kuehn amended complaint

TRANSCRIPT

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 1/69

1

IN THE UNITED STATES DISTRICT COURTFOR THE SOUTHERN DISTRICT OF MISSISSIPPI

SOUTHERN DIVISION

HENRY KUEHNAND JUNE P. KUEHN PLAINTIFFS

VERSUS CIVIL ACTION NO. 1:08CV577-LTS-RHW

STATE FARM FIRE AND CASUALTY COMPANYAND JOHN DOES 1 THROUGH 10 DEFENDANTS

AMENDED COMPLAINT

JURY TRIAL DEMANDED

COME NOW the Plaintiffs, HENRY KUEHN AND JUNE P. KUEHN, by and through

their attorneys of record, DENHAM LAW FIRM, and would file their Amended Complaint

against Defendants, State Farm Fire and Casualty Company (“State Farm Fire”) and John Does

1-10 (“John Does”), and allege as follows:

I.

PARTIES

1. Plaintiffs, HENRY KUEHN and JUNE P. KUEHN, are adult resident citizens of

the State of Mississippi, residing at 3208 North 3rd Street, Ocean Springs, Jackson County,

Mississippi.

2. Defendant, State Farm Fire, is a corporation organized and existing under the laws

of the State of Illinois, with its principal office and place of business located at One State Farm

Plaza, Bloomington, Illinois 71701-0001. This defendant may be served with process by service

on its agent for service of process, William Penna, at 1080 River Oakes Drive, Suite B-100,

Flowood, Mississippi 39232-7644, or on the Mississippi Insurance Commissioner at Post Office

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 2/69

2

Box 79, Jackson, Mississippi, 39205-0079, pursuant to Mississippi Code Annotated Section 83-

21-1.

3. At the time of the loss there was a line of credit with Keesler Federal Credit

Union secured by the Plaintiffs’ home, but it has since been paid off so that the home is free and

clear of liens that might require notice of this action.

4. Defendants John Does 1-10 are entities affiliated with Defendant and/or have

acted in concert with Defendant, and whose identities are currently unknown. All allegations

and claims asserted herein against the Defendant are incorporated herein by reference against

John Does 1-10. Said John Does, when their identities are known, will be identified by name

and joined in this action, if necessary, pursuant to the Federal Rules of Civil Procedure.

II.

SUBJECT MATTER AND PERSONAL JURISDICTION

5. This Court has jurisdiction over the subject matter and the Defendant in this case

pursuant to 28 U.S.C. § 1332 because there is complete diversity of citizenship between

Plaintiffs and Defendants and the amount in controversy exceeds $75,000.00.

III.

VENUE

6. Venue in this case is proper in this Court pursuant to 28 U.S.C. § 1391, because

this suit concerns real property located exclusively in Jackson County, Mississippi, and the

conduct, acts and/or omissions upon which this cause of action is based occurred in Jackson

County, Mississippi, which is completely within the United States District Court for the Southern

District of Mississippi, Southern Division.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 3/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 4/69

4

policy would provide full and comprehensive coverage for damage to the insured building

caused by windstorm.

12. On August 29, 2005, within the subject policy period, most of the insured

residence and the personal contents therein were proximately and/or efficiently damaged or

destroyed by the winds, rain, and wind-propelled objects of Hurricane Katrina. It is undisputed

that the storm surge reached the subject property; however, by the time the surge arrived, the

insured residence had already been rendered uninhabitable and the contents therein were

damaged or destroyed.

13.

Almost immediately thereafter, and in accordance with the subject policy

provisions, Plaintiffs notified State Farm Fire of the covered loss. An adjuster by the last name

of Wildsmith visited their property to make a determination.

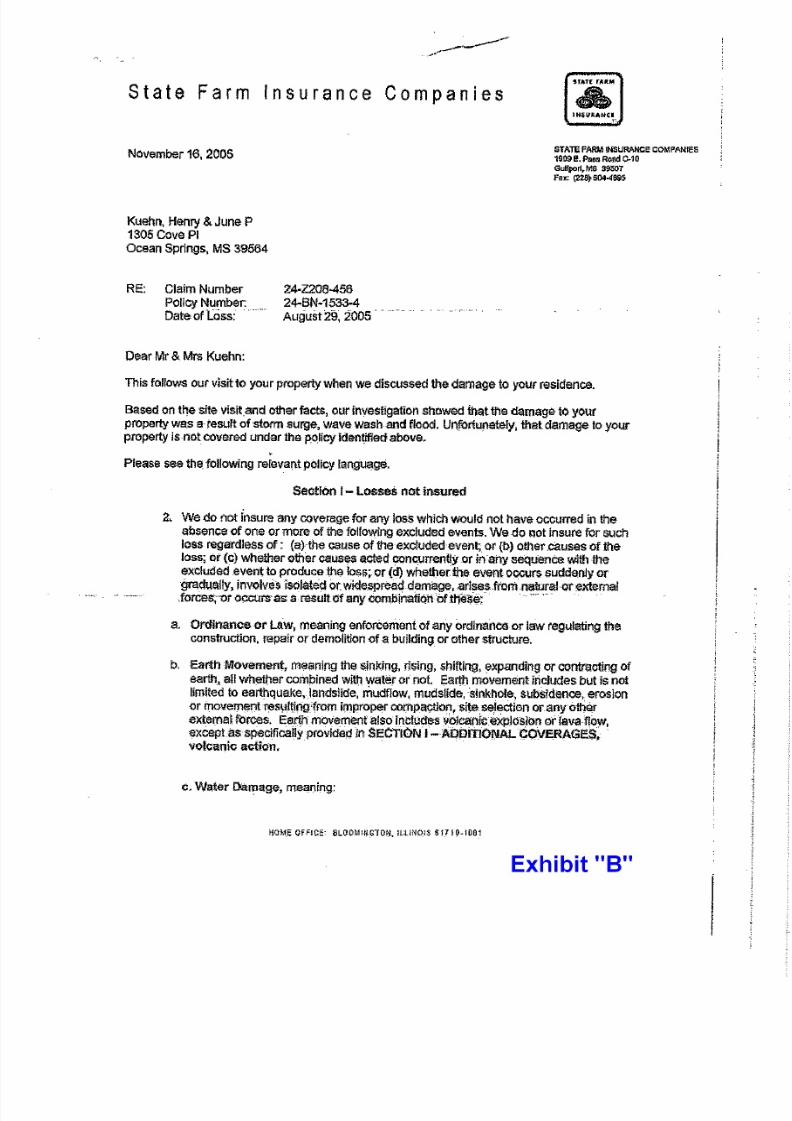

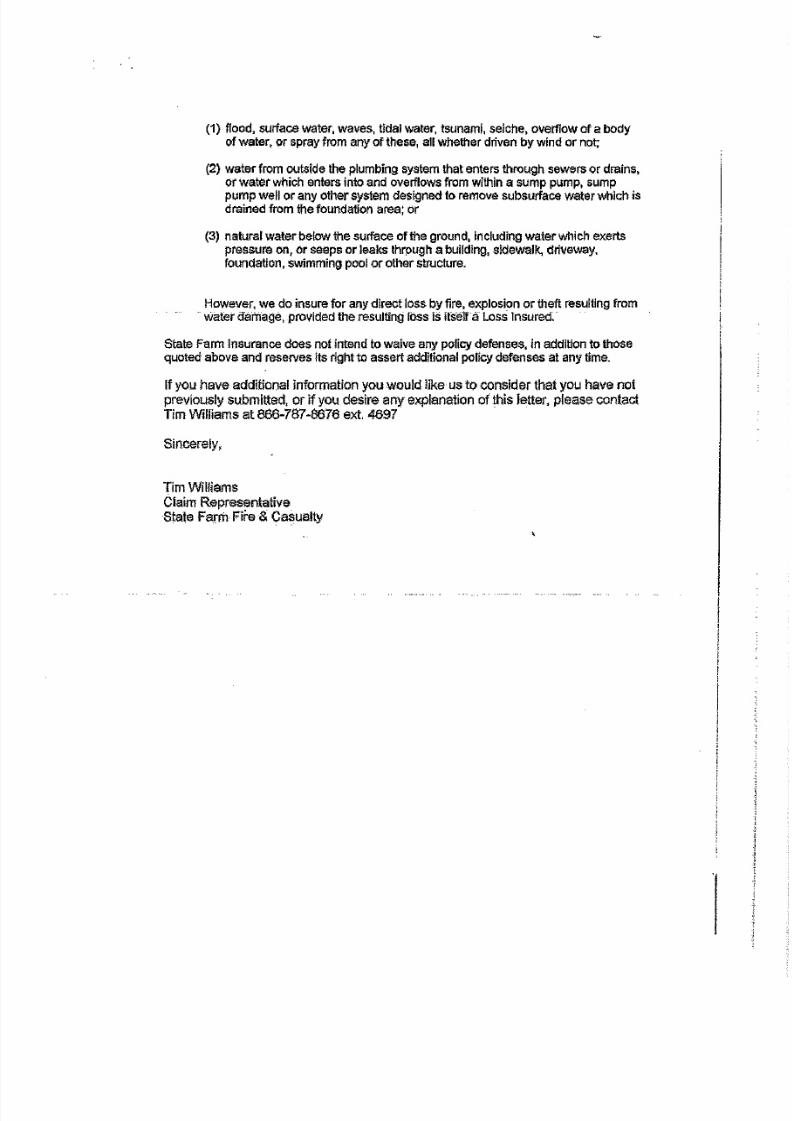

14. On or about November 16, 2005, State Farm Fire wrote to the Plaintiffs and

advised, contrary to the subject policy coverage provisions and despite the fact that the insured

property was damaged by wind, rain and/or wind-propelled objects, that the “damage to your

property was a result of storm surge, wave wash and flood. Unfortunately, that damage to your

property is not covered under the policy.” See attached Exhibit “B,” Letter from State Farm

Fire dated November 16, 2005.

15. Subsequently in a letter to Plaintiffs dated January 4, 2006, State Farm Fire,

contrary to the subject policy coverage provisions and despite the fact that the insured property

was damaged by wind, rain and/or wind-propelled objects, informed Plaintiffs that it would not

cover the loss beyond what was already paid, which was $10,765.48. See attached Exhibit “C,”

Letter from State Farm Fire dated January 4, 2006.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 5/69

5

16. Plaintiffs were completely unsatisfied with the inadequate payment, but they

continued their negotiations with State Farm Fire in an effort to settle their claim. The Kuehns

demanded appraisal under the terms of their policy, as was their right under the terms of the

contract. The policy states as follows:

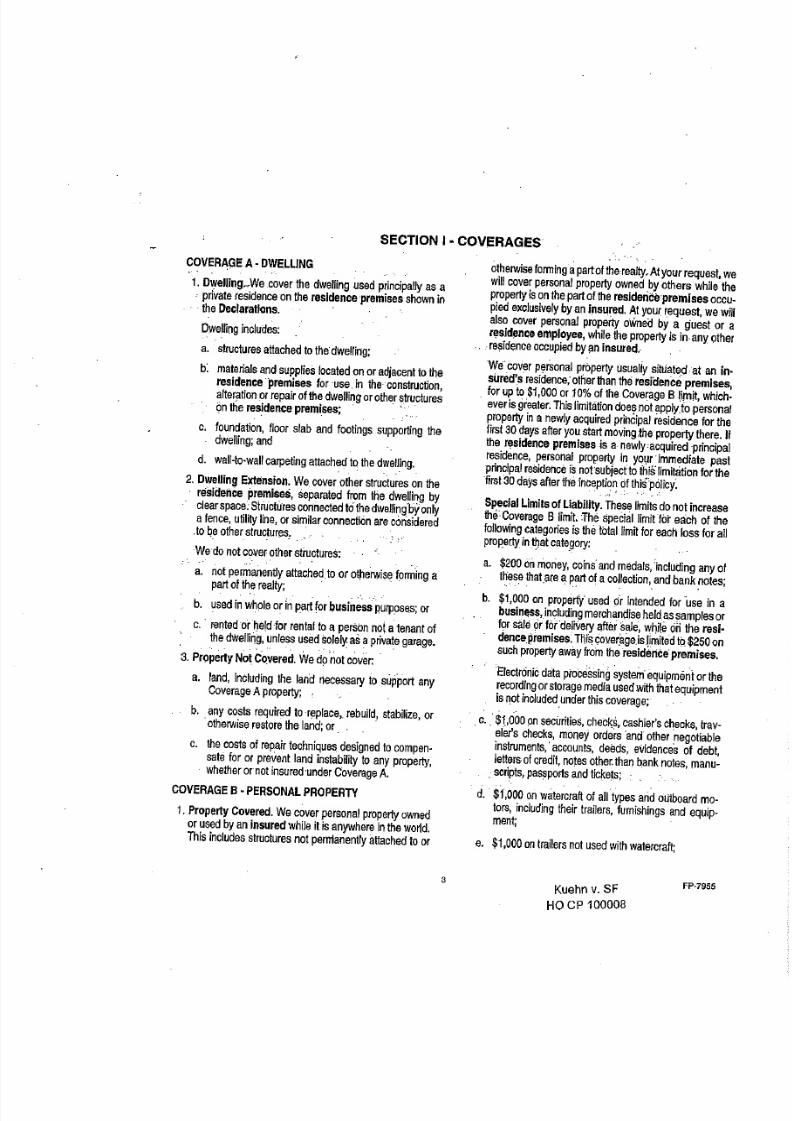

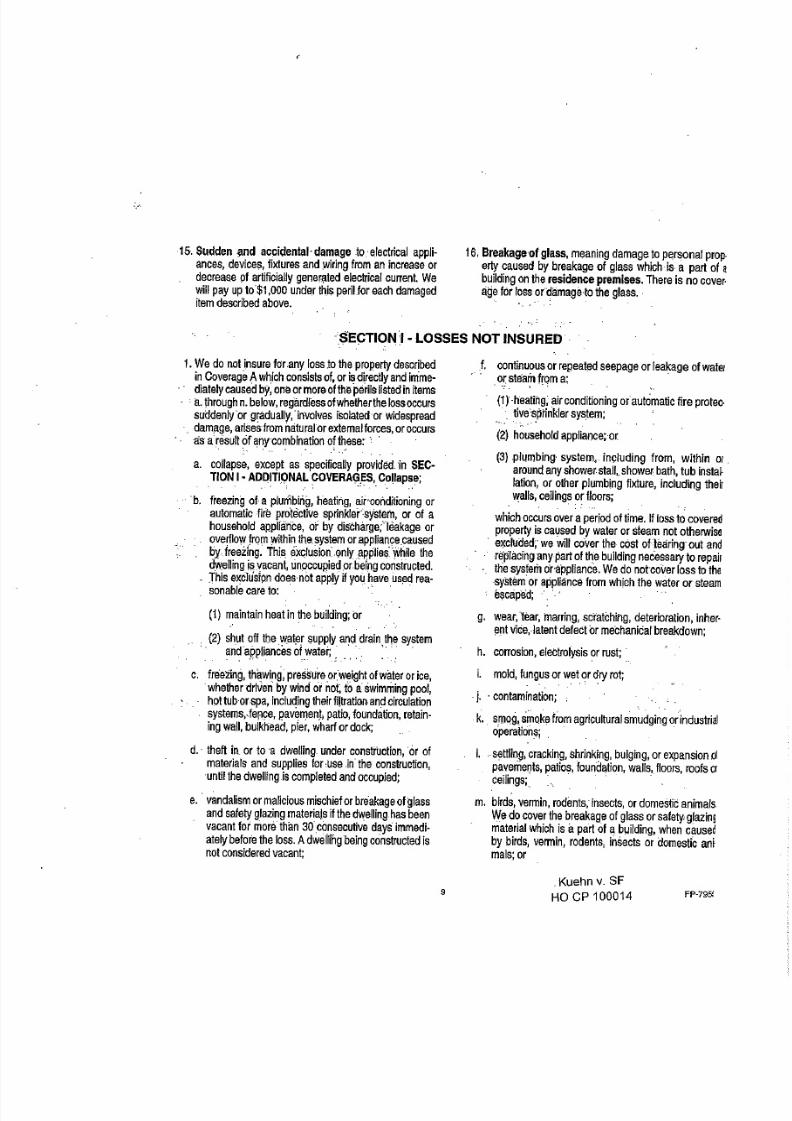

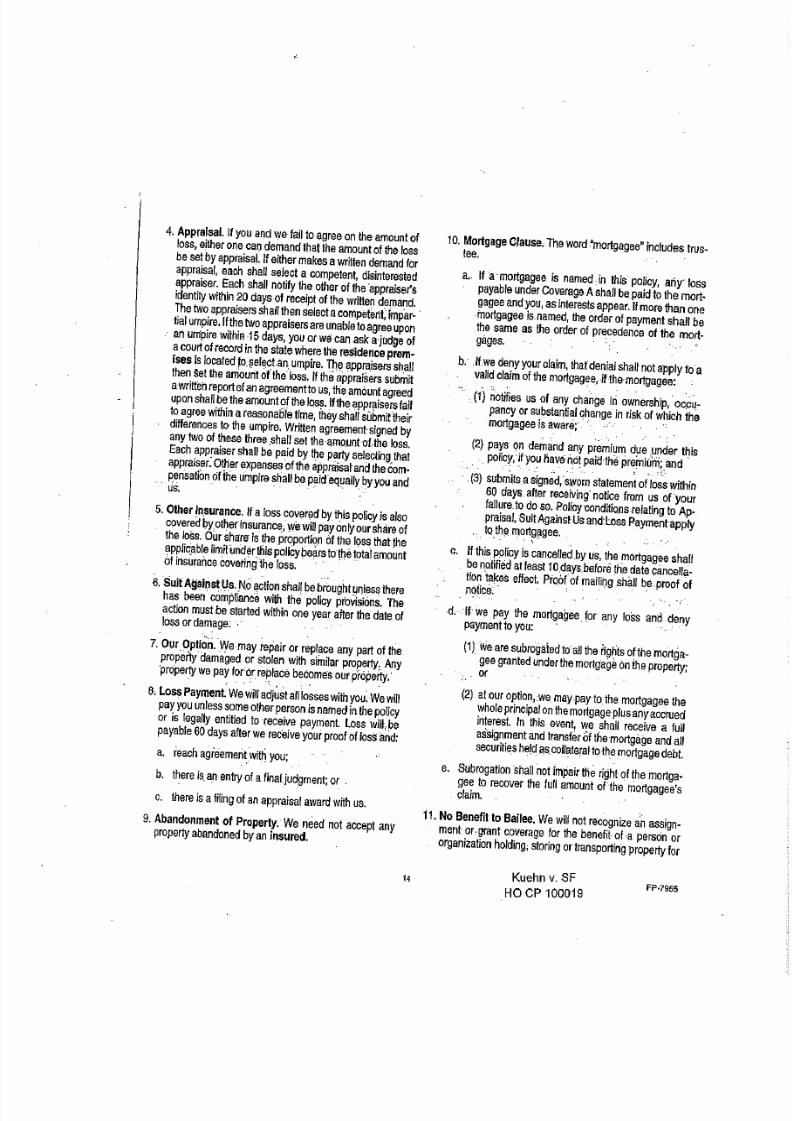

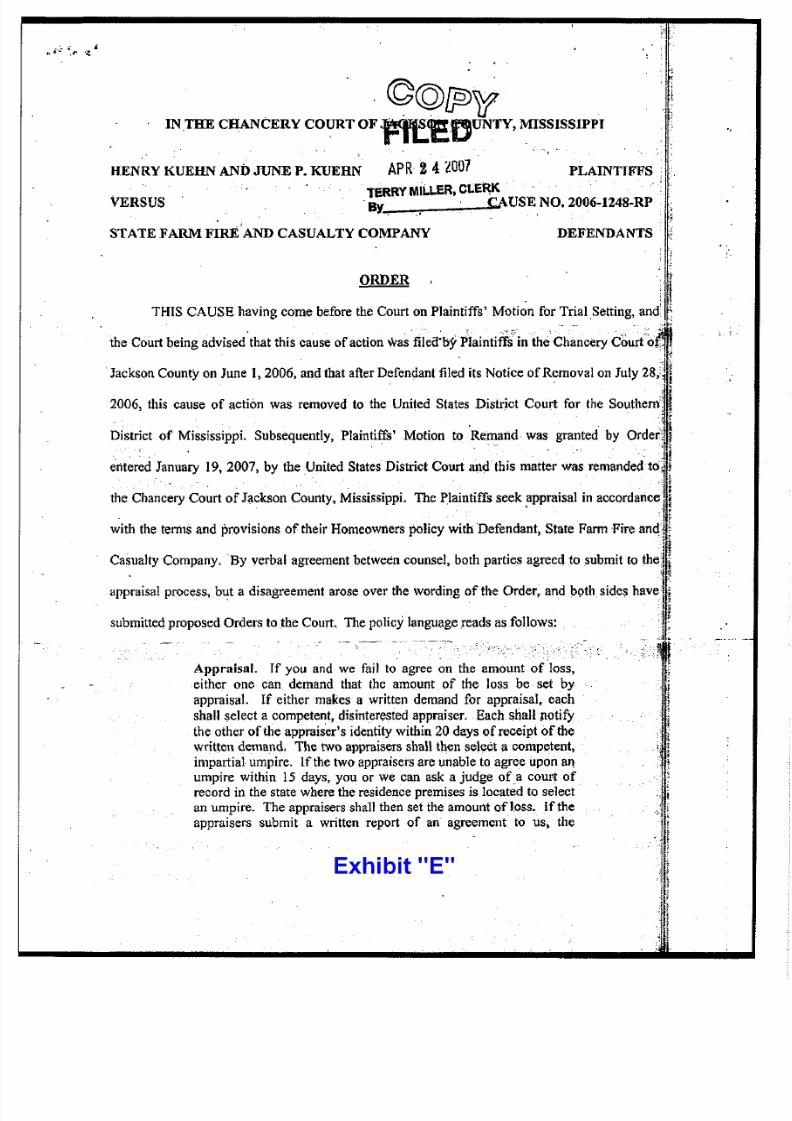

Appraisal. If you and we fail to agree on the amount of loss,either one can demand that the amount of the loss be set byappraisal. If either makes a written demand for appraisal, eachshall select a competent, disinterested appraiser. Each shall notifythe other of the appraiser’s identity within 20 days of receipt of thewritten demand. The two appraisers shall then select a competent,impartial umpire. If the two appraisers are unable to agree upon anumpire within 15 days, you or we can ask a judge of a court of

record in the state where the residence premises is located to selectan umpire. The appraisers shall then set the amount of loss. If theappraisers submit a written report of an agreement to us, theamount agreed upon shall be the amount of the loss. If theappraisers fail to agree within a reasonable amount of time, theyshall submit their differences to the umpire. Written agreement

signed by any two of these three people for any item shall set

the amount of loss. Each appraiser shall be paid by the partyselecting that appraiser. Other expenses of the appraisal and thecompensation of the umpire shall by paid equally by you and us.(Emphasis added)

. . . .

Loss Payment. We will adjust all losses with you. We will payyou unless some other person is named in the policy or is legallyentitled to receive payment. Loss will be payable 60 days after .. . there is a filing of an appraisal award with us.

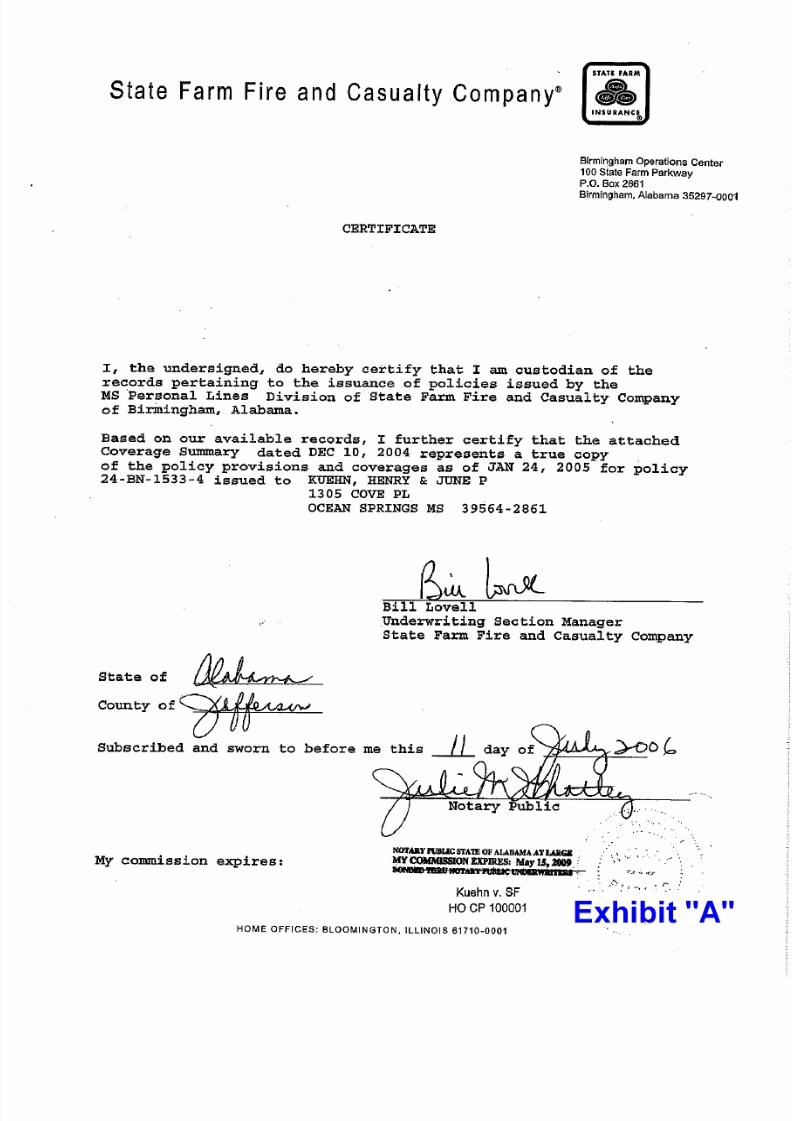

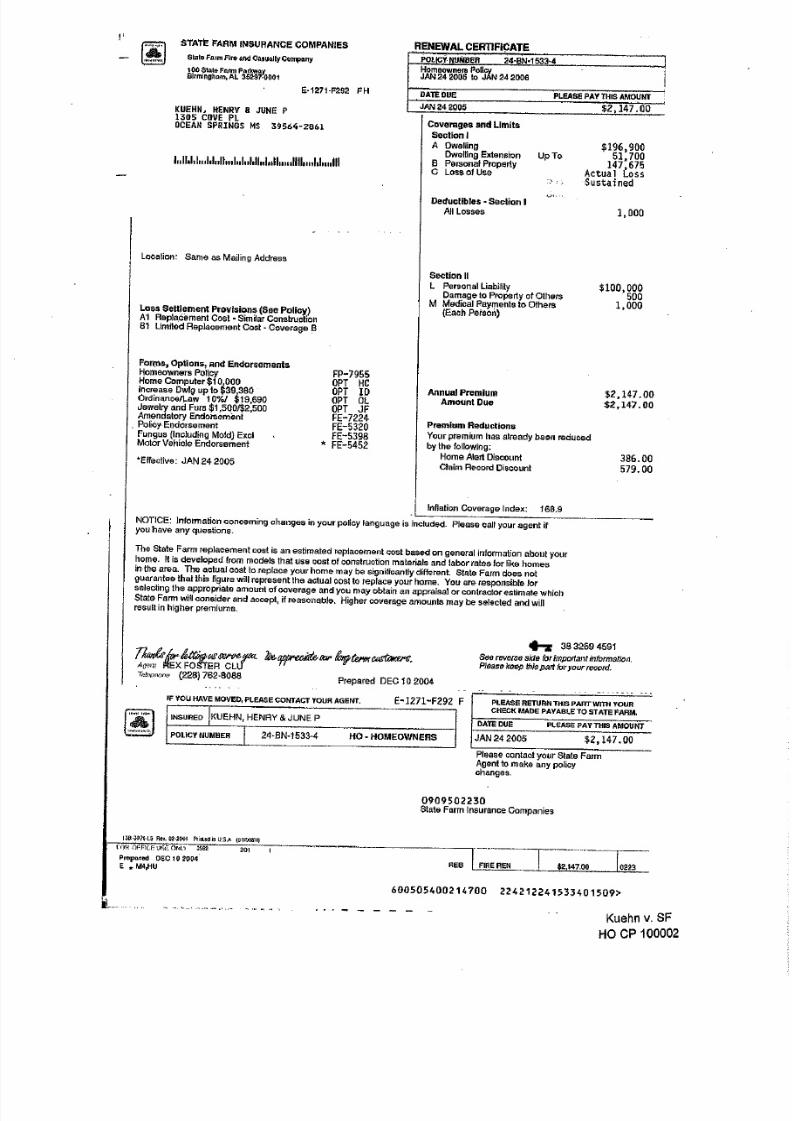

See Exhibit “A,” Certified policy. There was no response from State Farm Fire to Mr. Kuehn’s

request.

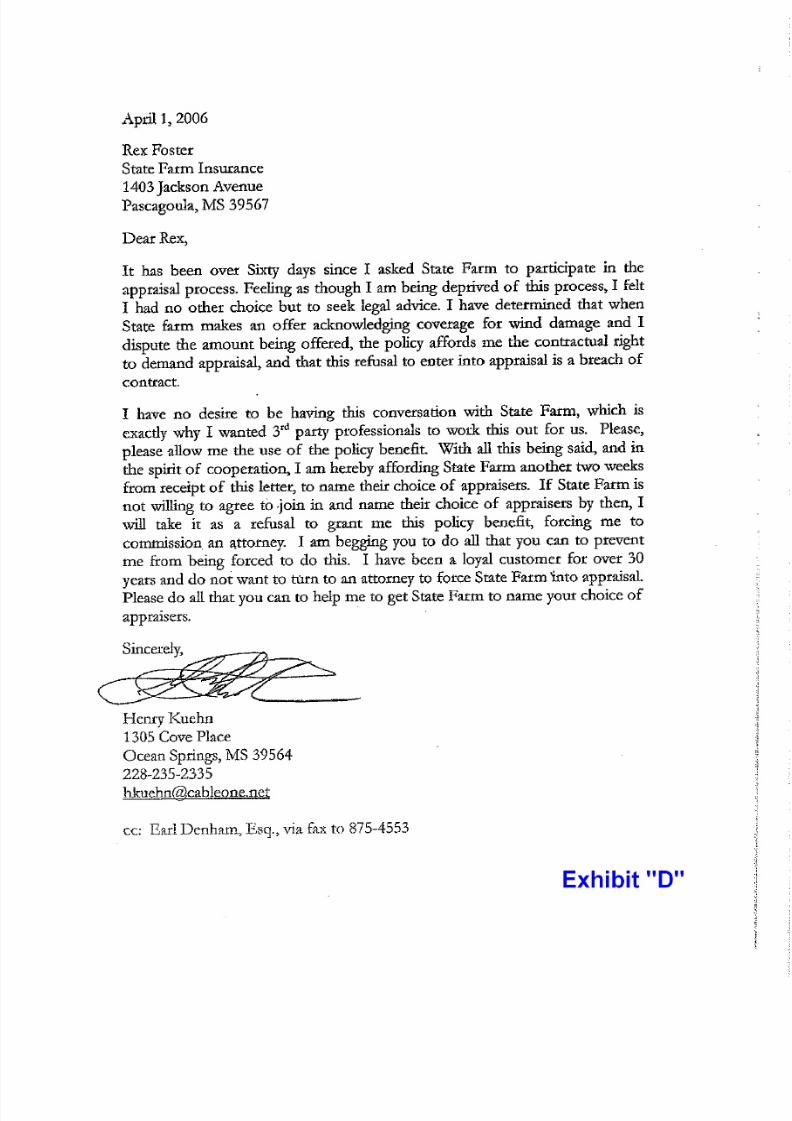

17. On April 1, 2006, Mr. Kuehn wrote to State Farm Fire to follow up on his prior

requests to participate in the appraisal process. See attached Exhibit “D,” Letter from Mr. Kuehn

to State Farm insurance agent Rex Foster, dated April 1, 2006.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 6/69

6

18. On April 17, 2006, Mr. Kuehn had a telephone conversation with a State Farm

representative named Tina, from Team 10. During this conversation, Tina informed Mr. Kuehn

that “The State of Mississippi has overrode [sic] our appraisal options.” Mr. Kuehn asked her

“You can’t get appraisal now, is that more or less what you’re saying,” to which she replied,

“Exactly.” She went on to say, “That’s what our management is saying, we’re not offering

appraisal at all because mediation overrides it.”

19. On June 21, 2006, Plaintiffs filed their Complaint in the Chancery Court of

Jackson County, Mississippi, asking for injunctive relief by the Chancellor; i.e., to compel State

Farm Fire to comply with the terms of its contract and go through with the appraisal process. On

July 28, 2006, State Farm Fire filed the Notice of Removal to the United State District Court and

also filed its Answer to the Complaint contesting the requested appraisal.

20. Plaintiffs filed their Motion to Remand on August 17, 2006. On August 24, 2006,

the U. S. Magistrate Judge entered an Order Staying Case pending a ruling on Plaintiffs’ Motion

to Remand.

21. One year after Hurricane Katrina on August 29, 2006, State Farm Fire filed its

Motion to Conduct Remand Related Discovery and for Additional Time to Respond to Plaintiffs'

Motion to Remand, which the Federal Court granted, allowing limited discovery on the appraisal

issue.

22. After the parties conducted discovery on the appraisal issue, United States District

Judge Senter entered an Order of Remand on January 19, 2007, granting Plaintiffs' Motion to

Remand and remanded the case to the Chancery Court of Jackson County, Mississippi.

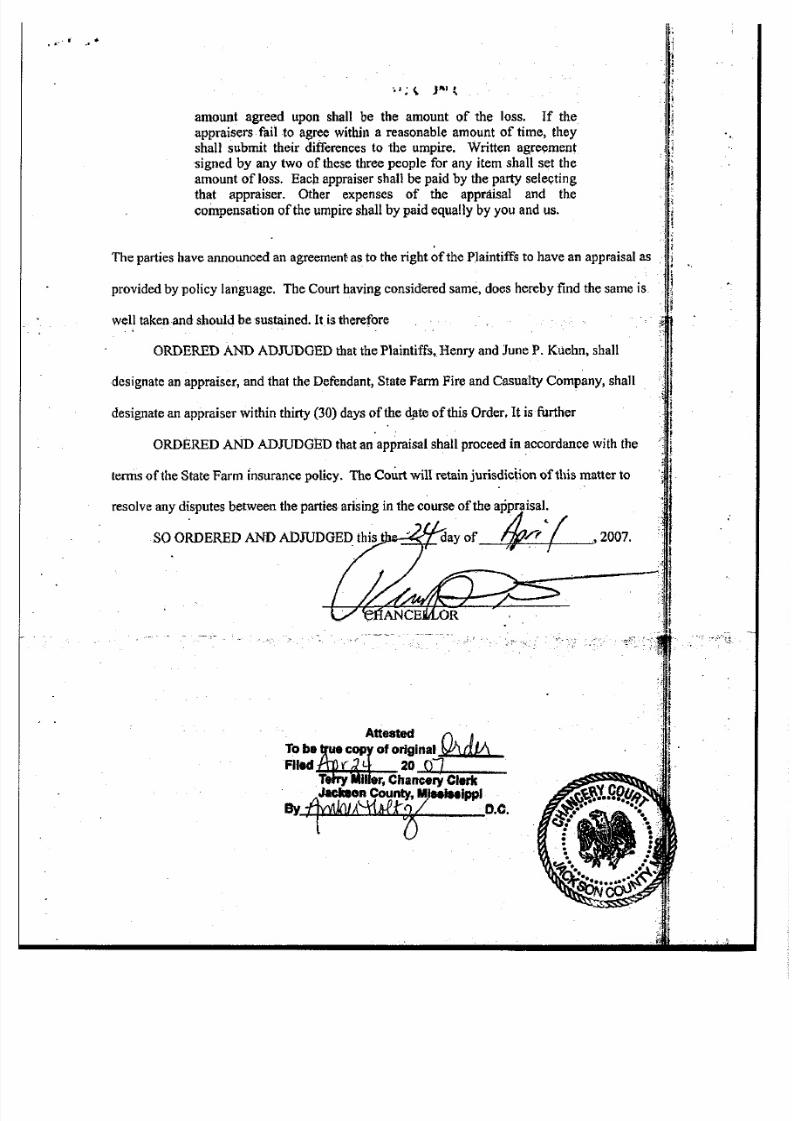

23. After the remand, the Chancery Court of Jackson County entered an Order on

April 24, 2007, finding the request for appraisal to be appropriate, and ordered each party to

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 7/69

7

designate an appraiser within 30 days. See Exhibit “E,” Order of Chancery Court of Jackson

County filed August 24, 2007. Plaintiffs filed their Designation of Appraiser on May 29, 2007,

and State Farm Fire filed its Designation of Appraiser on or about June 14, 2007. The parties

actually went through with the appraisal process under the State Farm policy, and the appraisers

appointed by both parties determined the value of the loss.

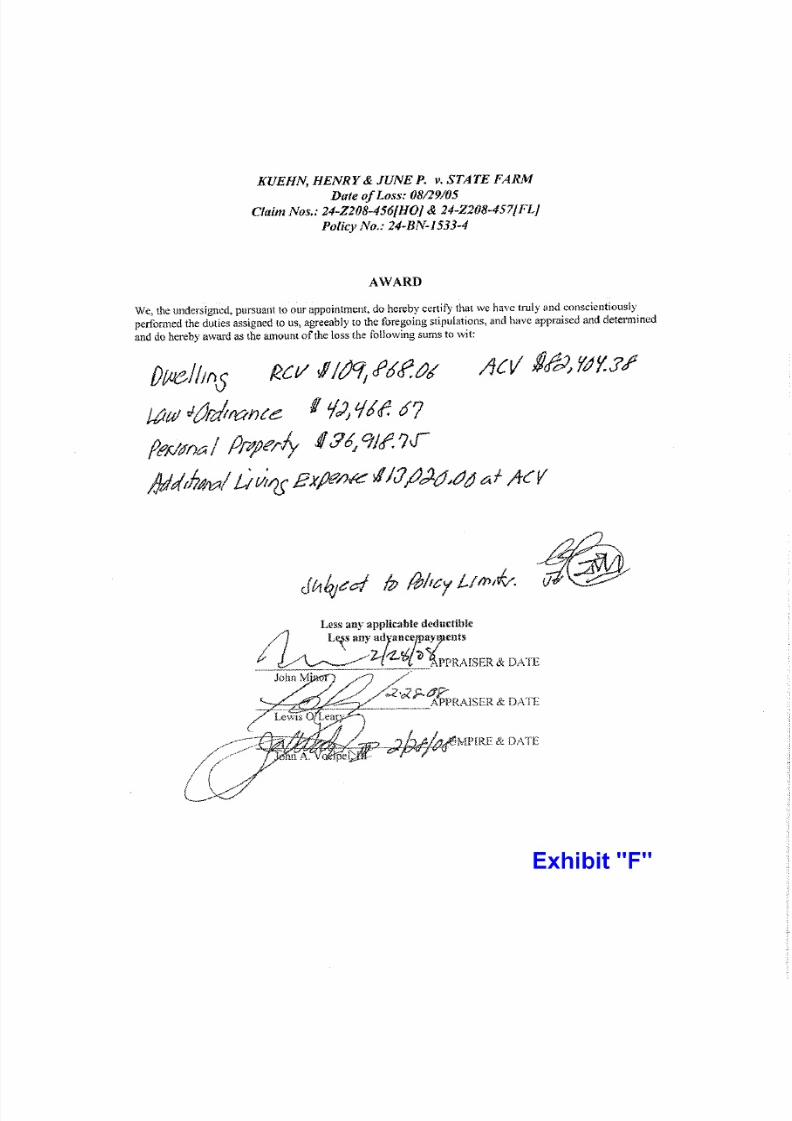

24. On February 28, 2008, the appraisal process concluded, and the umpire and the

parties’ appraisers signed an Award setting forth the appraisal amount of $174,811.80. A copy of

the Award is attached hereto and incorporated herein as Exhibit “F”. Yet after the Award was

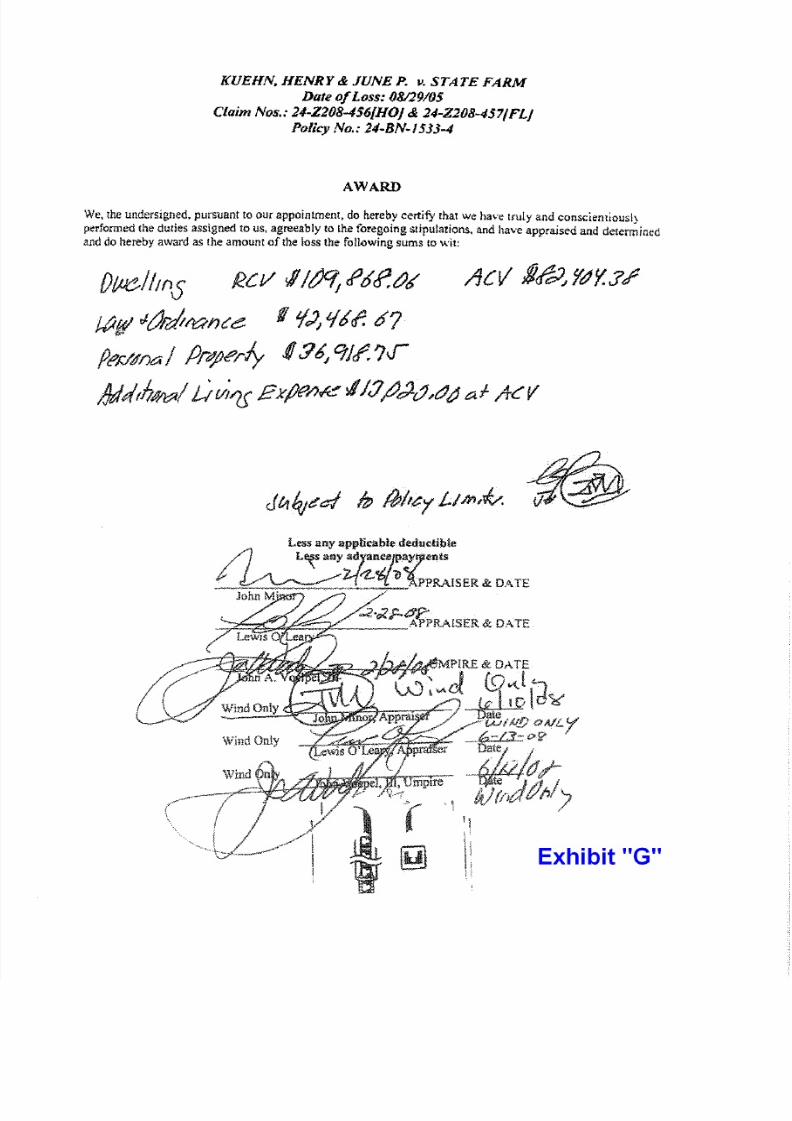

produced, counsel for State Farm Fire told the appraisers and the umpire that the Award did not

specify which part was for wind. However, the appraisers and umpire confirmed that entire

amount was for wind damage, i.e., that they had determined the amount of “loss” as they were

supposed to do under the policy. A copy of the amended Award is attached hereto and

incorporated herein as Exhibit “G”. As of the date of filing the Complaint, State Farm Fire has

contemptuously failed and refused to pay Plaintiffs any portion of the appraisal Award, contrary

to the clear terms of its own insurance contract and breaching its duty to the Plaintiffs. It has

done so maliciously, with gross negligence, and in recklessly indifferent regard to Plaintiffs’

rights.

25. Three years after the hurricane and despite their best efforts to settle their claim

with State Farm Fire, Plaintiffs still have not been fully compensated for their losses and State

Farm Fire still has not complied with the terms of the policy it drafted and sold to Plaintiffs. The

only other payment State Farm Fire has made was for $4,771.55, which was made on August 20,

2008.

26. State Farm Fire’s position in this directly contradicts Mississippi insurance law, in

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 8/69

8

existence for the last forty years, which mandates full insurance coverage if the hurricane winds

were the efficient proximate cause of the loss. It is uncontroverted that loss caused by hurricane

and/or tornadic wind is covered under the subject policy. It is also uncontroverted that Plaintiffs

had a right to appraisal under the subject policy.

27. Additionally, as the policy at issue is an “all risk” policy, all risks of accidental

direct physical loss are covered by the subject policy unless specifically excluded by the terms of

the subject policy. In such policies, insureds such as the Plaintiffs only have the burden of

showing the existence of a covered loss, at which point the burden of proof shifts to the insurer,

State Farm Fire, to establish the applicability of a named exclusion under the facts of the case

and the terms of the policy.

28. In this case, there is no question that the Plaintiffs have established a loss covered

by the subject policy. State Farm Fire has the burden to prove that the loss was attributable to an

excluded peril such as “flood,” and not to a covered peril, such as wind. State Farm Fire has not

met this burden of proof and cannot meet it . There is no question that an appraisal award was

entered. There is no question that State Farm Fire did not make a loss payment to Plaintiffs

within 60 days of the entry of the appraisal award.

29. An insurance contract is a contract of adhesion, and should be construed in the

light most favorable to the insured.

30. Inherent in any insurance contract, and in the policy at issue, is that payment must

be made promptly so that the insured may be put back into the position he or she was in prior to

the loss, and as quickly as possible.

31. A special relationship exists between an insurer and its insured; such relationship

is best characterized as one of the utmost good faith and fair dealing.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 9/69

9

32. Plaintiffs have complied with all conditions precedent to obtaining payment of

benefits under the subject policy, and State Farm Fire has waived and/or is estopped from raising

such conditions precedent.

33. State Farm Fire is merely attempting to dodge its coverage obligations to the

Plaintiffs under the subject policy by wrongfully characterizing their damage as being from

flood, surface water, waves and/or tidal water.

34. State Farm Fire’s investigation, adjustment, and denial of Plaintiffs’ claim were

negligent, grossly negligent, and in reckless disregard for Plaintiffs’ rights. State Farm Fire’s

denial of and eventual underpayment of Plaintiffs’ loss breached the subject contract of

insurance. Such conduct constitutes bad faith and tortious breach of contract and breach of duty

of good faith and fair dealing. State Farm Fire unjustly, in bad faith, denied Plaintiffs the

appraisal demanded under the subject policy. State Farm Fire fraudulently and/or negligently,

with gross negligence, reckless disregard for Plaintiffs’ rights and actual malice, misrepresented

to Plaintiffs through its policy of insurance that they could utilize the appraisal process provided

by the policy. Plaintiffs relied on these representations to their detriment. State Farm Fire’s

conduct has forced its customers to resort to litigation in order to receive benefits that should

have been paid under the policy, and to compel State Farm Fire and Casualty Company to

comply with its own policy terms.

35. Plaintiffs are therefore entitled to full coverage under the subject policy for the

damage to their property, injunctive relief, specific performance of the contract, indemnity,

unjust enrichment, other such equitable relief, and extra-contractual, compensatory and punitive

damages.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 10/69

10

V.

COUNT ONE:

DECLARATORY JUDGMENT

AND INJUNCTION AS TO APPRAISAL

36. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

37. This count is an action for declaratory judgment pursuant to Federal Rule of Civil

Procedure 57, and an action for an Injunction pursuant to Federal Rule of Civil Procedure 65.

38. The Defendant introduced and inserted a procedure into their policy, appraisal,

which was intended to afford policy holders and the insurance company a reasonable and

affordable alternative to litigation. From their actions, it is evident that the Defendant never

intended to use this procedure and instead wrote said procedure into its policies merely to entice

policy holders to pay premiums for coverage and dispute resolution that in reality it would not

offer, and where implementation would be resisted at any cost by the Defendant to the point that

appraisal could never resolve anything.

39. Because of the Defendant’s actions in misrepresenting and in dodging the

appraisal process, the Plaintiffs were forced to litigate the very issue of the existence of

appraisal, which within itself was supposedly designed to limit and/or remove the necessity and

expense of litigation. As a result of the Defendant’s behavior, the Plaintiffs had to seek and hire

counsel to assert their right to the appraisal “offered” by the Defendant, incurring attorney’s fees

in an amount exceeding $10,000.00. The Plaintiffs did hire counsel who filed suit in Chancery

Court to assert their right to appraisal, and the Defendant improperly removed said suit to

Federal Court. The removal was entirely done to further deny the Plaintiffs their right to

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 11/69

11

appraisal and was done with the intent to damage the Plaintiffs and cost them further attorney’s

fees. The Federal Court realized this improper removal and issued an Order of Remand.

40. After remand, the Chancery Court of Jackson County entered an Order on April

24, 2007, granting Plaintiffs’ request for an appraisal and ordered each party to designate an

appraiser within 30 days. Plaintiffs filed their Designation of Appraiser on May 29, 2007, and

State Farm Fire filed its Designation of Appraiser on or about June 14, 2007.

41. On February 28, 2008, the appraisal process concluded, and the umpire and the

parties’ appraisers signed an Award setting forth the appraisal amount of $174,811.80. Copies of

the Award and the amended Award are attached hereto and incorporated herein as Exhibits “F”

and “G”. However, as of the date of filing the Complaint, State Farm Fire has failed and refused

to pay Plaintiffs any portion of the appraisal Award.

42. The Plaintiffs’ policy provides:

Appraisal. If you and we fail to agree on the amount of loss,either one can demand that the amount of the loss be set byappraisal. If either makes a written demand for appraisal, eachshall select a competent, disinterested appraiser. Each shall notifythe other of the appraiser’s identity within 20 days of receipt of thewritten demand. The two appraisers shall then select a competent,impartial umpire. If the two appraisers are unable to agree upon anumpire within 15 days, you or we can ask a judge of a court of record in the state where the residence premises is located to selectan umpire. The appraisers shall then set the amount of loss. If theappraisers submit a written report of an agreement to us, theamount agreed upon shall be the amount of the loss. If theappraisers fail to agree within a reasonable amount of time, theyshall submit their differences to the umpire. Written agreement

signed by any two of these three people for any item shall set the

amount of loss. Each appraiser shall be paid by the party selectingthat appraiser. Other expenses of the appraisal and thecompensation of the umpire shall by paid equally by you and us.(Emphasis added)

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 12/69

12

43. State Farm Fire’s policy further states that “Loss will be payable 60 days after we

receive your proof of loss and . . . there is a filing of an appraisal award with us.” (Emphasis

added). The requirement for the filing of a proof of loss was waived in the wake of Hurricane

Katrina. An appraisal award was, however, ultimately filed. State Farm Fire did not pay the

loss/award amount of $174,811.80 within sixty days of the appraisal award as its own policy

demanded.

44. Plaintiffs would hereby request that the Court enter a declaratory judgment to

state that appraisal was done, to enforce the appraisal Award as a binding amount to be paid, and

to cause State Farm Fire to pay unto Plaintiffs the sum of $174,811.80 as per the appraisal

Award, as well as to order the Defendant to reimburse the Plaintiffs for their costs in the

appraisal process, due to State Farm Fire’s unreasonable delay tactics.

45. Plaintiffs would hereby request that an injunction issue to direct Defendant, State

Farm Fire, to pay unto Plaintiffs the sum of $174,811.80 as per the appraisal Award.

46. The Plaintiffs ask that the Court award declaratory relief and/or that the Court

award injunctive relief in ordering State Farm Fire and Casualty Company to pay what was

awarded in the appraisal process, and that the Court order the Defendant to pay punitive and/or

exemplary damages for their malicious behavior, attorney’s fees, extra-contractual damages

including damages for pain and suffering, costs of the appraisal and any other damages found

proper by this Court.

VI.

COUNT TWO:

DECLARATORY JUDGMENT AS TO THE POLICY

47. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 13/69

13

48. This count is an action for declaratory judgment pursuant to Federal Rule of Civil

Procedure 57.

49. On the occasion of Hurricane Katrina, Plaintiffs’ insured property was

proximately and/or efficiently devastated by wind, rain and wind-propelled objects. However,

State Farm Fire has maintained and continues to maintain the position that the majority of the

Plaintiffs’ claim was caused by water or water-borne material, relying on the exclusions in the

subject policy.

50. As a result of State Farm Fire’s partial payment of Plaintiffs’ claim, it has

admitted that wind damage to Plaintiffs’ property occurred, which is a covered peril. See Exhibit

“C”, Letter from State Farm Fire, dated January 4, 2006, with summary of loss.

51. In order to deny coverage for the Plaintiffs’ loss resulting from Hurricane

Katrina, State Farm Fire has the burden to prove that the loss was attributable to an excluded

peril, such as “flood,” rather than a covered peril, such as wind.

52. State Farm Fire has not met and cannot meet its burden of proof. The damage to

Plaintiffs’ property is thus covered under the subject policy. State Farm Fire should have

tendered policy limits to Plaintiffs as soon as it became apparent that it could not meet said

burden of proof.

53. Wherefore, Plaintiffs respectfully seek a declaration from this Court that:

(a) State Farm Fire breached its policy obligations to its insureds and

owes coverage for the damage sustained to Plaintiffs’ insured property due to

Hurricane Katrina;

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 14/69

14

(b) In order to deny coverage for Plaintiffs’ claim under the subject

policy, State Farm Fire has the burden to prove that the loss was attributable to an

excluded peril and not to a covered peril;

(c) State Farm Fire has not met and cannot meet its burden of proof, and

the loss and damage is thus covered under the subject policy; and

(d) Plaintiffs are entitled to an award of damages for the full value of all

coverage available to them under the policy, and such other extra-contractual

damages or relief as this Court may deem fit to make them whole; Plaintiffs are

entitled to receive a trial by jury on all issues triable.

VII.

COUNT THREE:

NEGLIGENCE/GROSS NEGLIGENCE/

RECKLESS DISREGARD FOR THE RIGHTS OF PLAINTIFFS

54. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

55. State Farm Fire had a duty under Mississippi law to fully, promptly, fairly,

adequately and correctly investigate and adjust Plaintiffs’ claim for damages caused by

Hurricane Katrina.

56. State Farm Fire breached its duty to conduct such an investigation, and to base its

decision on the facts. State Farm Fire knew or should have known that it could not meet its

burden of proving its policy exclusions, but it denied the claim based upon said exclusion

anyway.

57. State Farm Fire negligently and grossly negligently, in reckless disregard of

Plaintiffs’ rights, underpaid the claim, refused to comply with the appraisal process set forth in

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 15/69

15

the policy, and then failed and refused to pay monies to Plaintiffs in accordance with the policy

or the appraisal Award. State Farm Fire has repeatedly demonstrated its reckless disregard for

Plaintiffs’ rights. State Farm Fire has unreasonably delayed the claims process and it has refused

to fully and adequately compensate Plaintiffs and delayed making even the inadequate payment

that it eventually did.

58. State Farm Fire breached its duty by failing to adequately investigate and adjust

Plaintiffs’ claim. State Farm Fire breached its duty by denying Plaintiffs’ claim without meeting

its affirmative duty of proving at the time of the denial that Plaintiffs’ loss was proximately and

efficiently caused by “flood/tidal surge”, a peril excluded by the policy.

59. State Farm Fire breached its duty by denying Plaintiffs’ claim without meeting its

affirmative duty of establishing at the time of the denial, which amount of Plaintiffs’ loss was

caused by water and which amount was caused by wind.

60. Similarly, State Farm Fire breached its duty by failing to pay and/or by

subsequently underpaying Plaintiffs for the damage State Farm Fire could not prove was caused

by “flood/tidal surge”.

61. State Farm Fire breached its duty by shifting to the Plaintiffs the burden of

proving that the loss was not excluded by the policy.

62. State Farm Fire breached its duty by dispatching an adjuster that did not have the

qualifications or training to investigate, adjust and then deny Plaintiffs’ losses.

63. State Farm Fire breached its duty by failing to properly train its adjuster as to how

to investigate and adjust Plaintiffs’ losses.

64. State Farm Fire breached its duty by basing its denial of Plaintiffs’ claims for

hurricane damage on the investigation and adjustment of an unqualified adjuster.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 16/69

16

65. State Farm Fire breached its duty by failing to adequately inspect, investigate or

adjust the insured property prior to denying the claim, and by its subsequent underpayment of the

claim.

66. State Farm Fire breached its duty by failing to credit the statements from

eyewitnesses in investigating and adjusting Plaintiffs’ claim.

67. State Farm Fire breached its duty by failing to utilize an objective meteorologist

or structural engineer to determine the cause of Plaintiffs’ loss prior to denying the claim.

68. State Farm Fire breached its duty by failing to pay Plaintiffs for their losses.

69.

State Farm Fire intentionally interpreted its exclusions in the broadest possible

manner as a means of underpaying and/or denying valid claims such as the Plaintiffs’. The law

does not support State Farm Fire’s interpretation of said exclusions, but State Farm Fire

nevertheless attempted to use said broad interpretations to deny claims and thus increase its

profits.

70. Such conduct as alleged above constitutes negligence, gross negligence, and/or

reckless disregard for Plaintiffs’ rights as State Farm Fire insureds.

71. State Farm Fire’s negligent, grossly negligent, and/or reckless adjustment

proximately caused Plaintiffs to suffer economic and other damages.

VIII.

COUNT FOUR:

SPECIFIC PERFORMANCE OF INSURANCE CONTRACT

72. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

73. State Farm Fire entered into the subject contract of insurance with the Plaintiffs

wherein it clearly and expressly agreed to provide insurance coverage for physical loss to

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 17/69

17

property and loss of use proximately and efficiently caused by windstorm or hail. Plaintiffs, in

turn, have paid State Farm Fire substantial premiums.

74. Plaintiffs suffered substantial damage and/or destruction of their insured building

and property as a proximate and direct result of covered losses, and have consequently been

denied use of their property.

75. Plaintiffs have performed their end of the bargain and are accordingly now

entitled to Specific Performance of the subject insurance contract. The Court should therefore

require State Farm Fire to specifically perform such agreement.

IX.

COUNT FIVE:

WAIVER AND ESTOPPEL

76. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

77. State Farm Fire had the obligation to establish, prior to denying the claim, what

part, if any, of the loss fell under the terms of its exclusion. By declaring its burden of proof

irrelevant and intentionally abandoning its obligation to establish what, if any, part of the loss

was excluded, Defendant waived its right to attempt to put on “after-the-fact” evidence to

exclude any part of the claim.

78. State Farm Fire intentionally interpreted its exclusions in the broadest possible

manner as a means of underpaying and/or denying valid claims such as the Plaintiffs’. The law

does not support State Farm Fire’s interpretation of said exclusions, but State Farm Fire

nevertheless attempted to use said broad interpretations to deny claims and thus increase its

profits.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 18/69

18

79. State Farm Fire induced the Plaintiffs to rely on its representations that it was

handling the claim in good faith, while at the time, it had actually already adopted claims

handling procedures through which coverage under the subject policy would be denied in

Plaintiffs’ situation. Defendant should be estopped from denying that it owes full coverage

under the Homeowner’s policy to the Plaintiffs and all similarly situated insureds of the

Defendant.

80. State Farm Fire, by failing to conduct a prompt, reasonable and thorough

investigation prior to denying and/or underpaying the subject claim, has waived its right to

conduct a new investigation to justify its denial, and hence should be estopped from utilizing

information that it did not have at the time it denied or underpaid the subject claim as its

“arguable basis” for said denial.

X.

COUNT SIX:

INDEMNITY

81. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

82. State Farm Fire is obligated under the subject policy and by its representations to

provide full insurance coverage to Plaintiffs for all damage to the insured building and property

caused by windstorm or hail.

83. However, State Farm Fire has denied Plaintiffs their insurance coverage and has

refused to pay them for their covered losses.

84. As a direct and proximate result of State Farm Fire’s denial and subsequent

underpayment, Plaintiffs have been and/or will be forced to pay significant amounts of money to

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 19/69

19

rebuild and/or replace their severely damaged or destroyed property, and to pursue litigation in

order to recover amounts properly due under the subject policy.

85. The expenses Plaintiffs have incurred and continue to incur as a result of State

Farm Fire’s refusal to completely pay what they are owed are expenses that State Farm Fire, in

all fairness and equity, should pay under the subject policy or otherwise. Plaintiffs are therefore

entitled to indemnity from State Farm Fire and Casualty Company for all sums they have

expended and will be required to expend, as well as debt they will be required to incur, in order

to repair, refurbish, and/or replace the insured building and property, as well as any sums

expended or debts incurred as a result of being forced to hire engineers, attorneys and other

experts in order to recover sums under their insurance contract.

XI.

COUNT SEVEN:

UNJUST ENRICHMENT/CONSTRUCTIVE TRUST

86. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

87. In marketing, selling and issuing the subject policy to Plaintiffs, State Farm Fire

represented and agreed to obtain and provide Plaintiffs with full coverage for property damage

and loss of use, as well as for damage proximately caused by windstorm or hail as a result of

hurricane winds and rain. These representations and contractual obligations are also evidenced

by the subject policy’s coverage provisions.

88. Plaintiffs have paid State Farm Fire substantial monetary premiums for such

coverage.

89. Despite realizing substantial premiums from Plaintiffs, State Farm Fire has

withheld the insurance proceeds owed to Plaintiffs for the damage to their insured property.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 20/69

20

90. By purposefully mischaracterizing the damage to Plaintiffs’ building and property

as being caused by “flood/tidal surge” despite a complete lack of evidence or diligent

investigation, and despite the fact that State Farm Fire knew or should have known it could not

prove that Plaintiffs’ property was damaged solely by excluded perils, State Farm Fire has

wrongfully realized insurance premiums and withheld insurance proceeds to which the Plaintiffs

are entitled, and have gained interest on such sums.

91. State Farm Fire has therefore been unjustly enriched at Plaintiffs’ expense.

92. Plaintiffs have suffered injury as a proximate result of State Farm Fire’s unjust

enrichment. Plaintiffs have been and will continue to be forced to pay for costs that should, in

equity and good conscience, be borne by State Farm Fire under the subject policy.

93. As a proximate result of State Farm Fire’s false representations and refusal to

provide full insurance coverage under the subject policy for the damage to Plaintiffs’ insured

home and property, State Farm Fire is in possession of premiums, insurance proceeds and other

monies that it should not, in equity and good conscience, be entitled to retain.

94. Plaintiffs are therefore entitled to damages resulting from State Farm Fire’s unjust

enrichment, including, but not limited to, the imposition of a Constructive Trust on all premiums

Plaintiffs paid to State Farm Fire and on the insurance proceeds wrongfully held by State Farm

Fire under the subject policy.

XII.

COUNT EIGHT:

BAD FAITH

95. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 21/69

21

96. State Farm Fire had a duty to undertake a prompt and reasonable investigation

into the Plaintiffs’ claim and to base its decision on the evidence.

97. State Farm Fire knew or should have known that it was incumbent upon it, in

denying Plaintiffs’ claim, to meet the factual burden of proving the damage to Plaintiffs’

property was due solely to an excluded peril such as “flood/tidal surge”, but nevertheless it failed

to do so and initially denied Plaintiffs’ claim.

98. In bad faith, State Farm Fire refused to comply with the appraisal clause in its

policy and the accompanying settlement of loss language. State Farm Fire intentionally denied

Plaintiffs this right, in reckless disregard of their clear rights under the policy, and forced

Plaintiffs to file suit in Chancery Court to get State Farm Fire to comply with its own policy.

Once the ordered appraisal was concluded and an award was rendered, State Farm Fire refused to

comply with its own policy and compensate the Plaintiffs.

99. After intentionally interpreting its exclusions in the broadest possible manner,

State Farm Fire denied valid claims such as that of the Plaintiffs. State Farm Fire’s interpretation

of its exclusions is not supported by the law, but it relied upon those expansive interpretations to

deny claims and thus increase its profits.

100. Because of State Farm Fire’s conduct in handling and denying Plaintiffs’ claim,

Plaintiffs have suffered depression, emotional distress, mental anxiety, and mental anguish.

State Farm Fire knew that Plaintiffs’ home was severely damaged/destroyed and no longer

habitable, but nevertheless unreasonably denied Plaintiffs’ claim. Further, State Farm Fire

exercised unreasonable delay in its paltry investigation of said claim, further causing mental

anguish to Plaintiffs. Such depression, emotional distress, mental anxiety, and mental anguish

were clearly foreseeable results to State Farm Fire when it unreasonably denied Plaintiffs’ claim.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 22/69

22

XIII.

COUNT NINE:

FRAUDULENT CLAIMS PRACTICES

101.

Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

102. The massive number of properties destroyed by Hurricane Katrina left State Farm

Fire facing the prospect of large payouts to its insureds after Hurricane Katrina. Upon

information and belief, State Farm Fire made an initial assessment of the magnitude of the

losses, and then it conceived and instituted a fraudulent course of claims practices to be applied

to Katrina cases such as Plaintiffs’ claim.

103. The claim of Plaintiffs and other insureds of State Farm Fire whose homes and

businesses were destroyed or substantially damaged by Hurricane Katrina were wrongfully

denied pursuant to Defendant’s Katrina-specific corporate “top-down” scheme of fraudulent and

deceptive claims practices.

104. State Farm Fire in effect rewrote its contract and its claims procedures for cases

where properties were destroyed or substantially damaged by wind and water and embarked on

an intentional course of pre-litigation and post-litigation conduct, fraudulently concealed from

the Plaintiffs and other insureds, deliberately designed to deny legitimate claims covered under

the Defendant’s contract, the insurance policy, and Mississippi law.

105. State Farm Fire’s intentional broad interpretation of the exclusions in its policy

were undertaken as a means of denying and/or underpaying valid claims of State Farm Fire’s

insureds. Although State Farm Fire’s interpretation of its exclusions is not supported by the law,

it continued to use them as a means to deny or reduce its obligations to its insureds in order to

protect its profits.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 23/69

23

106. State Farm Fire also sold Plaintiffs a policy containing an appraisal clause and

other policy language, representing to Plaintiffs that said clause was available to Plaintiffs, and

representing that State Farm Fire would comply with the terms of its policy. It did so

fraudulently, as Plaintiffs found out when they were denied appraisal in the wake of Hurricane

Katrina. Plaintiffs relied on this to their detriment, and were ultimately forced to file suit to get

State Farm Fire to comply with the terms of its own policy. Plaintiffs were damaged thereby,

including incurring attorneys’ fees, extra-contractual damages, mental anguish, mental anxiety,

emotional distress, and other damages clearly foreseeable to State Farm Fire as a result of its

conduct.

107. The actions of State Farm Fire constituted a deliberate course of company-wide

fraudulent post-Katrina claims handling practices by which it intentionally undertook to defraud

the Plaintiffs and others whose properties were insured by State Farm Fire.

108. The scheme included post-Katrina modification of its coverage provisions, as well

as improper engineering procedures, all of which were concealed from Plaintiffs and others who

were expecting and relying on good faith handling of their claims by the Defendant.

109. State Farm Fire’s actions constitute fraud, fraudulent concealment and fraudulent

inducement, as well as bad faith claims handling on an institutional basis in State Farm Fire’s

handling of claims resulting from Hurricane Katrina. State Farm Fire’s actions were intended to,

and did, result in the intentional and fraudulent denial and/or underpayment of claims of the

Plaintiffs and others.

110. State Farm Fire’s actions warrant the imposition of compensatory, extra-

contractual and punitive damages under Mississippi law.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 24/69

24

XIV.

REMEDIES

111. Plaintiffs hereby incorporate and adopt by reference each and every allegation set

forth in each Paragraph of the Amended Complaint.

112. Plaintiffs are entitled to declaratory relief as to the rights and obligations of the

parties under the subject policy.

113. Plaintiffs are entitled to declaratory and injunctive relief as to the payment by

State Farm Fire of $174,811.80, as was awarded in the appraisal process provided by the policy.

114.

Plaintiffs are entitled to full insurance coverage under the subject policy for

damage to the insured building and property, as well as other monies they should have been paid

under the subject policy, and other such equitable relief set forth in the Complaint, including, but

not limited to, specific performance, indemnity and/or a constructive trust.

115. Plaintiffs are entitled to recover consequential and incidental damages caused by

State Farm Fire’s refusal to honor its obligations under the subject policy and otherwise.

116. Plaintiffs are entitled to recover punitive and/or exemplary damages for State

Farm Fire’s bad faith denial of coverage.

117. Plaintiffs are entitled to recover damages for pain and suffering, emotional

distress, mental anguish, loss of enjoyment of life and such other extra-contractual damages as

may be appropriate.

118. Plaintiffs are entitled to recover attorneys’ fees, litigation expenses, funds

expended on experts, pre-judgment interest and post-judgment interest; such expenses were

clearly foreseeable to State Farm Fire and Casualty Company as a result of its conduct.

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 25/69

25

WHEREFORE, PREMISES CONSIDERED, your Plaintiffs demand judgment against

the Defendants, and in particular Defendant, State Farm Fire and Casualty Company, of actual

damages in the amount of the appraisal Award, or in the alternative, in the amount of limits of

liability of their insurance policy, and other sums they should have been paid under the insurance

policy, extra-contractual damages and punitive damages in an amount sufficient to make

Plaintiffs whole and deter future wrongful conduct of the Defendants, and in particular

Defendant, State Farm Fire and Casualty Company, together with all costs, attorneys’ fees and

pre- and post-judgment interest. Plaintiffs request any further relief that may be appropriate.

Respectfully submitted,HENRY KUEHNAND JUNE P. KUEHN

BY: DENHAM LAW FIRM

BY: __s/Earl L. Denham___EARL L. DENHAMMS Bar No. 6047

CERTIFICATE

I, EARL L. DENHAM, do hereby certify that I electronically filed the above andforegoing Amended Complaint with the Clerk of the Court utilizing the ECF system, whichprovides notification of said filing to the following:

H. Scot [email protected] Hickman, Goza & Spragins, PLLC

Post Office Box 668Oxford, MS 38655-0068

John A. Banahan [email protected] H. Benjamin [email protected]; [email protected] Bryan, Nelson, Schroeder, Castigliola & Banahan

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 26/69

26

P.O. Drawer 1529Pascagoula, MS 39568-1529

SO CERTIFIED on this the 1st day of May, 2009.

___s/Earl L. Denham_EARL L. DENHAM

EARL L. DENHAM, MS Bar No. 6047KRISTOPHER W. CARTER, MS Bar No. 101963DENHAM LAW FIRM424 Washington Avenue (39564)Post Office Drawer 580Ocean Springs, MS 39566-0580

228.875.1234 Telephone228.875.4553 Facsimile

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 27/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 28/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 29/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 30/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 31/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 32/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 33/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 34/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 35/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 36/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 37/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 38/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 39/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 40/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 41/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 42/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 43/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 44/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 45/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 46/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 47/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 48/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 49/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 50/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 51/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 52/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 53/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 54/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 55/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 56/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 57/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 58/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 59/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 60/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 61/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 62/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 63/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 64/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 65/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 66/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 67/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 68/69

8/14/2019 Kuehn Amended Complaint

http://slidepdf.com/reader/full/kuehn-amended-complaint 69/69