caz, Editura Artifex, Bucureşti

2. Anghelache, C., Anghelache, G.V., Sacală, C. (2016). Aspecte generale privind

evoluţia investiţiilor de capital în România / General Aspects on Developments in

Equity Investments in Romania, Romanian Statistical Review Supplement, Issue

4/2016, pg. 74-82/83-90

3. Anghelache, C., Manole, A., Anghel, M.G. (2015). Unifactorial Econometric

Model - Connection between the Final Consumption and the Private Consumption,

Asian Academic Research Journal Of Social Science & Humanities, Volume 2,

Issue 6, November 2015, pp. 212-219

4. Anghelache, C., Manole, A., Dumitrescu, D. (2015). The Correlation between Final

Consumption, Gross Available Income and Gross Investment: An Econometric

Analysis, International Journal of Academic Research in Accounting, Finance and

Management Sciences, Volume 5, No. 4, October 2015, pp. 84-88

5. Anghelache, C., Manole, A., Anghel, M.G. (2015). Analysis of fi nal consumption

and gross investment infl uence on GDP – multiple linear regression model,

Theoretical and Applied Economics, No. 3/2015 (604), Autumn, pg 137-142

6. Anghelache, C., Anghel, M.G. (2014). Modelare economică. Concepte, teorie şi

studii de caz, Editura Economică, Bucureşti

7. Anghelache, C. (2008). Tratat de statistică teoretică şi economică, Editura

Economică, Bucureşti

8. Cummins, J., Hassett, K., Oliner, S. (2006). Investment Behavior, Observable

Expectations, and Internal Funds, American Economic Review 96, no. 3, pp. 796-810

9. Deaton, A. (1991). Saving and liquidity constraints, Econometrica, 59

10. Dornbusch, R., Fischer, S., Startz, R. (2007). Macroeconomie - traducere, Editura

Economică, Bucureşti

11. Epstei, L.G., Zin, S.. (1991). Substitution, risk aversion and temporal behaviour

of consumption and assets returns: an empirical framework, Journal of political

economy, 99

12. Greenwood, R., Shleifer, A. (2014). Expectations of Returns and Expected

Returns, Review of Financial Studies 27, no. 3, pg. 714-746

13. Kimball, M.S. (1990). Precautionary cavings in the small and in the large,

Econometrica 58

14. Rampini, A.A., Viswanathan, S. (2010). Collateral, risk management, and the

distribution of debt capacity, Journal of Finance 65, 2293–2322

Romanian Statistical Review - Supplement nr. 2 / 201712

SIGNIFICANT ISSUES ON CONSUMPTION AND SAVING

Prof. Alexandru MANOLE PhD.

„ARTIFEX” University of BucharestAssoc. prof. Madalina-Gabriela ANGHEL PhD.

„ARTIFEX” University of BucharestGeorgiana NIȚU PhD. Student

Bucharest University of Economic Studies

Abstract

In this article, the authors analyze some aspects of correlation between consumption and savings. Consumption and savings are addressed to certain conditions, fl uctuation in time of consumption, the possibilities of increasing

consumption in optimally with certainty. The models presented are described

in detail and commented.

Between saving and consumption whole dynamic menus subjective

human behavior that oscillates between purchasing goods and securities

and preservation in some form of money. In one form or another, for the

acquisition of securities or shares, beyond the commercial character of the

action, signifi es still investing in securities with appropriate amount of money,

which ultimately represents her papers invested with a certain value and

inevitably and signifi cance.

These two aspects of the dynamics of decision-makers form part of

the spring while important in shaping behavior subjective decision-maker.

Removing the initial act of modeling out of time, by considering the approach

decision to run a single time, they set the rules of mathematical modeling

behavior decision in a static framework, subject only action of a number of

variables, which are as less under the sway of subjectivity and as much below

the obictivităţii.

Keywords: certainty, decision, consumption, saving resources JEL Classifi cation: E20, E21

Introduction

Until now, we assumed that the decision maker only covers one cycle. This perspective obscures important intertemporal dimension of risk. In real life, agencies can postpone the risk for later. Indeed, the ability to defer risky choices increase the value of their own choosing, usually called “value real choice.” Policy makers can choose to share the possible gains and losses in the current elections that we have done several times and cycles, which becomes

Revista Română de Statistică - Supliment nr. 2 / 2017 13

a kind of temporal diversifi cation of risk effects on fi nal consumption.

Alternatively, they can hope to recover some of the losses current assuming

additional risks in the future. In the extreme, this strategy can lead to “assume

your total loss”, as a player from Las Vegas to bet the little money available in

a fi nal and ultimate bet, hoping to recoup the massive losses suffered. Finally,

agencies can change levels of consumption and saving pending planned future

confrontation with uncertainty and to save a little more in the earlier phases

as a kind of protection against future risks. We will continue to analyze the

relationship between risk and time. Mment we will focus on the impact of risk

on the organization judicious consumption and saving.

Literature review

Understanding consumer behavior is probably one of the most

important challenges of modern macroeconomics. In this area there have been

numerous approaches from the works of Modigliani and Brumberg (1954)

and Friedman (1957). These developments relate to real business cycle theory.

Estimates relating to the degree of resistance to fl uctuations in consumption can

be mentioned in various papers. Hall (1988) mentioned an estimate around 10,

while Epstein and Zin (1991) found values between 1.25 and 5. An experiment

in this regard was made by Barsky, Juster, Kimball and Shapiro ( 1997). Precu

fi rst formal analysis of savings is due to Leland (1968), Sandmo (1970) and

Drez and Modigliani (1972). Kimball (1990) examining fashioned term care

premium properties caution. Over time it has consolidated a signifi cant literature

on the effect of liquidity constraints in the optimal rates of saving. Strotz (1956)

was the fi rst to put the issue of temporal consistency for consumers using a

discount factor that decreases exponentially with time horizon. Pollack (1968)

solved the problem using a temporal consistency from game theory approach in

which different players of the same consumer is different sivariante in different

periods. Laibson (1997) review this issue to explain different aspects of the credit

markets so that we have today is a vast literature on “reducing hyperbolic”.

Anghelache and Anghel (2016, 2014) presents econometric tools

useful in micro and macro level analyzes and modeling economic and

fi nancial instruments. Anghelache (2008) is a work of reference in economic

statistics. Anghelache, Anghelache Jackal (2016) analyzes the evolution of

capital investment in Romania. Anghelache, Manole and Anghel (2015)

study, regression unifactorial, fi nal consumption characteristics, Anghelache,

Manole and Anghel (2015) analyzes the growth rate of fi nal consumption

and investment on Romania’s Gross Domestic Product. Anghelache, Manole

Dumitrescu (2015) evaluated the correlation between fi nal consumption, gross

disposable income and investments.

Romanian Statistical Review - Supplement nr. 2 / 201714

Methodology and Data

1. Consumption and savings under certain

Casuistically as a benchmark, we start with the characterization of optimal consumption with certainty Suppose a decider lives agent for a known number of cycles. During indexing na denotes the date t = 0, ... n - 1. agent has a secure fi nancial fl ow yt where yt denotes the date t receipts safe. It assumes

a credit market lacks effective rate constant for both credit derisc r and for the

loan. In each cycle, the agent decides how much to consume, which would

implicitly defi ne how much you spend or how much it will save. If ct denotes

consumption at time t, conditioning dynamic of the budget can be expressed

as:

zt+1 = (1 + r)[zt + yt ct], t =0,…,n – 1, (1)

where zt represents the amount transferred in time t - 1 to time t. We

assume that z0 is zero initial amount.

Figure 1

Since lenders will not accept to give credit agents will not be able to

repay the debt later, it makes a fi nal constraint zn 0: when the agent dies, he can

not be positioned with a net negative debt. Since I assumed certainty regarding

both wealth and income, this constraint may be imposed on debt fi nancing.

Making use of dynamic constraint on the budget (1) recursive condition zn 0

can be written as:

0)1(

1

0

∑−

=

≥+

−n

tttt

r

cy

(2)

This budget constraint agent is alive. It means that the net present

value of the stream of savings yt - ct must be non-negative; or equivalent,

Revista Română de Statistică - Supliment nr. 2 / 2017 15

the present value of lifetime consumption can not exceed the current value of income throughout life. More directly, we can write

∑−

=

Π1

0

n

t

tt c (3)

where П (1 + r) t and w0 Пtyt life is wealth, for example, net present

value of the income stream. Note that Пt a coupon of zero value of an action

with maturity date t, for example, a good generating unit cash only at the time

t. For a given value w0, the objective of the agent is to choose the path of

optimal consumption ( which in turn will defi ne the optimum plan savings)

over time.

Let me outline a consumer preference towards younger set of all

possible liquidity throughout life. Let U (c0, c1, ..., cn-1) denoting usefulness

life when choosing the agent consumption c = (c0, c1, ..., cn-1). Suppose U is

increasing and concave function. Optimal consumption is obtained by solving

the following schedule:

),...,,(max 110 −nc

cccU (4)

This issue is described JV decision Figure 1 for two investment cycles.

This plan is characterized optimal consumption point “A”, where indiferenţăa

curve is tangent to the budget line AB.

Before any discussions about resolving this problem as analytical,

suppose the agent will choose a profi le of income (y0, ..., yn-1) in a particular

context of opportunity. This investment is typical investor with an investment

of more chances, each with a different stream of earnings. Problem structure

(4) Vident mode implies that the optimal revenue profi le is one that maximizes

the net present their own value (NPV) w0 = Пtyt, regardless of consumer

preferences caraxcterizează time that the decider. This result is known

as Fisher’s separation theorem. It supports NPV rule, which is one of the

most important rules of economic ştinţele: Any investor should choose an

investment that maximizes the net present value ΣПt (1 + r) -t fi nancial fl ow.

The problem (4) is not too different from static decision problem of an

agent who consume physical goods in a classical theory of demand. The general

properties of these functions are well known. The model can be enriched with

a proposal on time preferences, namely the introduction of an axiom which

assumes that the order of preference top pair (c0, c1) does not depend on how

consumption for two cycles n-2, that is, if (a, b, c2, ..., cn-1) is preferred to (d,

e, c2, ..., cn-1), then (a, b, x2, ..., xn-1) is preferred to (d, e, x2, ... , xn-1) for

Romanian Statistical Review - Supplement nr. 2 / 201716

all (x2, ..., xn-1). This excludes phenomena such as the formation of behavior. This assumption of independence implies that the utility function U must be separable, U (c) t (ct), where ut is the utility (intraperioadă) consumption at time t. To distinguish between the utility function intertemporal U, which call ut as a “function of happiness” of consumption at time t. a common assumption is that the functions of happiness are equivalent: ut (·) = pt u (·) for some functions increasing and concave u and scalar pt 0 . Most researchers have adopted this set of assumptions in the last 50 years. Keeping the character of generality, we consider p0 as a unit. Thus p can be interpreted as a reduction factor fericireu (ct) at time t. If pt is less than unity, can be interpreted as a loss proportional to the utility due to the postponement of consumption, for example, it indicates a preference for eating sooner than later. It is important to separate for a psychological parameter, r, a fi nancial variable. The parameter

is used for the happiness factor reduction in the interest rate r timpp is only

useful in reducing monetary fl ows, as seen above.

Using these restrictions, we can rewrite consumption problem as

follows:

∑−

=

1

0

)(maxn

t

ttc

cup

subject to 0

1

0

ω=Π∑−

=

n

t

tt c

(5)

The fi rst order conditions for this problem can be written as

PTU (ct) = ξ Пt for t = 0, ... n-1 (6)

together with the tightening budget, where ξ Lagrange multiplier

associated with the problem (6.5). Lagrage multiplier ξ is simply marginal

utility increases the life of the present value of welfare.

This problem is formally equivalent to Arrow-Debreu static portfolio

problem. Just replace “state of nature” with data, probabilities with reduction

factors, and “securities” Arrow-Debreu coupons - bonds with zero. Equivalence

has many consequences for the working assumptions.

2. Considerations regarding consumption fl uctuations while

First, we can interpret the concavity function u happiness in the context

of consumption-saving problem in a certain period of time. That is decreasing

marginal utility of consumption generates incentives for the decider in terms

of a constant consumption over time. Let us consider the special case where

pt = 1 for all t, and r = 0, which implies Пt = 1 for all t. Since the conditions

of fi rst-order (6.6) that u (ct) = ξ for each period so optimal consumption path

that do not show any fl uctuation in consumption from one period to another:

ct = w0 / n for all values of t. This is a circumstance canâplanul optimal

Revista Română de Statistică - Supliment nr. 2 / 2017 17

consumption is a line in Figure 6.1.Dacă income 45" fl uctuates lifelong

consumer saving optimal strategy is to save any extra income over w0 / n, or

borrow money in the cycle where earnings are lower than w0 / n. Concavity

of u implies that second order conditions are satisfi ed, so that utility-long

learning is maximized by eating an equal amount in each period. So if u would

be convex, this approach would be a minimum useful life and it is easy to

show that maximum utility is achieved by use of a single investment cycle. We

conclude that when there is forward (pt = 1), and the interest rate is zero (r =

0), the optimal situation if you can even out consumption function is concave

happiness. Thus, the assumption U ̕ 0 expresses an aversion to fl uctuations

in consumption over the “natural state” of the Arrow-Debreu static portfolio

problem. In the last model, it implies that comprehensive insurance is optimal

when the prices of goods equals the probability of each state.

It can measure the intensity of the desire to equalize consumption

while considering the situation in which there is no market for loans, so ct =

yt. Suppose y0 income at time 0 is strictly less than the income at the time Y1

1. Since the marginal utility of consumption is higher than when the deadline

0 1 u (y0) 1), we know that the agent will not like to change today a unit of

consumption per unit of consumption tomorrow.

Agreement on such a model of understanding, would increase the

consumption time difference between 0 and 1 moment, and would reduce the

overall usefulness. Questioned about the killing unit of consumption at this

time, the agent decider tomorrow will require more than a consumer unit for

the following day in compensation. One way to measure the strength of this

resistance to negotiate the current consumption for the next intake is to defi ne

additional compensation k> 0, the consumer should be granted when one

agent in order to minimize the loss in consumption at time zero. Considering

losses in consumption is suffi ciently small k is defi ned as

u̕(y0) = (1 + k)u̕ ( y1).

The left side of this equality is the marginal cost of reducing

consumption today, while the right side represents the marginal benefi t of

future growth in consumption by factor 1 + k. In other words, k can be defi ned

so that the loss of utility marginalăprin divest a unit of consumption at time 0

must equal marginal increase his usefulness by adding 1 + k consumer units

when Y1 is close to y0 1. If I use fi rst-order Taylor expansion of u (y0) to get

closer to y1

−−≅

)('

)(''

1

11

1

01

yu

yuy

y

yyk

(7)

Romanian Statistical Review - Supplement nr. 2 / 201718

Resistance to inter-temporal substitution is approximately proportional to the rate of increase in consumption. The multiplication factor, (y) = ̕-Yu (y) /

u (y) is also called the measure aversion fl uctuation relative or relative degree

of resistance to intertemporal substitution of consumption. Obviously, (y) is

similar measure relative to risk aversion Arrow -Pratt model. Both assesses

the percentage decreasing marginal utility with respect to a minor percentage

increase in wealth or consumption. Currently, we can consider a local measure

of consumer aversion to postpone consumption to once or time consuming to

one with low consumption slightly increased. In this regard, attention should

be given greater empirical estimates of (y), considered somewhere between 1

and 5.

3. Consumption with certainty - increase optimal

In principle, the real interest rate is zero, which feeds anxiety

agents makers. Suppose that consumers are calling the discount principle

exponentially, p1 = t for scalar less than 1. This implies a yield of pure

preference rate at the present time (1) / positive value. In other words, -1 and

happiness rate u (ct) multiplied by t is equivalent to happiness decrease at a

constant rate for that time period. Using a constant rate reductions subsequent

utilities is important for temporal consistency in consumer decisions, as will

be seen below.

Impatience and a positive profi t in saving has two balancing reasons so as not to equalize consumption over time. A high level of impatience, or higher, causing agents need to consume earlier that time. In other words, impatience tends to question the ways consumer preference in favor of that decrease over time. These two contradictory effects to be combined with aversion to fl uctuations in consumption, in order to achieve optimal growth

characterizations safe consumption.

Analytical problem solving exemplify this particular function if

happiness presents a constant degree of aversion to fl uctuations in consumption.

Using Arrow-Debreu model analogy, we get the solution

ct = c0 at (8)

where:

γ

δ

/1

1

1

++

=r

a

and c0 is a consumer initially chose to meet budget constraints across

lifetimes. Thus, when the reduction is exponential psychological and relative

Revista Română de Statistică - Supliment nr. 2 / 2017 19

aversion is constant, the consumer is best to keep consumption growth at a constant rate g, where

γδ

δ

γ−

≅−

++

≡rr

g 11

1/1

(9) Approximation is closer when not much different from r. Optimum consumption growth rate is positive when above. This property is maintained independently of happiness accurate function. This is where speculative facvoarea caremotivul saving effect dominates forward. Notice here and intuitive aversion effect of fl uctuations: an increase in the rate of growth

reduces consumption while optimal. But balance is optimal for complete

consumption throughout life only when r =, as happened when I was r =

.

Conclusion

In the real world, consumption growth is ascribed business cycles,

which put pressure on consumption fl uctuation over time. It has been debated

over the past 30 years. This cycle was found to have a negative impact on

well-being. Forcing her to collapse equalization cycles productive, we benefi t consumers whom dislike anyway fl uctuations in consumption growth rate

optimal g. In 1987, Lucas shows that important effect induced business cycle

on welfare has been overrated by specialists . It can measure the business

cycle cost by reducing consumption growth rate that the agent would accept

in exchange for complete elimination cycle afeceri. Using information

concerning fl uctuations of the US consumption, Lucas says that “price”

business cycle consists of a reduction than one-tenth less than one percent of

the annual growth rate of the US economy, which is totally insignifi cant. The reason is simple: the same as for the risk aversion we deal with the effect of second-order model additional EU aversion to fl uctuations in consumption as

a result of second order present in the model plus the temporal dimension of

model. In other words, consumers have an aversion to fl uctuations in extremely

low consumption low. Lucas concluded that economists should be concerned

rather the characteristics of long-term growth than reducing volatility.

Bibliografi e

1. Anghelache, C., Anghel, M.G. (2016). Econometrie generală. Concepte, teorie şi

studii de caz, Editura Artifex, Bucureşti

2. Anghelache, C., Anghelache, G.V., Sacală, C. (2016). Aspecte generale privind

evoluţia investiţiilor de capital în România / General Aspects on Developments in

Equity Investments in Romania, Romanian Statistical Review Supplement, Issue

4/2016, pg. 74-82/83-90

Romanian Statistical Review - Supplement nr. 2 / 201720

3. Anghelache, C., Manole, A., Anghel, M.G. (2015). Unifactorial Econometric Model - Connection between the Final Consumption and the Private Consumption, Asian Academic Research Journal Of Social Science & Humanities, Volume 2,

Issue 6, November 2015, pp. 212-219

4. Anghelache, C., Manole, A., Dumitrescu, D. (2015). The Correlation between Final Consumption, Gross Available Income and Gross Investment: An Econometric Analysis, International Journal of Academic Research in Accounting, Finance and

Management Sciences, Volume 5, No. 4, October 2015, pp. 84-88

5. Anghelache, C., Manole, A., Anghel, M.G. (2015). Analysis of fi nal consumption

and gross investment infl uence on GDP – multiple linear regression model,

Theoretical and Applied Economics, No. 3/2015 (604), Autumn, pg 137-142

6. Anghelache, C., Anghel, M.G. (2014). Modelare economică. Concepte, teorie şi

studii de caz, Editura Economică, Bucureşti

7. Anghelache, C. (2008). Tratat de statistică teoretică şi economică, Editura

Economică, Bucureşti

8. Cummins, J., Hassett, K., Oliner, S. (2006). Investment Behavior, Observable

Expectations, and Internal Funds, American Economic Review 96, no. 3, pp. 796-810

9. Deaton, A. (1991). Saving and liquidity constraints, Econometrica, 59

10. Dornbusch, R., Fischer, S., Startz, R. (2007). Macroeconomie - traducere, Editura

Economică, Bucureşti

11. Epstei, L.G., Zin, S.. (1991). Substitution, risk aversion and temporal behaviour

of consumption and assets returns: an empirical framework, Journal of political

economy, 99

12. Greenwood, R., Shleifer, A. (2014). Expectations of Returns and Expected

Returns, Review of Financial Studies 27, no. 3, pg. 714-746

13. Kimball, M.S. (1990). Precautionary cavings in the small and in the large,

Econometrica 58

14. Rampini, A.A., Viswanathan, S. (2010). Collateral, risk management, and the

distribution of debt capacity, Journal of Finance 65, 2293–2322

Revista Română de Statistică - Supliment nr. 2 / 2017 21

Precauţiunea economisirii în condiţii de incertitudine

Prof. univ. dr. Constantin ANGHELACHE

Academia de Studii Economice din București

Universitatea „ARTIFEX” din București

Conf. Univ. Dr. Aurelian DIACONU

Universitatea „ARTIFEX” din București

Drd. Emilia STANCIU

Academia de Studii Economice din București

Abstract

Problema certitudinii, a siguranței care infl uențează comportamentul decidentului, reprezintă un aspect cu dublă determinare: subiectivă și obiectivă. Într-o perspectivă temporală largă cu referire la orizontul integral al vieții decidentului, aspectele legate de factorii care constrâng sau relaxează comportamentul decizional se adună sub arcul de defi niție subiectivă al rezistenței și aversiunii față de fl uctuațiile consumului, dar și față de risc, devenit astfel parte din cadrul decizional subîntins întregii vieți a decidentului. Raportul dintre consum și siguranța decizională reprezintă un factor care asigură creșterea sau, după caz, descreșterea consumului. În momentul în care se instalează condiții de nesiguranță, decidentul va înclina comportamental către economisire, în ideea asigurării unei anumite fl uențe a consumului în timp, dar și a propriei existențe. Ideea unui comportament precaut nu ii este străină decidentului în asemenea circumstanțe, dar nici aceea a economisirii riscante, subiect necesar de defi nit și clarifi cat. Cuvinte cheie : venit, incertitudine, economisire, planifi care, consum Clasifi care JEL : E20, E21

Introducere

Presupunerea conform careia consumatorii au un venit constant este, in mod evident, o supozitie nerealista. Astfel, suntem nevoiti sa introducem nesiguranta in acest tablou general. Consumatorul ar putea planifi ca stiind ca

viitorul lui castig din munca este supus unor schimbari iar acesta ar putea fi

mai mare sau mai mic decat anticipase anterior.

Incertitudinea care afecteaza veniturile viitoare aduce un nou

motiv pentru a economisi. Banuiala este ca aceasta pune presiune asupra

consumatorilor sa creasca acumularea de bunastare tocmai pentru a se pregati

sa infrunte un risc viitor. Acesta este asa-numitul motiv de precautie pentru

economisire si el consta intr-un comportament prudent de consum.

Romanian Statistical Review - Supplement nr. 2 / 201722

1. Noţiuni generale introductive

Sa consideram un model simplu cu doua termene temporale cu un venit sigur y0 in perioada 0, dar un venit y͠1 in a doua perioada de timp. Sa presupunem ca acest risc are natura exogena. Consumatorii aleg cat de mult sa economiseasca la data 0 tocmai pentru a maximiza utilitatea asteptata de-a lungul vietii

asteptata de-a lungul vietii

1100~)1(()()(max ysrEusyusV

c

Dupa cum putem observa, nu avem nevoie sa presupunem la acest nivel ca

~

Dupa cum putem observa, nu avem nevoie sa presupunem la acest nivel ca u1 este egal cu u0. Sa consideram economisirea optima in conditii de nesiguranta prin s*. Conditia de prim ordin pentru s* este scrisa astfel :

)~*)1((')1()( 11

*

00' ysrEursyu

De observat ca dorinta de a economisi este determinata de utilitatea marginala asteptata pentru consumul viitor. Fundamentarea teoretica a comportamentului prudent de consum poate fi derivata prin compararea lui s* cu economisirea ŝ unde un anume

venit viitor, nesigur y͠1 este inlocuit cu asteptarea lui :

)~)1(()()(ˆmax 1100 yEsrusyusV

s+++−=

Fie ŝ care denota solutia la acest program de maximizare. Vrem sa

stabilim daca economisirea optima in conditii de nesiguranta este mai mare

atunci cand incertitudinea este indepartata : s* > ŝ . Intrucat V̂ este concav

in s, ceea ce este usor de verifi cat, aceasta se intampla daca si numai daca

V̂’ (s*) este negativ. Aceasta conditie presupune ca reducerea marginala a

economisirii din s* creste utilitatea de-a lungul vietii in conditii de siguranta.

Cu alte cuvinte, va fi o cerere precauta pentru economisire, daca si numai daca

precauta pentru economisire, daca si numai daca

0

)~*)1((')~*)1((')[1(

)~*)1((')1(*)('*)('ˆ

1111

1100

ysrEuyEsrur

yEsrursyusV

unde egalitatea secunda este obtinuta prin utilizarea conditiei de max. De aceea, nivelul

~

unde egalitatea secunda este obtinuta prin utilizarea conditiei de max.

De aceea, nivelul economisirii din motive de precautie este pozitiv daca si

numai daca

)~*)1((')~*)1((' 1111 yEsruysrEu

Din inegalitatea lui Jensen, aceasta rezulta, ori de cate ori ca ori de cate ori Din inegalitatea lui Jensen, aceasta rezulta, ori de cate ori ca ori de cate

ori u’1 este convex sau echivalent, sau echivalent ori de cate ori u’’’1 este pozitiv.

Aceasta conditie este considerata ca ”prudenta”. Astfel, prudenta este necesara

daca vrem ca economisirea precauta sa fi e pozitiva pentru toate distributiile

Revista Română de Statistică - Supliment nr. 2 / 2017 23

posibile ale riscului viitor. Un consumator cu o functie de utilitate marginala concava, dimpotriva, va reduce economisirile din cauza riscului viitor. Acest individ va manifesta ceea ce se numeste ”comportament imprudent”. Astfel, prudenta corespunde pozitivitatii celei de a treia derivate a functiei de utilitate la fel cum aversiunea fata de risc se bazeaza pe negativitatea derivatei secunde. Un agent poate exprima un comportament advers fata de risc si imprudent, de exemplu, asigurandu-si riscul printr-o prima de risc incorecta si reducandu-si economiile fata in fata cu un risc viitor neasigurat. Astfel, conform defi nitilor,

o persoana prudenta ar putea fi considerata iubitoare de risc. Exista o legatura

totusi intre aversiunea de risc descrescatoare si prudenta. Intrucat consideram

aversiunea descrescatoare fata de riscul absolut (DARA) ca pe o supozitie

naturala, la fel ar trebui sa consideram si prudenta.

Am putea sa masuram intensitatea motivului economisirii precaute.

Aceasta se poate face raspunzand la urmatoarea intrebare : ce anume ar putea

sa fi e reducerea sigura a veniturilor viitoare astfel incat sa aiba acelasi efect

asupra economisirilor ca si introducerea riscului viitor? Fie simbolul pentru

”prima de precautie”. Ea este defi nita implicit de

simbolul pentru ”prima de precautie”. Ea este definita implicit de

)(')(' 1111 yEuyEu

este bogatia acumulata inainte de al doilea termen. Aceasta conditie statueaza faptul ca unde w este bogatia acumulata inainte de al doilea termen. Aceasta

conditie statueaza faptul ca dorinta de a economisi, care este masurata de

utilitatea marginala asteptata a consumului viitor, nu este afectata de inlocuirea

riscului prin asteptarea diminuata de . Prima de precautie este vazuta ca fi ind

pozitiva ori de cate ori agentul este prudent. De exemplu ori de cate ori u’’’1 este mai mare ca 0. Este util sa observam la acest nivel al demonstratiei ca

prima de precautie este echivalenta cu prima de risc defi nita anterior, dar unde

functia de utilitatea u1 ar fi inlocuita de functia de utilitate marginala -u’1.

Prima de precautie si prima de risc reprezinta reduceri sigure ale bunastarii

care au aceleasi efecte ca si riscurile adaugate la utilitatea marginala asteptata

si, respectiv, la EU. Aceasta implica faptul ca toate rezultatele pe care le-am

obtinut anterior pentru aversiunea fata de risc si pentru prima de risc pot fi

transferate prudentei si primei de precautie, pur si simplu inlocuind u1 cu -u’1.

Astfel, cineva poate folosi aproximatia Arrow-Pratt pentru prima de

risc pentru a obtine un echivalent unu pentru prima de precautie :

1

~2

1 )(2

1yyEP σωψ +≅

unde P reprezintă gradul de prudenta absoluta. Pentru a vedea modul in care prima de precautie afecteaza economisirea, sa consideram cazul simplu in care rata economisirii neriscante

Romanian Statistical Review - Supplement nr. 2 / 201724

egaleaza rata reducerii pentru preferinta temporala, si le stabilim pe amandoua ca fi ind egale cu 0, de exemplu r= =0. In particular, utilitatea pe viata este

considerata a fi U(c0,c1) = u(c0) + u(c1). Presupunem, de asemenea, Ey͠

1=y0, astfel ca individul are acelasi venit asteptat atat la momentul 0 cat si la

momentul 1. Sa presupunem, mai intai, ca ỹ 1 este neriscant, adica ỹ 1 ỹ 0.

In aceasta formula, conditia de prim ordin (6.11) implica faptul ca u’(y0-s)

= u’(y0+s). Asa cum observam deja rezulta ca economisirea optima este 0,

s*=0, de vreme ce u este strict concava. Cu alte cuvinte, consumatorul pur si

simplu isi consuma venitul curent in fi ecare perioada : c*0 = c*1 = y0.

Acum sa presupunem ca y͠ 1 este riscant, astfel ca conditia de ordin

prim este

)(')~(')(' 010 syusyEEusyu

A doua egalitate de mai sus deriva din defi nita noastra asupra primei

de precautie. Rezolvarea pentru economisirea optima da s*= ½ Astfel,

atunci cand consumatorul este prudent el va manifesta o cerere precauta

de economisiri, s*>0. Mai mult, un individ care este mult mai prudent va

avea o valoare mai mare a primei de precautie , in acelasi mod in care un

individ care o aversiune mai mare fata de risc are o prima de risc mai mare.

Rezulta ca un consumator mai prudent va economisi mai mult decat unul mai

putin prudent. Este foarte interesant de vazut ca daca functia de fericire este

cuadratica ceea ce reprezinta o presupunere mai putin comuna literaturii din

acest domeniu, vom avea = 0, ceea ce inseamna inexistenta unui motiv

de economisire precauta.

Literature review

Anghelache şi Anghel (2016), Anghelache et.al. (2006) descriu

instrumentele statistice utilizate în măsurarea indicatorilor macroeconomici.

Anghelache, Manole şi Anghel (2016) abordează caracteristica de normalitate

asimptotică a estimatorilor de ecuaţie singulară. Anghelache (2016),

Dougherty (2007) se preocupă de conceptele teoretice legate de instrumentele

econometrice, Anghelache, Manole şi Anghel (2015) studiază instrumentele

modelării economice, fi nanciar-bancare şi informatice. Anghelache şi Sacală

(2014) descriu caracteristicile mediului de afaceri românesc prin prisma

investiţiilor de capital. Bloom (2009) evaluează impactul incertitudinii,

Bloom, Bond şi Van Reenen (2007) analizează impactul incertitudinii asupra

investiţiilor, Bolton, Wang şi Yang (2014), Grenadier şi Wang (2007) dezvoltă

pe teme apropiate. Hafner şi Wallmeier (2008) se concentrează pe volatilitate

ca factor de infl uenţă asupra investiţiilor. Itzhak, Graham şi Campbell (2013)

studiază o serie de riscuri de ordin psihologic şi economic care se manifestă

la nivelul managementului. Miles (2009) analizează efectele incertitudinii

Revista Română de Statistică - Supliment nr. 2 / 2017 25

asupra investiţiilor. Salman şi McLee (2014) au în vedere relaţia dintre

investiţia agregată şi sentimentele investitorilor.

2. Corelaţia dintre economisirea riscantă si cererea precaută

Anterior am considerat numai riscul legat de venitul din munca.

Individul avea o alternativa de economisire fara risc dar era nesigur in legatura

cu marimea venitului pe care il va castiga la momentul 1. Avand in vedere un

model in care venitul din munca este cunoscut, dar rata profi tului din economii

este riscanta. Sa consideram un consumator cu un orizont investitional de

doua perioade. In cazul in care venitul de-a lungul vietii este cunoscut cu

certitudine, presupunem fara a pierde caracterul de generalitate ca intregul

venit este platit la data t=0. Presupunem ca w0 denota aceasta bunastare.

Obiectivul consumatorului este

))~1(()()(max 0 srEususV

s

~~

~~

Conditia de ordin prim pentru acest program este

))1((')1()(' 000 srursu

~~

Conditia de ordin secund este mai usor de indicat ca derulandu-se sub

aversiunea fata de risc. In fapt, functia obiectiva V(s) este concava in s.

Sa consideram, in primul rand, cazul in care rata economisirii lipsita

de risc este r0 ca anterior. Conditia de ordin prim in acest caz devine

))1((')1()(' 000 srursu ++=− βω

Concentrandu-ne asupra efectelor riscului consideram inca o data

cazul simplu in care rata de profi t asteptata a economiilor egaleaza rata de

discount pentru preferinta de timp, de exemplu, r= , astfel ca =(1+r0)-1.

Totusi, s* satisface

w0-s*=(1+r0)s*. Asa cum era de asteptat economia optimala s* este astfel

considerata incat nu exista nici o fl uctuatie in consum intre cele doua date :

c*0=c*1. Revenim la chestiunea daca adaugand risc la profi tul din economisiri

se obtine un nivel mai mare de economisire, in aceasta formula rezulta ca

prudenta singura nu este sufi cienta pentru a conduce la o crestere de nivel a

economisirii. In fapt, exista doua infl uente care contribuie la aceasta, pe de

o parte caracterul riscant al profi tului face economisirile mai putin atractive

decat o rata libera de risc cu acelasi profi t mediu. Dar, pe de alta parte, termenul

1 al riscului va induce un motiv de precautie consumatorului prudent. Rezulta

ca avem nevoie de un nivel de prudenta sufi cient de ridicat pentru a avea o

dominatie a motivului de precautie asa cum vom arata in continuare.

De vreme ce V(s) este concav, rezulta ca nesiguranta in rata profi tului

va forta nivelul optim al economisirilor ori de cate ori este satisfacuta relatia :

))1((')1()])~1((')~1[( 00 srursrurE

Aceasta inegalitate se sustine daca functia h(R) Ru’(Rs) este convex in R. Calculul corect arata

Romanian Statistical Review - Supplement nr. 2 / 201726

Aceasta inegalitate se sustine daca functia h(R) Ru’(Rs) este convex in R. Calculul corect arata ca h’’(R)=2su’’(Rs)+s2Ru’’’(Rs). Sa presupunem ca u’’<0 si ca economisirile nu sunt 0, de vreme ce c1 ar fi tot zero, in acest caz.

Rezulta ca h’’>0 daca

ar fi tot zero, in acest caz. Rezulta ca h’’>0 daca

2)(''

)('''

zu

zzu

Partea stanga a ecuatiei este doar o se sustine cu z=Rs. Partea stanga a ecuatiei este doar o masura

a prudentei relative. Astfel, din ecuatia mentionata obtinem urmatoarea

proprietate statica comparativa a unei cresteri a riscului profi tului prin

economii :

Desigur, prudența relativa nu trebuie sa satisfaca conditiile de mai sus. Cu toate acestea, un caz in care ea o face este cel in care functia de fericire este de tipul CRRA, si anume u(c)=c1-γ/(1-γ), unde γ este gradul constant al aversiunii fata de risc. Ne referim la ‘’aversiunea fata de risc’’ si nu la ‘’aversiunea fata de fl uctuatie’’ intrucat ne intereseaza riscul iar nu consumul proiectat in timp intr-o constructie fara risc. In acest caz mentionat calculele arata ca prudenta relativa este egala cu γ+1. In acest caz de preferinta se obtine

3. Continutul si semnifi catia consecvenței temporale

Când modelul conține numai două termene de consum ca mai sus, orice acțiune viitoare poate fi planifi cată în avans la termenul 0 fără posibilitatea de a schimba ceva. La termenul secund, agentul doar consuma ceea ce are in contul sau de economii. Când există mai mult de două termene, ceea ce a fost planifi cat la momentul t=0 poate fi revăzut la momentul t=1. Dacă ai decis la momentul t=0 să cumperi un produs scump pe care ai decis să îl plătești la termenul următor t=1 încă mai poți decide la momentul t=1 să amâni plata pentru a-ți menține nivelul ridicat al consumului. Astfel consumatorii pot să aibă o problemă de consecvență în timp. Să reexaminăm problema raportului dintre consum și economii în condiții de certitudine descrisă în ecuația (6.5)

Revista Română de Statistică - Supliment nr. 2 / 2017 27

unde Пt=(1+r)-t si n 3. La momentul t=0 consumatorul iși planifi că profi lul de consum (c0 ,…, cn-1) pentru restul vieții lui, ceea ce maximizează utilitatea

duratei vieții 0

1

)( ω=∑−

=

n

ot

tt cup care este supusă restricțiilor de buget de-a

lungul vieții 0

1

ω=Π∑−

=

n

ot

tt c . Să ne amintim că pt este factorul folosit pentru a

determina scăderea fericirii la momentele t din ciclul curent. Folosind condiția pentru t=1și t=0, alegerea planifi cată este de forma:

)(')1(

)(' 12

12 cu

pr

pcu

+= .

Această regulă de consum poate fi satisfăcută astfel încât să se cheltuie efi cient banii economisiți la momentul t=0. Anticipând modul în care va cheltui banii economisiți, agentul își determină consumul optim inițial c0. Rezolvând sistemul de ecuații rezultat împreună cu restrângerea de buget, întregul profi l al consumului este selectat astfel: (c0, c1, c2, ... , cn-1) Să considerăm situația generată la momentul t=1. Bunăstarea a fost efectivă prin consumul inițial c0, dar a și crescut pe baza profi tului r din economisire. La momentul t=0, agentul a planifi cat să consume c1 la momentul t=1. Cu toate acestea, el este gata să își reconsidere alegerea. Bunăstarea pentru perioada rămasă poate fi scrisă:

∑−

=−

1

1 )(n

ot

tt cup .

Indexurile parametrilor p și variabilelor c sunt importante în acest moment. În particular trebuie remarcat, că satisfacţia u(c2) care are loc la o perioadă distanță t=1 este micșorată în punctul p1, factorul de micșorare pentru orizontul unei perioade. Maximizând funcția obiectivă cu restrângerea bugetului obţinem:

)1)(( 00

1

1 rcc

n

ot

tt, ceea ce genereaz, ceea ce generează condiția de ordin

prin alegerea actuală: )(')1(

)(' 11

02 cu

pr

pcu

+=

Ecuațiile de mai sus sunt echivalente numai dacă p1/p2=p0/p1. Aceasta echivalează cu o cerere pt=aβt pentru t=0,1,2, sau acea scădere să fi e

Romanian Statistical Review - Supplement nr. 2 / 201728

exponențială. Această terminologie decurge din faptul că echivalentul timp-continuu al acestei funcții de scădere este p(t) = e-δt. Extinderea acestei condiții pentru toate momentele t implică faptul că alegerea de consum optimă c1 se localizează în momentul t=1 și nu este diferită de cea care a fost planifi cată la momentul t=0.

Concluzii

Problema este mult mai complexă atunci când consumatorul nu

folosește condiţia pt=aβt pentru factorii de scădere. Presupunem că p2 este mai

cuprinzător decât relaţia p /p0. Din ecuațiile iniţiale rezultă că nivelul de consum

c1 selectat la momentul t=1 este mai mare decât cel planifi cat la momentul t=0. În acest caz avem o problemă de consistență. Când determină consumul inițial, agentul nu poate avea încredere în el insuși în legătură cu limitarea propriului consum în viitor. Aceasta este tipic pentru comportamentul adictiv: un consumator consideră că este bine pentru el să consume astăzi în funcție de convingerea sa că va renunţa la consum mâine dar când vine ziua de mâine consumatorul descoperă că este bine pentru el să consume, amânând astfel pe mâine decizia de a nu mai consuma în ziua următoare, și așa mai departe. Putem suspecta că un asemenea comportament adictiv se poate extinde și asupra altor produse generând o problemă globală de adicție în consum. Pentru oamenii care au această problemă, planurile de economisire pe termen lung fără posibilitatea de a retrage bani pot să fi e benefi ce în pofi da infl exibilității acestor planuri. Problema consistenței temporale poate explica de ce un număr mare al populației din țările dezvoltate găsește acceptabil să fi nanțeze consumul pe termen scurt cu împrumuturi prin cărți de credit la rate de 20% și încă să păstreze bani în conturi de economie pe termen lung cu rate sub 5%.

Bibliografi e

1. Anghelache, C., Anghel, M.G. (2016). Bazele statisticii economice. Concepte

teoretice şi studii de caz, Editura Economică, Bucureşti 2. Anghelache, C., Manole, A., Anghel, M.G. (2016). Asymptotic Normality for

Single Equation Estimators for Population with Sensitive Instrument, Economica, Scientifi c and didactic journal, Year XXIV, nr. 2 (96), June 2016, pp. 124-130

3. Anghelache, C. (2016). Econometrie teoretică – Ediţia a II-a revizuită, Editura Artifex, Bucureşti

4. Anghelache, C., Manole, A., Anghel, M.G. (2015). Modelare economică, fi nanciar-

bancară şi informatică, Editura Artifex, Bucureşti 5. Anghelache, C., Sacală, C. (2014). The Autochtonous Investments and the Business

Environment, Romanian Statistical Review Supplement no. 10/2014 6. Anghelache, C., Isaic-Maniu, A., Mitruţ, C., Voineagu, V., Dumbravă, M., Manole,

A. (2006). Analiză macroeconomică: teorie şi studii de caz, Editura Economică, Bucureşti

Revista Română de Statistică - Supliment nr. 2 / 2017 29

7. Bloom, N. (2009). The Impact of Uncertainty Shocks, Econometrica 77, no. 3, pg. 623-685

8. Bloom, N., Bond, S., Van Reenen. J. (2007). Uncertainty and Investment Dynamics, Review of Economic Studies 74, no. 2, pp. 391-415

9. Bolton, P., Wang, N., Yang, J. (2014). Investment under uncertainty and the value

of real and fi nancial fl exibility, National Bureau Of Economic Research Working Paper Series issued in October 2014, Cambridge

10. Dougherty, C. (2007). Introduction to Econometrics, Oxford University Press 11. Grenadier, S.R., Wang, N. (2007). Investment under uncertainty and time-

inconsistent preferences, Journal of Financial Economics 84, pp. 2-39 12. Hafner, R., Wallmeier, M. (2008). Optimal investments in volatility, Financial

Markets and Portfolio Management, v. 22, iss. 2, pp. 147-67 13. Itzhak, B.D., Graham, J., Campbell, H.(2013). Managerial Miscalibration,

Quarterly Journal of Economics 128, no. 4, pp. 1547-1584 14. Miles, W. (2009). Irreversibility, Uncertainty and Housing Investment, Journal of

Real Estate Finan Econ, 38, pg. 173–182 15. Salman, A., McLee, Ch. (2014). Aggregate Investment and Investor Sentiment,

Review of Financial Studies 27, no. 11, pg. 3241-3279

Romanian Statistical Review - Supplement nr. 2 / 201730

PRECAUTION OF SAVINGS UNDER UNCERTAIN CIRCUMSTANCES

Prof. Constantin ANGHELACHE PhD.

Bucharest University of Economic Studies, „ARTIFEX” University of Bucharest

Assoc. prof. Aurelian DIACONU PhD.

„ARTIFEX” University of Bucharest

Emilia STANCIU PhD. Student

Bucharest University of Economic Studies

Abstract

The problem of certainty, of safety which infl uences the decision-makers’

behaviour is both subjective and objective. In a wide temporal perspective with

reference to the full horizon of the decision-maker’s life, the aspects related to the

factors that constrain or relax the decisional behavior gather under the umbrella of the

subjective defi nition of resistance and aversion to fl uctuations in consumption, but also

to risk, thus becaming part of the decision framework in the decision maker’s lifetime.

The ratio between consumption and safe decision-making is a factor

that ensures the increase or the decrease in consumption. Under unsafe

conditions, the decision-maker will incline towards a saving behaviour, with the

view to ensuring a certain continuity in consumption, but also with the benefi t of

ensuring his own existence. Neither the idea of a cautious behavior, nor that of

risky saving is foreign to the decision-maker in such circumstances, that being

an issue necessary to defi ne and clarify.

Keywords: income, uncertainty, savings, planning, consumption

JEL Classifi cation: E20, E21

Introduction

The assumption that consumers have a steady income is obviously unrealistic. Thus, we have to introduce uncertainty in this overview. The consumer should be able to plan knowing that his future earnings from work is subject to changes and they could be higher or lower than expected. Uncertainty affecting future income brings a new reason to saving. The supposition is that this puts pressure on consumers to increase the accumulation of wealth in order to prepare to face a future risk. This is the so-called precautionary reason for saving and it consists of a cautious consumer behavior.

1. Introductory general notions

Let us consider a simple model with two time periods with a secure income y0 during a period 0, but an income y͠1 in the second period. Suppose that risk is exogenous.

Revista Română de Statistică - Supliment nr. 2 / 2017 31

Consumers choose how much to save at the time 0 in order to maximize the utility of they expected all along:

���������������� ���������!

������

�

�

�

��

��

As we can notice, we do not need to suppose at this level is that u1 equal to u0. Let us consider s* as optimal saving under uncertain conditions. The fi rst order condition for s* is written as follows:

������������ ��

���

��������� �����

�

�

�

��

Note that the desire to save is determined by the marginal utility of

consumption expected in the future.

Theoretical cautious consumer behaviour can be derived by comparing

s* with savings ŝ , where ŝ a certain insecure future income y͠1 is replaced by

its expectation:

�������������� ���� ���������!

������

�

��

��

Let us consider ŝ as the solution to this maximization program.

We want to establish whether optimal savings under uncertain conditions is

bigger when uncertainty is removed: s* > ŝ . Since V̂ is concave in s, which is

easily verifi able, this happens if and only if V̂’ (s*) is negative. This condition

implies that by marginal decrease in saving of s* , we increase the utility in

the long run, under certain conditions. In other words, there will be a demand

for cautious savings, if and only if:

�

������������������

�����������������

����

����

�

�������

�������

�����������

����������!

��

where the second equality is achieved by using the max condition.

Therefore, the level of savings out of cautious reasons is positive if and only

if:

�������������� ���� ���������� ������

From Jensen’s inequality, this results whenever u’1 is convex or

equivalent, or when u’’’1 is positive. This condition is considered „cautious”.

Thus, caution is needed if we want prudent saving to be positive for all

possible distributions of the future risk. A consumer with a concave function

of marginal utility, on the contrary, will reduce future savings because of the

future risk. This individual will manifest what is called „reckless behavior”.

Thus, caution corresponds to the third derivative’s positivity of the utility

Romanian Statistical Review - Supplement nr. 2 / 201732

function just as risk aversion is based on the second derivative’s negativity. An agent may express an adversary and imprudent behaviour towards risk, for example, by ensuring the risk using an incorrect risk premium and reducing his savings in the case of a future uninsured risk. So, according to defi nition,

a prudent person could be considered a risk-loving person. Yet, there is a link

between decreasing risk aversion and caution. As we consider the decreasing

risk aversion toward absolute risk (DARA) as a natural assumption, we should

consider caution in the same way.

We could measure the intensity of the reason for cautious saving. This