results presentation 1q16

TRANSCRIPT

2 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

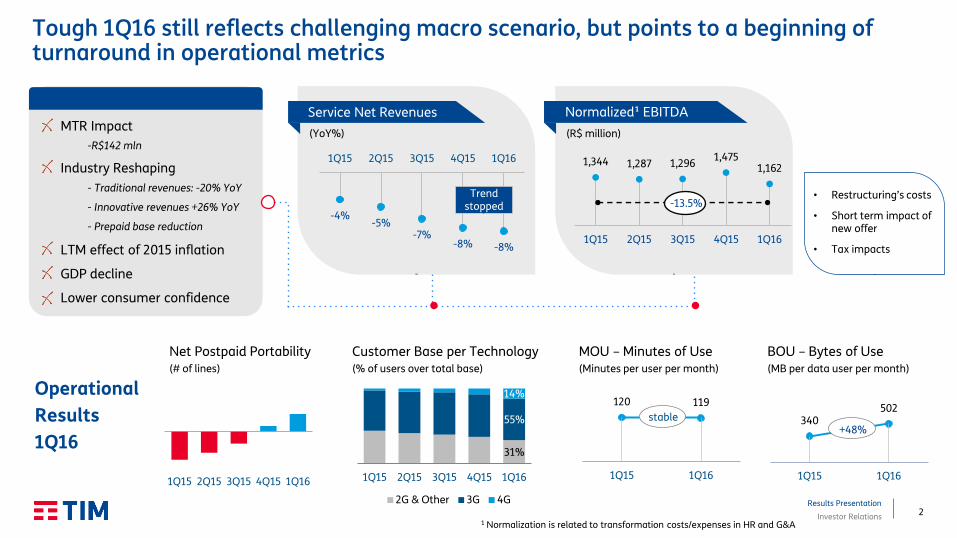

Tough 1Q16 still reflects challenging macro scenario, but points to a beginning of turnaround in operational metrics

Operational

Results

1Q16

Net Postpaid Portability (# of lines)

Customer Base per Technology (% of users over total base)

1 Normalization is related to transformation costs/expenses in HR and G&A

Service Net Revenues

(YoY%) (R$ million)

Normalized¹ EBITDA

MOU – Minutes of Use (Minutes per user per month)

1Q15 2Q15 3Q15 4Q15 1Q16

MTR Impact

-R$142 mln

Industry Reshaping

- Traditional revenues: -20% YoY

- Innovative revenues +26% YoY

- Prepaid base reduction

LTM effect of 2015 inflation

GDP decline

Lower consumer confidence

• Restructuring’s costs

• Short term impact of new offer

• Tax impacts

-4% -5%

-7% -8% -8%

1Q15 2Q15 3Q15 4Q15 1Q16

Trend stopped

1,344 1,287 1,296 1,475

1,162

1Q15 2Q15 3Q15 4Q15 1Q16

-13.5%

BOU – Bytes of Use (MB per data user per month)

120 119

1Q15 1Q16

340 502

1Q15 1Q16

+48% stable

31%

55%

14%

1Q15 2Q15 3Q15 4Q15 1Q16

2G & Other 3G 4G

3 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Fast reaction in multiple fronts, positioned for recovery path

Keep investment focus

+394 new cities with 4G vs. 1Q15

4G leadership position

Increasing customer base value

Off-net to all plans & focus on

mobile bundle

Defending results from tax impact

Actions to offset

ICMS increase

Workforce Restructuring program

Adapting to market reality

Company repositioning

New brand launch: quality,

innovation, customer experience

~10% of customer base in the new

portfolio

Price repositioning to compensate tax

Rightsizing workforce

On track with Efficiency Plan

> R$ 1 bln in efficiency (2015-17)

~40% of program achieved in 1Q16

New phase launched in 2Q16

Infrastructure Offer Portfolio Efficiency Actions Positioning

4 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

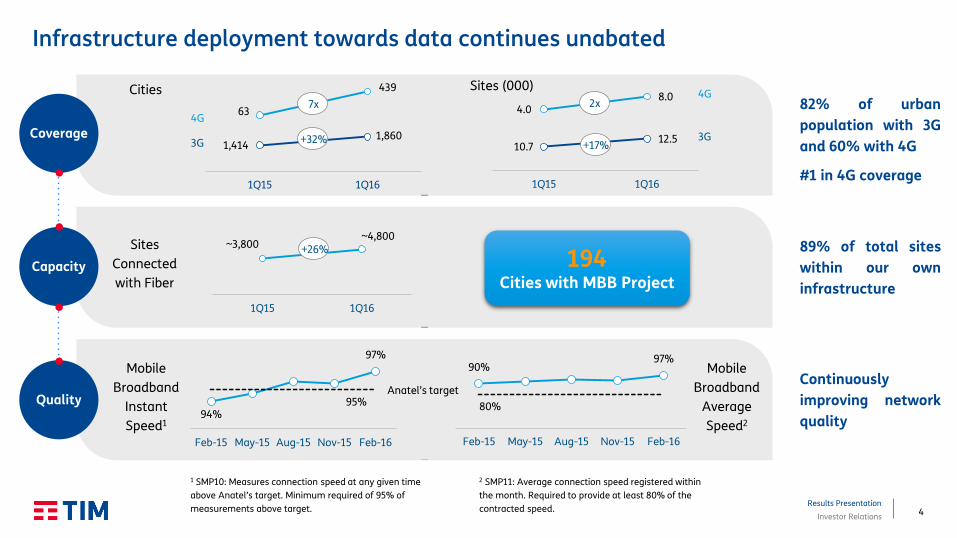

63

439

1,414 1,860

1Q15 1Q16

Infrastructure deployment towards data continues unabated

Coverage

Capacity

Quality

82% of urban

population with 3G

and 60% with 4G

#1 in 4G coverage

89% of total sites

within our own

infrastructure

Continuously

improving network

quality

Sites

Connected

with Fiber

Cities Sites (000)

194 Cities with MBB Project

94%

97%

95%

Feb-15 May-15 Aug-15 Nov-15 Feb-16

90% 97%

80%

Feb-15 May-15 Aug-15 Nov-15 Feb-16

Mobile

Broadband

Instant

Speed1

Mobile

Broadband

Average

Speed2

1 SMP10: Measures connection speed at any given time

above Anatel’s target. Minimum required of 95% of

measurements above target.

2 SMP11: Average connection speed registered within

the month. Required to provide at least 80% of the

contracted speed.

Anatel’s target

+32%

~3,800 ~4,800

1Q15 1Q16

+26%

10.7 12.5

1Q15 1Q16

4G

3G +17%

4G

3G

7x 4.0 8.0

2x

5 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

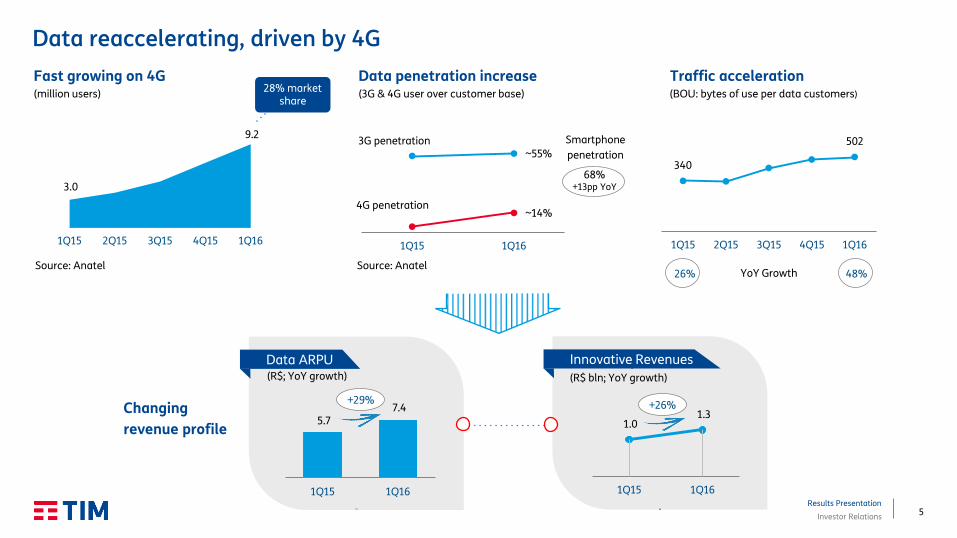

28% market share

Data reaccelerating, driven by 4G

Fast growing on 4G

Changing

revenue profile

Data penetration increase Traffic acceleration (BOU: bytes of use per data customers) (million users)

4G penetration

3G penetration

Innovative Revenues

(R$ bln; YoY growth) (R$; YoY growth)

Source: Anatel

340

502

1Q15 2Q15 3Q15 4Q15 1Q16

26% 48% YoY Growth

(3G & 4G user over customer base)

Source: Anatel

Data ARPU

1.0 1.3

1Q15 1Q16

5.7 7.4

1Q15 1Q16

68% +13pp YoY

Smartphone

penetration

+29% +26%

3.0

9.2

1Q15 2Q15 3Q15 4Q15 1Q16

~55%

~14%

1Q15 1Q16

6 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

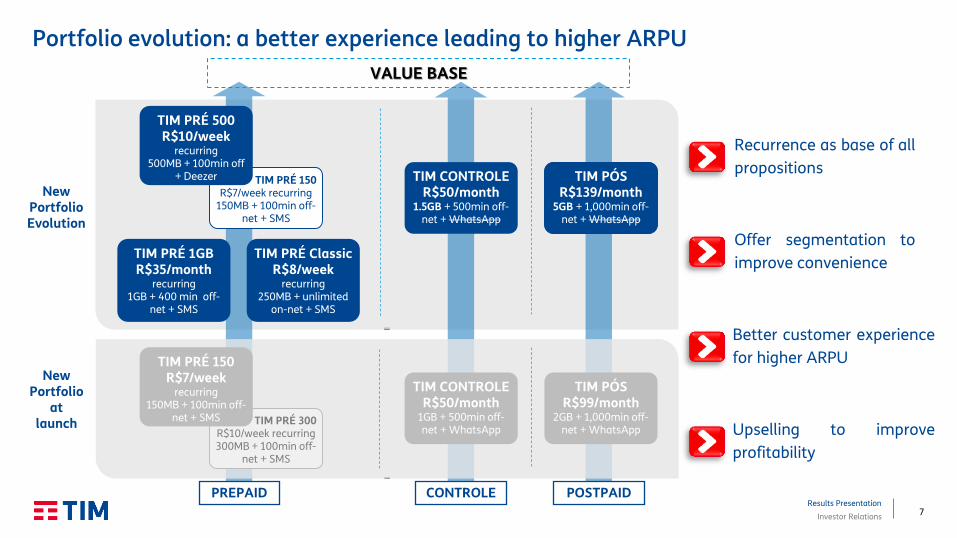

Base New OfferBase New Offer

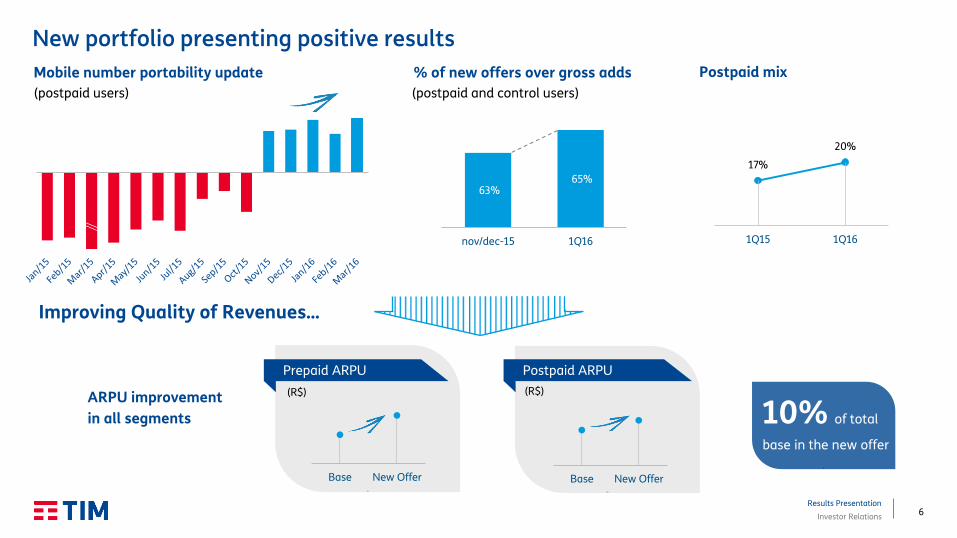

New portfolio presenting positive results

Mobile number portability update

Improving Quality of Revenues…

ARPU improvement

in all segments 10% of total

base in the new offer

% of new offers over gross adds

Prepaid ARPU Postpaid ARPU

(postpaid users)

(R$) (R$)

17%

20%

1Q15 1Q16

Postpaid mix

63% 65%

nov/dec-15 1Q16

(postpaid and control users)

7 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

POSTPAID PREPAID

Portfolio evolution: a better experience leading to higher ARPU

TIM PRÉ 150 R$7/week recurring

150MB + 100min off-net + SMS

TIM PRÉ 500 R$10/week

recurring 500MB + 100min off

+ Deezer

TIM PRÉ Classic R$8/week

recurring 250MB + unlimited

on-net + SMS

TIM PRÉ 1GB R$35/month

recurring 1GB + 400 min off-

net + SMS

CONTROLE

TIM CONTROLE R$50/month

1.5GB + 500min off-net + WhatsApp

TIM PÓS R$139/month

5GB + 1,000min off-net + WhatsApp

Recurrence as base of all

propositions

VALUE BASE

Offer segmentation to

improve convenience

Better customer experience

for higher ARPU

New Portfolio Evolution

TIM PRÉ 300 R$10/week recurring 300MB + 100min off-

net + SMS

TIM PRÉ 150 R$7/week

recurring 150MB + 100min off-

net + SMS

TIM CONTROLE R$50/month

1GB + 500min off-net + WhatsApp

TIM PÓS R$99/month

2GB + 1,000min off-net + WhatsApp

New Portfolio

at launch Upselling to improve

profitability

8 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

1Q15 1Q16

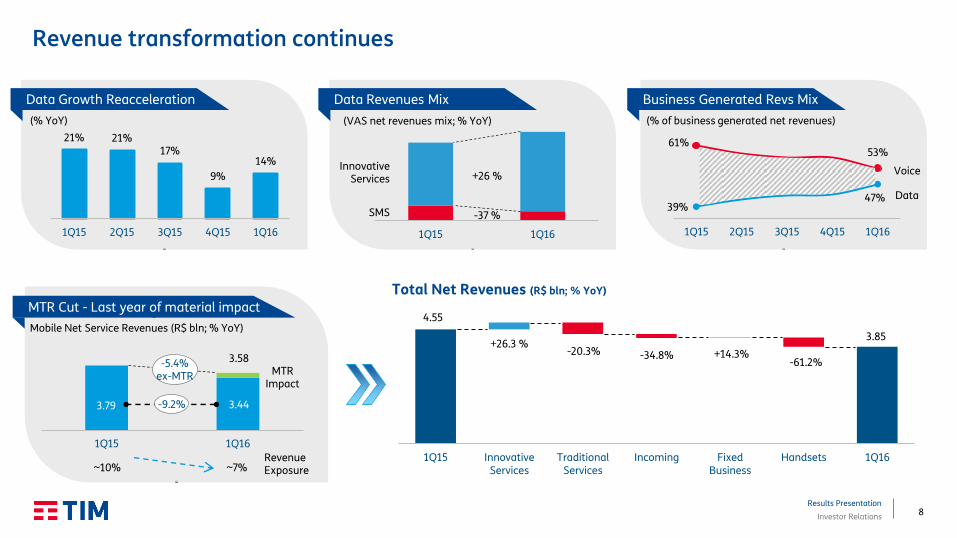

Revenue transformation continues

Business Generated Revs Mix Data Revenues Mix Data Growth Reacceleration

MTR Cut - Last year of material impact

Total Net Revenues (R$ bln; % YoY)

4.55

3.85 +26.3 %

-20.3% -34.8% +14.3% -61.2%

1Q15 InnovativeServices

TraditionalServices

Incoming FixedBusiness

Handsets 1Q16

21% 21% 17%

9%

14%

1Q15 2Q15 3Q15 4Q15 1Q16

(% YoY)

SMS

Innovative Services +26 %

-37 %

Mobile Net Service Revenues (R$ bln; % YoY)

-5.4% ex-MTR

Revenue Exposure

39% 47%

61% 53%

1Q15 2Q15 3Q15 4Q15 1Q16

Data

MTR Impact

Voice

3.79

3.58

3.44

(% of business generated net revenues)

1Q15 1Q16

-9.2%

(VAS net revenues mix; % YoY)

~7% ~10%

9 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

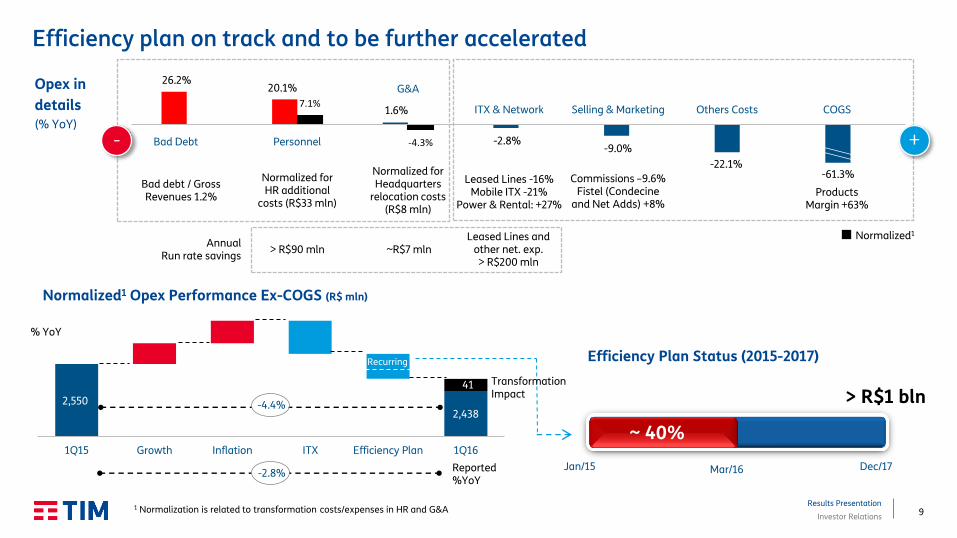

26.2% 20.1%

1.6%

-2.8% -9.0%

-22.1% -61.3%

7.1%

-4.3% Personnel

Efficiency plan on track and to be further accelerated

Normalized1 Opex Performance Ex-COGS (R$ mln)

2,550 2,438

41

1Q15 Growth Inflation ITX Efficiency Plan 1Q16

Efficiency Plan Status (2015-2017)

Jan/15 Dec/17

> R$1 bln

Mar/16

~ 40%

Recurring

% YoY

-4.4%

Reported %YoY

1 Normalization is related to transformation costs/expenses in HR and G&A

-2.8%

Transformation Impact

Normalized for HR additional

costs (R$33 mln)

Opex in

details (% YoY)

Selling & Marketing ITX & Network

G&A

COGS

Bad Debt

Commissions –9.6% Fistel (Condecine

and Net Adds) +8%

Leased Lines -16% Mobile ITX -21%

Power & Rental: +27%

Normalized for Headquarters

relocation costs (R$8 mln)

Products Margin +63%

Bad debt / Gross Revenues 1.2%

Normalized1

-

> R$90 mln Annual

Run rate savings ~R$7 mln

Leased Lines and other net. exp. > R$200 mln

+

Others Costs

10 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Process Improvement

Digging deeper into cost reduction – Efficiency Program 2.0

Optimization / Control

Strategic Sourcing

Organization/ Rightsizing

and Efficiency

Process Improvement

Business Model

Changes

> R$1 bln in savings

Jan/15 Dec/17

Business Model

Changes

• 3 years program

• Between R$ 300-350 mln per year

Mar/16

Corporate Efficiency Plan

Additional Efficiency & Cost Restructuring

• Enhancement of corporate efficiency program;

• Additional efforts in Sales & Marketing (commissioning

model and advertising);

• Full cash cost approach;

+ Sales & MKT

New Approach

Optimization / Control

+

Strategic Sourcing

+

Organization/ Rightsizing

and Efficiency

+

~ 40%

11 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

1.34

1.12 1.16

-8% -1% +63%

+41 mln

1Q15 ∆ Other OPEX

ProductsMargin

1Q16 Reported TransformationCosts / Expenses

1Q16 Normalized

1Q15 1Q16

317

128

1Q15 1Q16

Defending margin despite tough environment

Net Debt Net Profit

MTR Cut - Last year of material impact EBITDA Evolution (R$ bln; % YoY)

EBITDA Margin

29.1% 29.5%

Normalized1 EBITDA (R$ bln; % YoY)

Normalized¹ EBITDA Exposure

-9.1% ex-MTR

-60%

7.9

3.5

4.4

Debt Cash Net Debt

(R$ bln)

Net Debt / 12M EBITDA: 0.54x

MTR Impact

1.34 1.16

1.22

1 Normalization is related to transformation costs/expenses in HR and G&A

(R$ mln)

Voice & Data Contribution Margin

Impact of off-net offers, investment

for repositioning & future growth

-13.5%

30.2%

-16.6%

-13.5%

1 ~14% ~8%

12 Results Presentation

Investor Relations

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Conclusion & Outlook

Less impact from

MTR

-8.7% -9.2%

4Q15 1Q16 2Q16 3Q16 4Q16

-5.3%

-13.5%

4Q15 1Q16 2Q16 3Q16 4Q16

Mobile Service Net Revenues (%YoY)

Normalized¹ EBITDA (%YoY)

1 Normalization is related to transformation costs/expenses in HR and G&A

Headwinds should gradually reduce…

Traditional business

stabilization

Data services

resuming growth

Better customer

base mix

Continuous cost

efficiency program

intensified

Keeping focus on

Infrastructure