h2020 energía limpia, segura y eficiente próximas oportunidades de participación

TRANSCRIPT

H2020: ENERGÍA LIMPIA, SEGURA Y EFICIENTE:

PRÓXIMAS OPORTUNIDADES DE

PARTICIPACIÓN

Pilar González GotorNCP Energía H2020

División de Programas de la UECDTI

Barcelona 21 de diciembre de 2016

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

3 (22/12/2016)

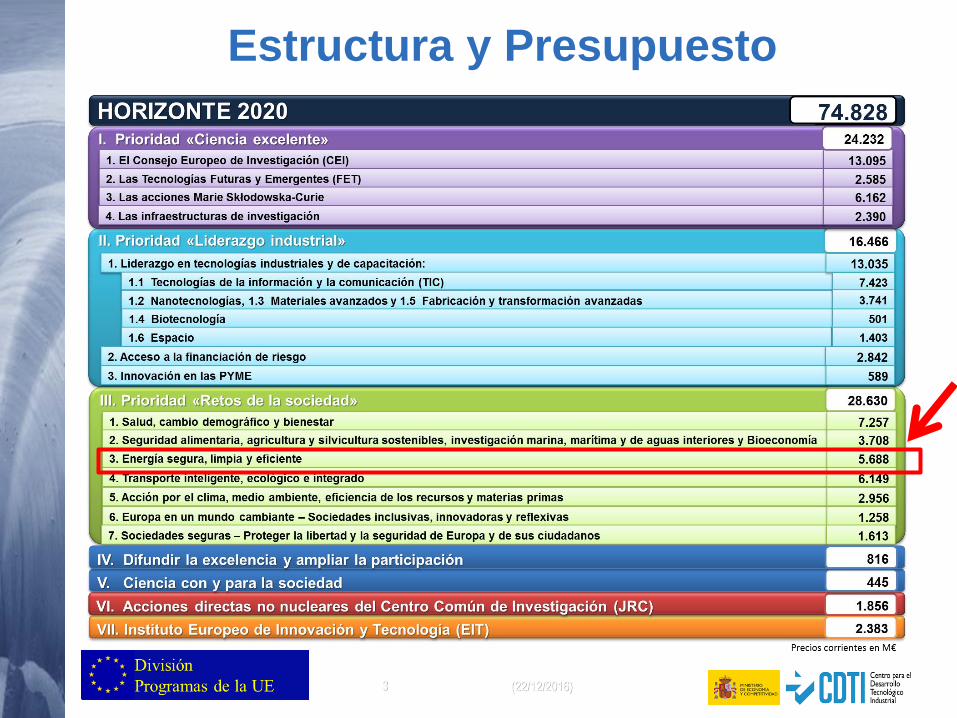

Estructura y Presupuesto

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

5 (22/12/2016)

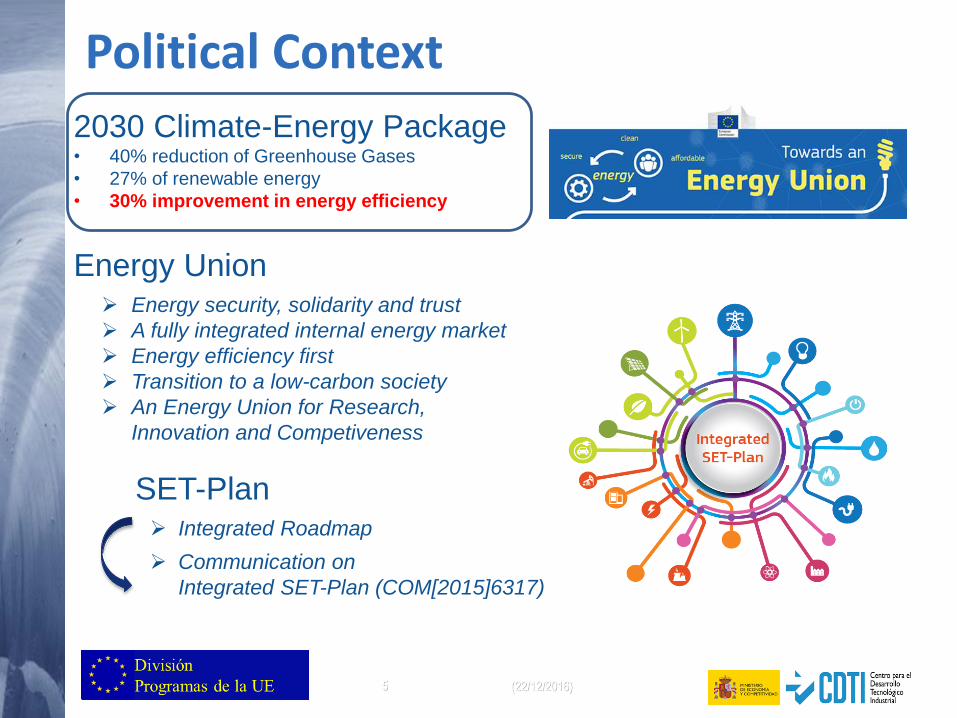

Political Context

2030 Climate-Energy Package• 40% reduction of Greenhouse Gases

• 27% of renewable energy

• 30% improvement in energy efficiency

Energy Union Energy security, solidarity and trust

A fully integrated internal energy market

Energy efficiency first

Transition to a low-carbon society

An Energy Union for Research,

Innovation and Competiveness

SET-Plan Integrated Roadmap

Communication on

Integrated SET-Plan (COM[2015]6317)

R&I as drivers for the 3 overarching goals of the Winter Package:

• Energy efficiency first

• Europe as a global leader in renewables

• A fair deal for consumers

CLEAN ENERGY FOR ALL EUROPEANS

6

Clean Energy R&Ias a part of the Energy Union Winter Package

7 (22/12/2016)

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

8 (22/12/2016)

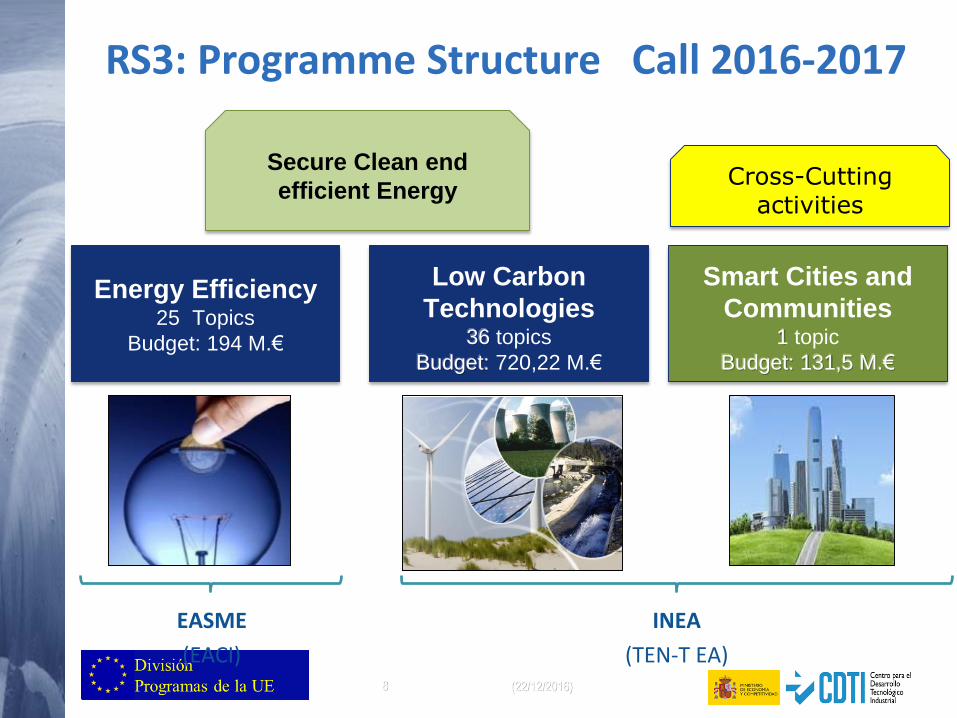

Secure Clean end

efficient Energy

Energy Efficiency25 Topics

Budget: 194 M.€

Low Carbon

Technologies36 topics

Budget: 720,22 M.€

Smart Cities and

Communities1 topic

Budget: 131,5 M.€

EASME

(EACI)

INEA

(TEN-T EA)

RS3: Programme Structure Call 2016-2017

Cross-Cutting activities

9 (22/12/2016)

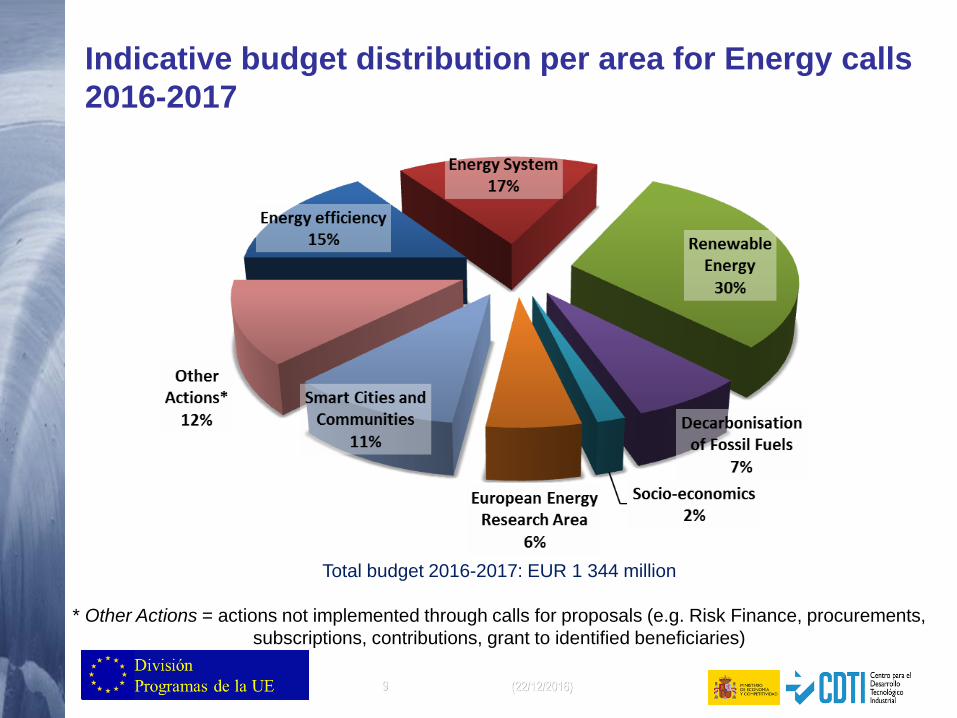

Indicative budget distribution per area for Energy calls

2016-2017

Total budget 2016-2017: EUR 1 344 million

* Other Actions = actions not implemented through calls for proposals (e.g. Risk Finance, procurements,

subscriptions, contributions, grant to identified beneficiaries)

10 (22/12/2016)

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

11 (22/12/2016)

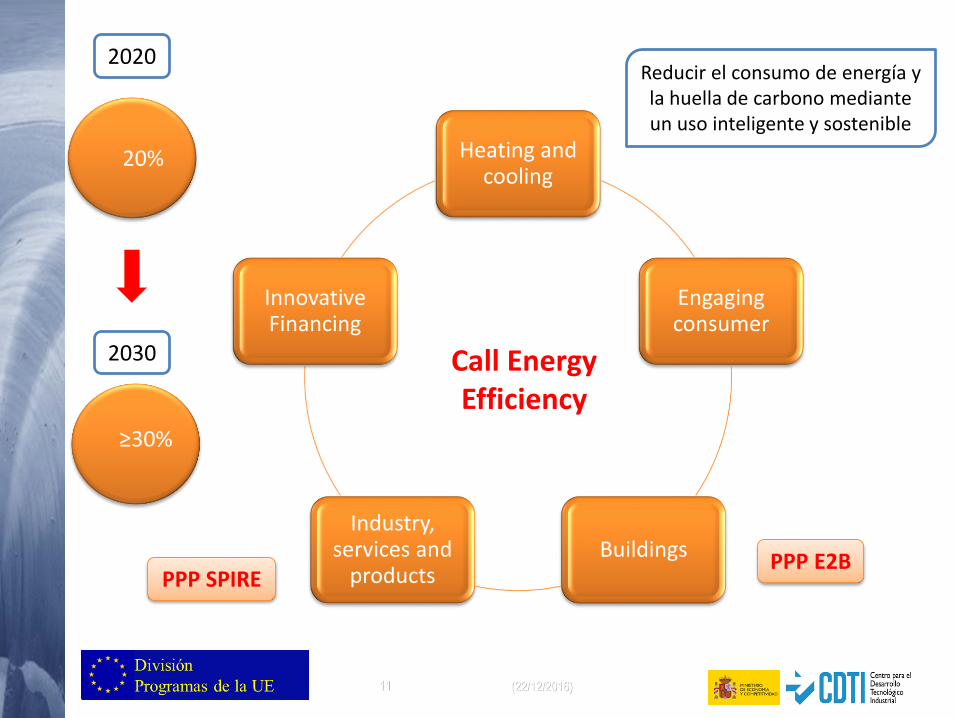

Heating and cooling

Engaging consumer

BuildingsIndustry,

services and products

Innovative Financing

Call Energy Efficiency

Reducir el consumo de energía y la huella de carbono mediante un uso inteligente y sostenible

20%

≥30%

2020

2030

PPP E2BPPP SPIRE

12 (22/12/2016)

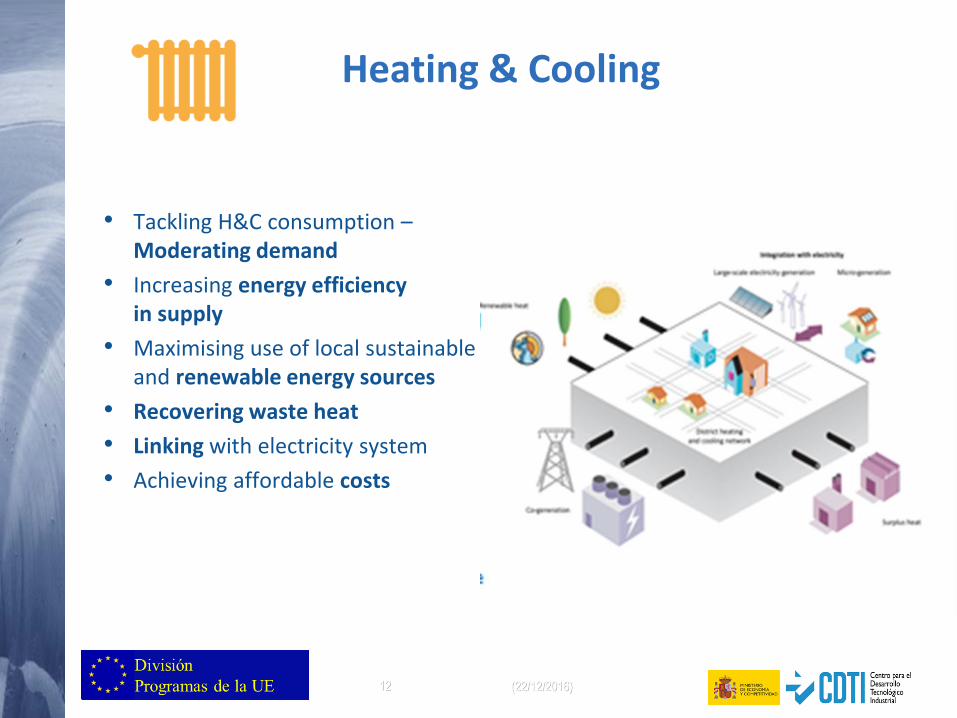

Heating & Cooling

• Tackling H&C consumption –Moderating demand

• Increasing energy efficiencyin supply

• Maximising use of local sustainable and renewable energy sources

• Recovering waste heat

• Linking with electricity system

• Achieving affordable costs

13 (22/12/2016)

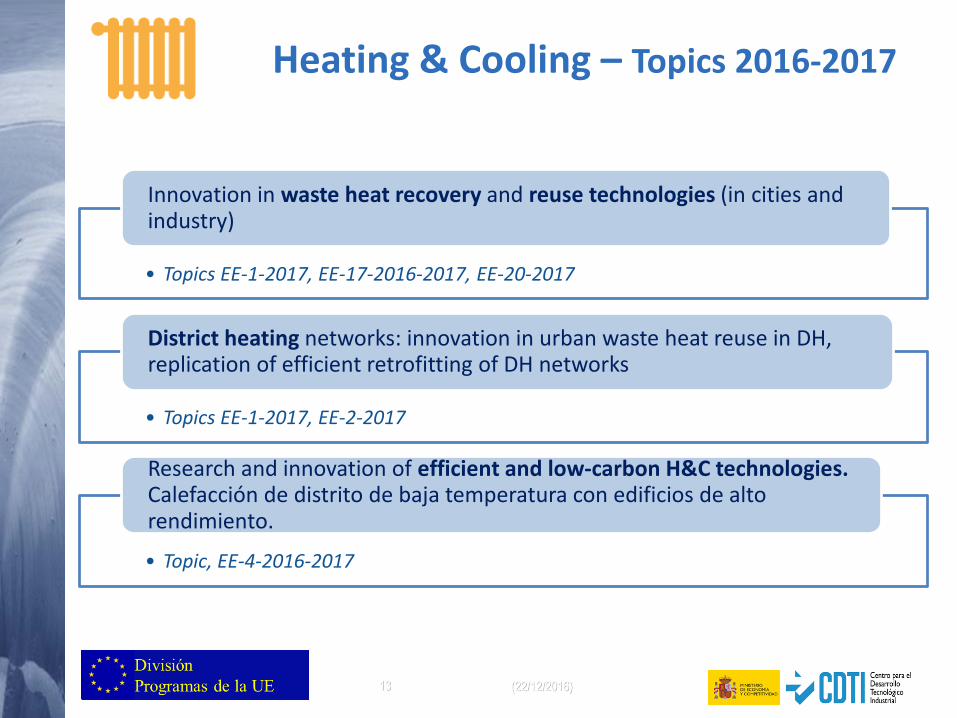

Heating & Cooling – Topics 2016-2017

• Topics EE-1-2017, EE-17-2016-2017, EE-20-2017

Innovation in waste heat recovery and reuse technologies (in cities and industry)

• Topics EE-1-2017, EE-2-2017

District heating networks: innovation in urban waste heat reuse in DH, replication of efficient retrofitting of DH networks

• Topic, EE-4-2016-2017

Research and innovation of efficient and low-carbon H&C technologies. Calefacción de distrito de baja temperatura con edificios de alto rendimiento.

14 (22/12/2016)

New deal for energy consumers: Empowering consumer Deploying demand side response Using smart technologies Protecting vulnerable customers

Objectives: Achieve a deeper understanding of consumer behaviour and motivation

structures Inform, engage and activate consumers

Consumer in the centre

15 (22/12/2016)

• Topic EE-6-2016-2017

Engaging private consumers towards sustainable energy

• Topic EE-7-2016-2017

Behavioural change toward energy-efficiency through ICT

• Topic EE-9-2016-2017

Engaging and activating public authorities

Consumer engagement –Topics 2016-2017

Consumer empowerment through smart homes system and demand response EE-12-2017

Consumer information through EU product efficiency legislation EE-16-2016-2017

16 (22/12/2016)

Buildings

Buildings account for 40% of the final energy consumption

• Increasing the rate, quality and effectiveness of renovation to reduce the energy use in buildings, as well as their replication capacity;

• Integration of demand response in energy management systems while ensuring interoperability;

• Reducing the cost of designing and constructing new Near-Zero Energy Buildings (NZEBs) in order to increase their market uptake;

• Building capacity and provide support for sustainable energy policy implementation.

17 (22/12/2016)

Buildings – Topics 2016-2017

• Topics EE-11-2016-2017

Deep renovation of buildings

• Topic EE-12-2017 (EeB-PPP)

Demand response in energy management systems

• Topic EE-14-2016-2017

Construction skills

18 (22/12/2016)

Industry and service sectors represent more than 39% of the EU's final energy consumption

Industry, services and products

• Design of manufacturing processes, energy recovery, energy

audits and energy management systems

• Re-use of industrial waste,

• Optimisation of the value chain

• Development and market uptake of innovative highly efficient

energy-related products, systems and services

.

19 (22/12/2016)

Industry, services and products – Topics 2016-2017

• Topic EE-15-2017, EE-18-2017

Capacity building in industry and energy services for industrial parks

• Topic EE-17-2016-2017 (SPIRE-PPP)

Waste heat recovery / Energy symbiosis in industrial systems

• Topic EE-16-2016-2017

Effective implementation of EU product legislation

• Topic EE-20-2017

Energy efficient and integrated data centres

• Topic EE-19-2017

Public procurement of innovative energy efficiency solutions

20 (22/12/2016)

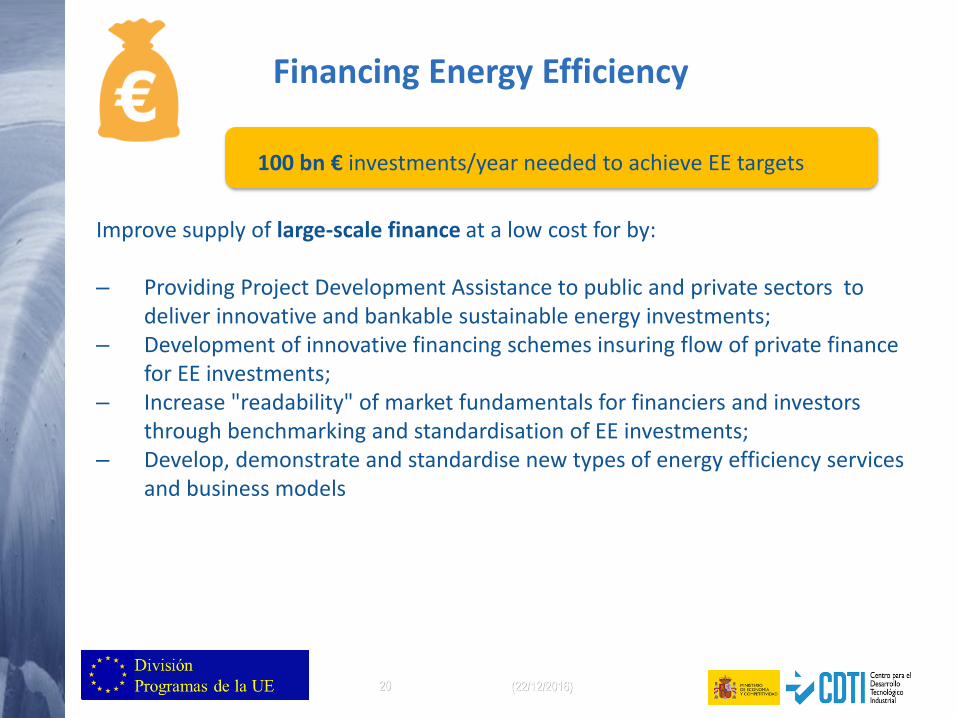

Financing Energy Efficiency

100 bn € investments/year needed to achieve EE targets

Improve supply of large-scale finance at a low cost for by:

– Providing Project Development Assistance to public and private sectors to deliver innovative and bankable sustainable energy investments;

– Development of innovative financing schemes insuring flow of private finance for EE investments;

– Increase "readability" of market fundamentals for financiers and investors through benchmarking and standardisation of EE investments;

– Develop, demonstrate and standardise new types of energy efficiency services and business models

21 (22/12/2016)

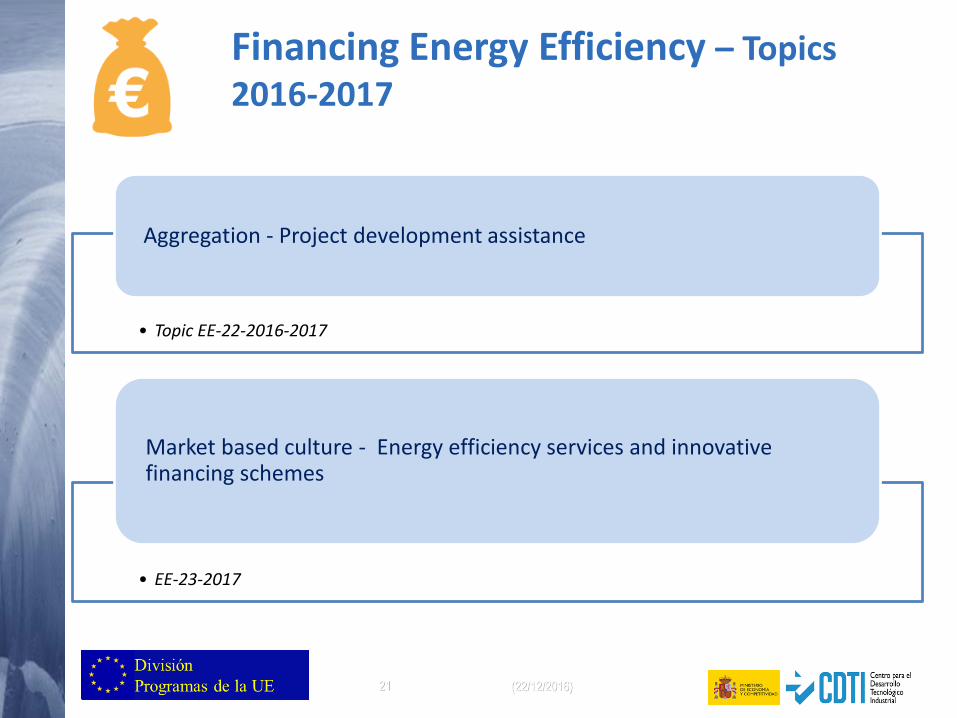

Financing Energy Efficiency – Topics 2016-2017

• Topic EE-22-2016-2017

Aggregation - Project development assistance

• EE-23-2017

Market based culture - Energy efficiency services and innovative financing schemes

22 (22/12/2016)

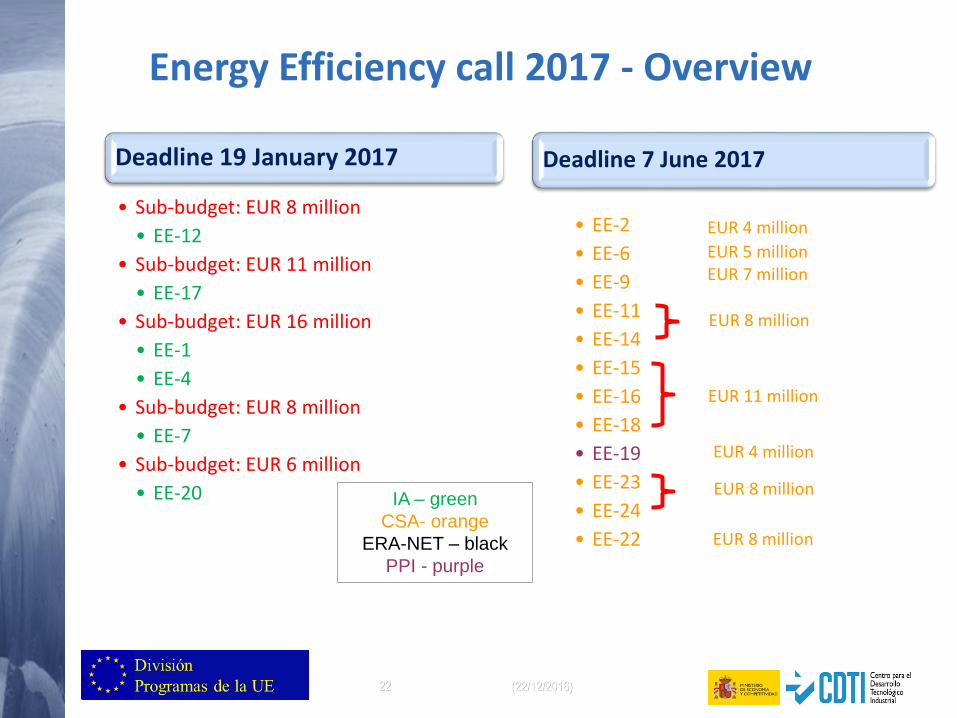

Energy Efficiency call 2017 - Overview

Deadline 19 January 2017

• Sub-budget: EUR 8 million

• EE-12

• Sub-budget: EUR 11 million

• EE-17

• Sub-budget: EUR 16 million

• EE-1

• EE-4

• Sub-budget: EUR 8 million

• EE-7

• Sub-budget: EUR 6 million

• EE-20

Deadline 7 June 2017

• EE-2

• EE-6

• EE-9

• EE-11

• EE-14

• EE-15

• EE-16

• EE-18

• EE-19

• EE-23

• EE-24

• EE-22

IA – green

CSA- orange

ERA-NET – black

PPI - purple

EUR 4 million

EUR 5 millionEUR 7 million

EUR 8 million

EUR 11 million

EUR 4 million

EUR 8 million

EUR 8 million

23 (22/12/2016)

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

24 (22/12/2016)

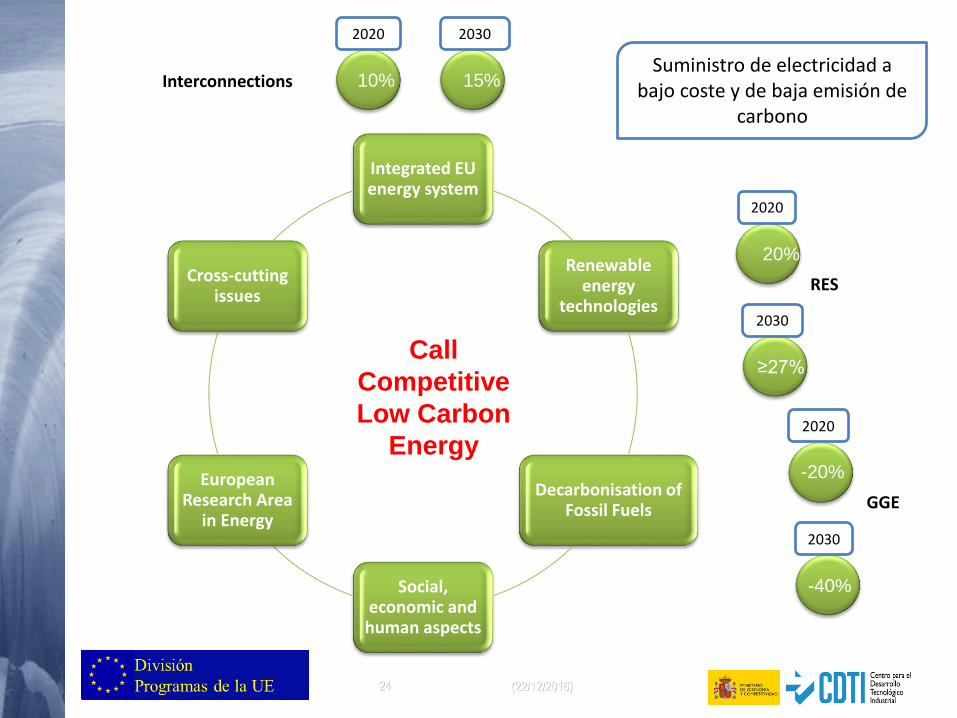

Integrated EU energy system

Renewable energy

technologies

Decarbonisation of Fossil Fuels

Social, economic and human aspects

European Research Area

in Energy

Cross-cutting issues

Call

Competitive

Low Carbon

Energy

Suministro de electricidad a bajo coste y de baja emisión de

carbono

2020 2030

2020

2030

2020

2030

10%

≥27%

20%

15%

-40%

-20%

Interconnections

RES

GGE

25 (22/12/2016)

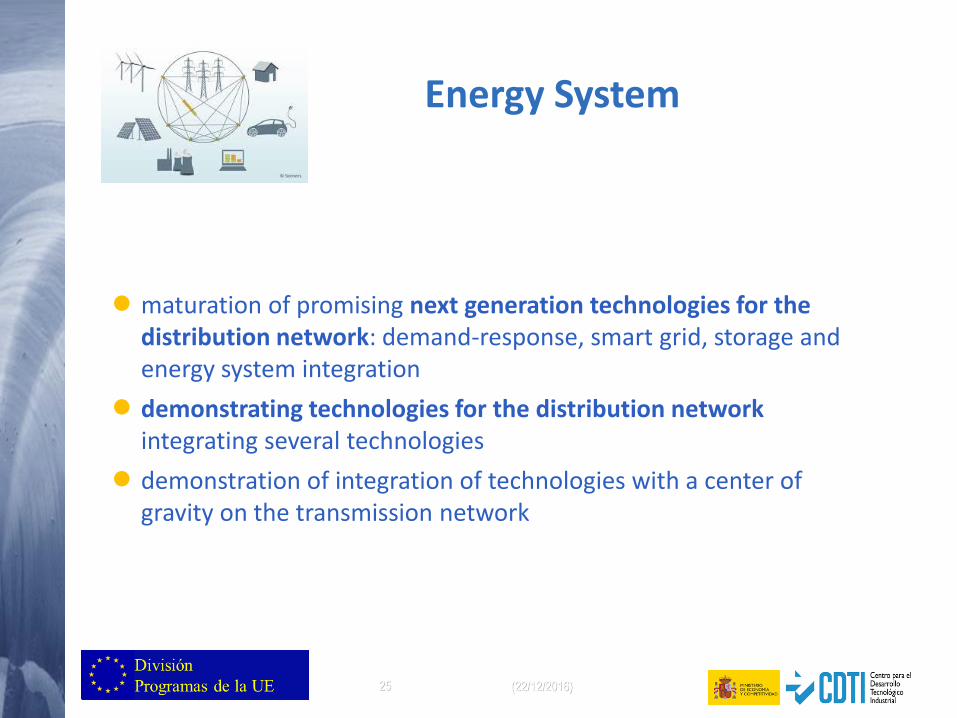

Energy System

● maturation of promising next generation technologies for the distribution network: demand-response, smart grid, storage and energy system integration

● demonstrating technologies for the distribution network integrating several technologies

● demonstration of integration of technologies with a center of gravity on the transmission network

26 (22/12/2016)

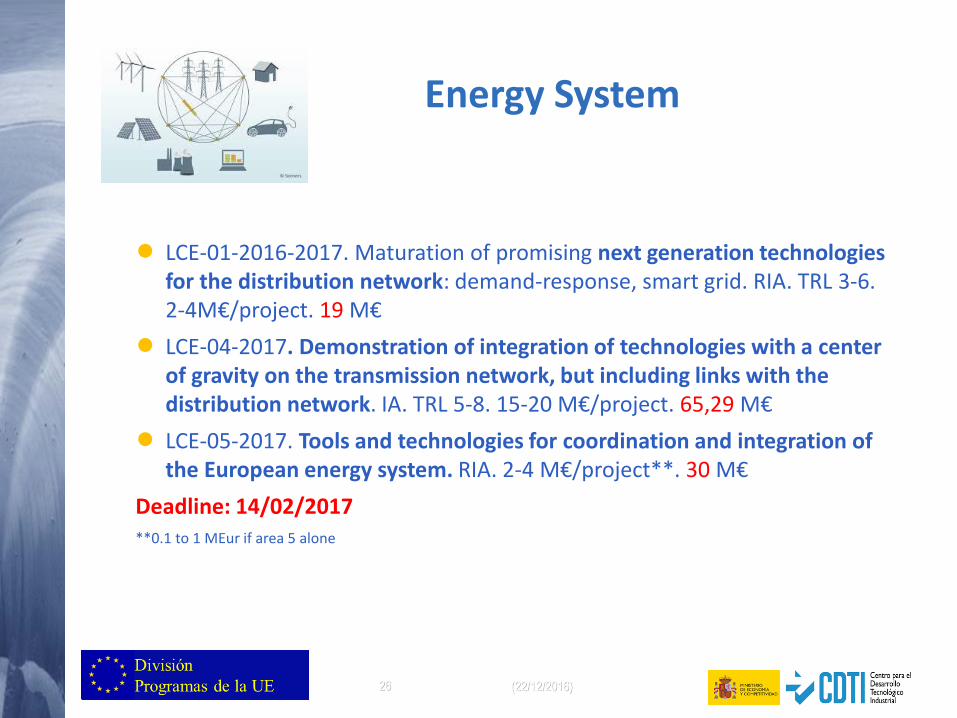

Energy System

● LCE-01-2016-2017. Maturation of promising next generation technologies for the distribution network: demand-response, smart grid. RIA. TRL 3-6. 2-4M€/project. 19 M€

● LCE-04-2017. Demonstration of integration of technologies with a center of gravity on the transmission network, but including links with the distribution network. IA. TRL 5-8. 15-20 M€/project. 65,29 M€

● LCE-05-2017. Tools and technologies for coordination and integration of the European energy system. RIA. 2-4 M€/project**. 30 M€

Deadline: 14/02/2017**0.1 to 1 MEur if area 5 alone

27 (22/12/2016)

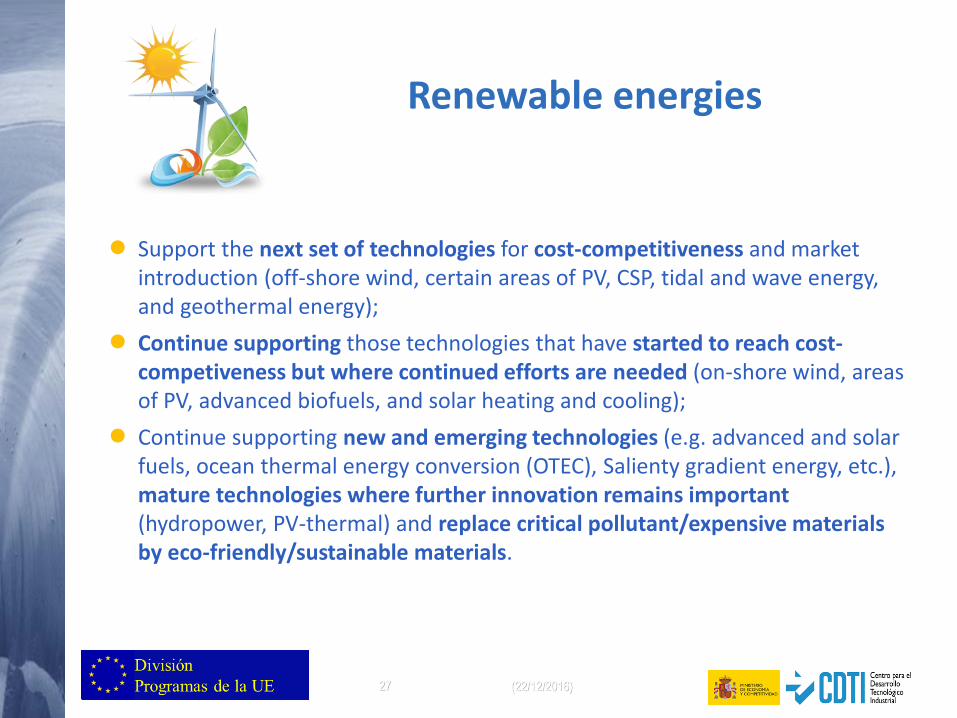

Renewable energies

● Support the next set of technologies for cost-competitiveness and market introduction (off-shore wind, certain areas of PV, CSP, tidal and wave energy, and geothermal energy);

● Continue supporting those technologies that have started to reach cost-competiveness but where continued efforts are needed (on-shore wind, areas of PV, advanced biofuels, and solar heating and cooling);

● Continue supporting new and emerging technologies (e.g. advanced and solar fuels, ocean thermal energy conversion (OTEC), Salienty gradient energy, etc.), mature technologies where further innovation remains important (hydropower, PV-thermal) and replace critical pollutant/expensive materials by eco-friendly/sustainable materials.

28 (22/12/2016)

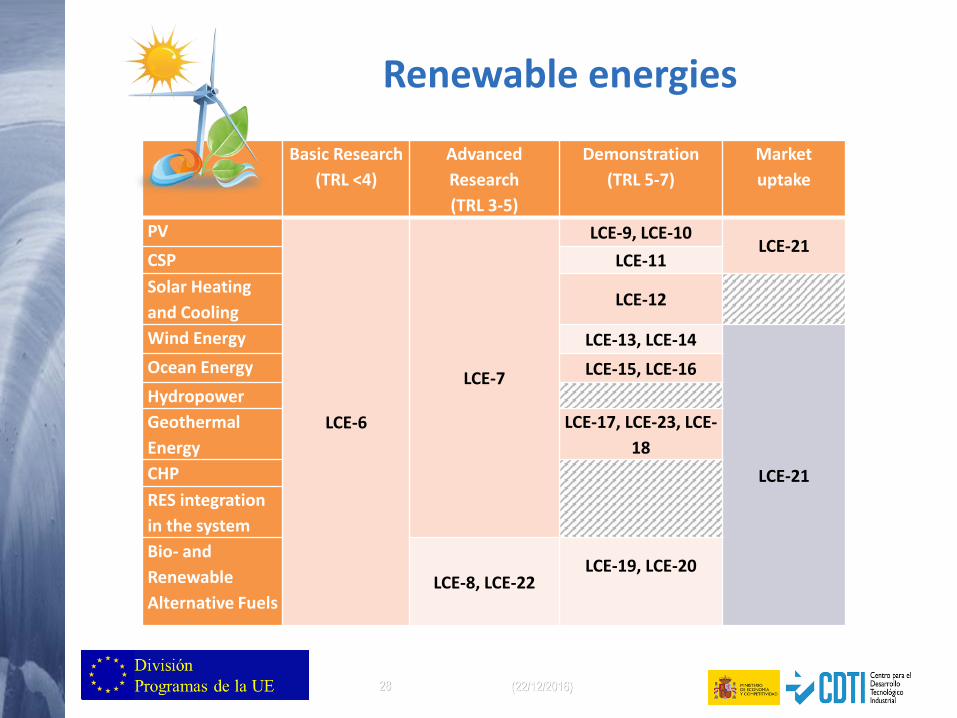

Renewable energies

Basic Research

(TRL <4)

Advanced

Research

(TRL 3-5)

Demonstration

(TRL 5-7)

Market

uptake

PV

LCE-6

LCE-7

LCE-9, LCE-10LCE-21

CSP LCE-11

Solar Heating

and CoolingLCE-12

Wind Energy LCE-13, LCE-14

LCE-21

Ocean Energy LCE-15, LCE-16

Hydropower

Geothermal

Energy

LCE-17, LCE-23, LCE-

18

CHP

RES integration

in the system

Bio- and

Renewable

Alternative FuelsLCE-8, LCE-22

LCE-19, LCE-20

29 (22/12/2016)

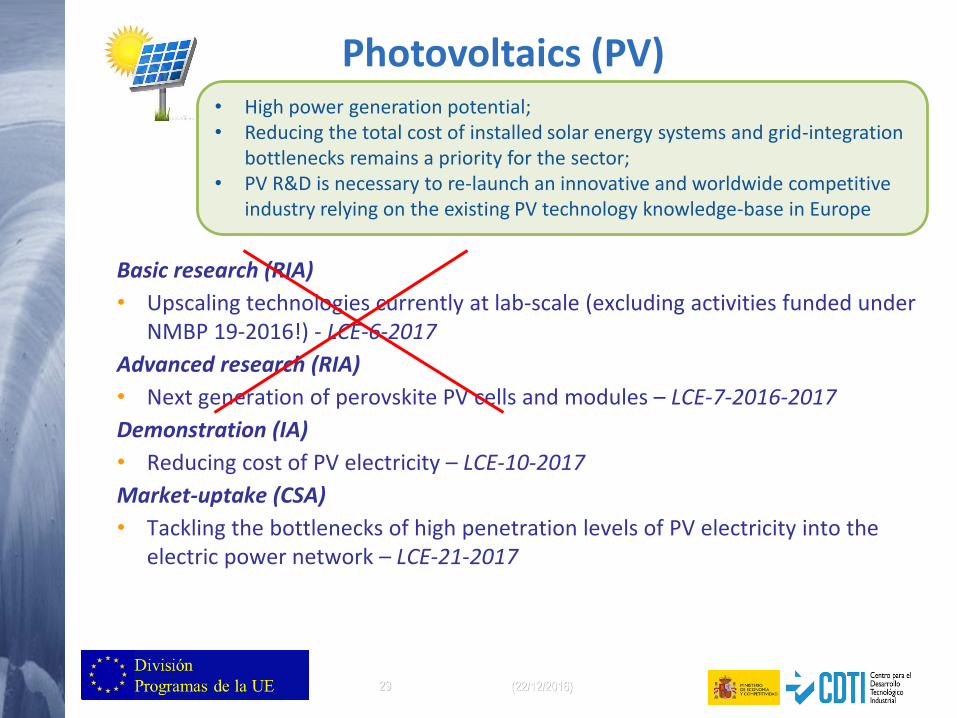

Photovoltaics (PV)

Basic research (RIA)

• Upscaling technologies currently at lab-scale (excluding activities funded underNMBP 19-2016!) - LCE-6-2017

Advanced research (RIA)

• Next generation of perovskite PV cells and modules – LCE-7-2016-2017

Demonstration (IA)

• Reducing cost of PV electricity – LCE-10-2017

Market-uptake (CSA)

• Tackling the bottlenecks of high penetration levels of PV electricity into the electric power network – LCE-21-2017

• High power generation potential;• Reducing the total cost of installed solar energy systems and grid-integration

bottlenecks remains a priority for the sector;• PV R&D is necessary to re-launch an innovative and worldwide competitive

industry relying on the existing PV technology knowledge-base in Europe

30 (22/12/2016)

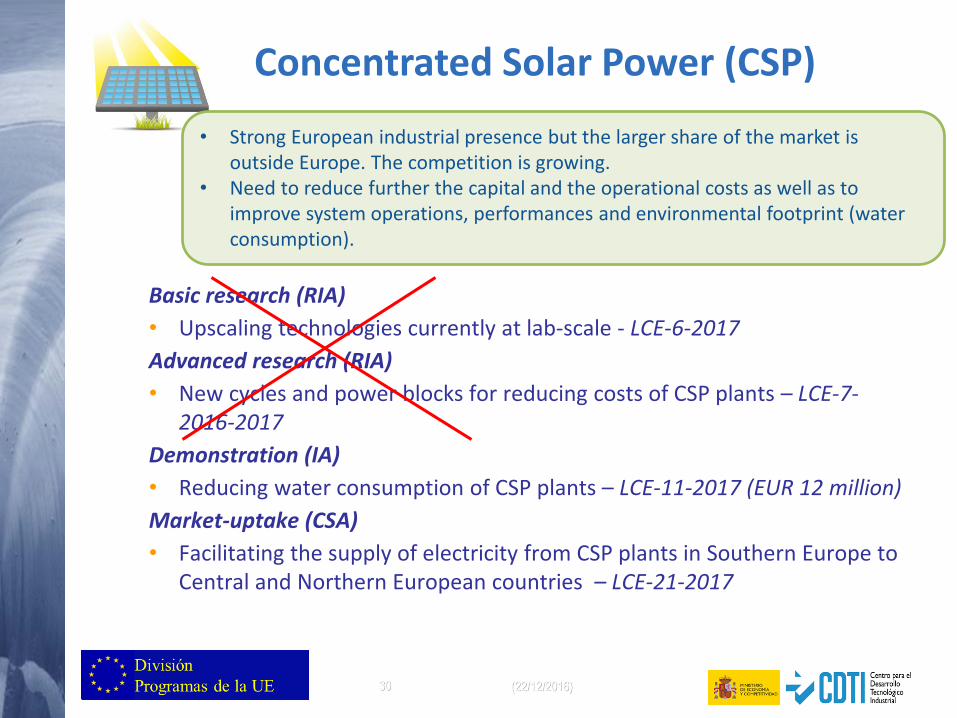

Concentrated Solar Power (CSP)

Basic research (RIA)

• Upscaling technologies currently at lab-scale - LCE-6-2017

Advanced research (RIA)

• New cycles and power blocks for reducing costs of CSP plants – LCE-7-2016-2017

Demonstration (IA)

• Reducing water consumption of CSP plants – LCE-11-2017 (EUR 12 million)

Market-uptake (CSA)

• Facilitating the supply of electricity from CSP plants in Southern Europe to Central and Northern European countries – LCE-21-2017

• Strong European industrial presence but the larger share of the market is outside Europe. The competition is growing.

• Need to reduce further the capital and the operational costs as well as to improve system operations, performances and environmental footprint (water consumption).

31 (22/12/2016)

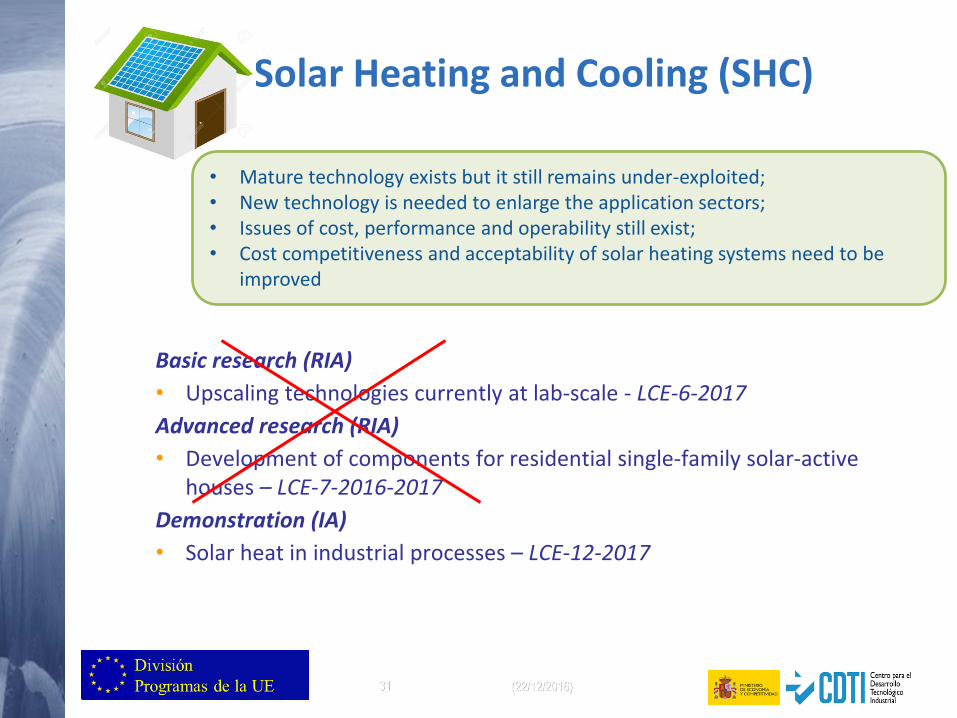

Solar Heating and Cooling (SHC)

Basic research (RIA)

• Upscaling technologies currently at lab-scale - LCE-6-2017

Advanced research (RIA)

• Development of components for residential single-family solar-active houses – LCE-7-2016-2017

Demonstration (IA)

• Solar heat in industrial processes – LCE-12-2017

• Mature technology exists but it still remains under-exploited; • New technology is needed to enlarge the application sectors;• Issues of cost, performance and operability still exist;• Cost competitiveness and acceptability of solar heating systems need to be

improved

32 (22/12/2016)

Geothermal energy

Basic research (RIA)

• Upscaling technologies currently at lab-scale - LCE-6-2017

Advanced research (RIA)

• Materials for geothermal installations (deep geothermal) – LCE-7-2016-2017

Demonstration (IA)

• Geothermal systems for retrofitting buildings – LCE-17-2017

• EGS in different geological conditions – LCE-18-2017

Market-uptake (CSA)

• Tackling bottlenecks for high penetration – LCE-21-2017• Accelerating the penetration of heat pumps for heating and cooling – LCE-21-

2017

• Geothermal energy has great untapped potential for diversifying the energy mix.• "Shallow geothermal": retroffiting existing installations with improved technology;• Enhanced geothermal systems (EGS): reduction of drilling costs and risks;

demonstration of viable technologies to create new reservoirs.

33 (22/12/2016)

Wind energy

Basic research (RIA)

• Improved understanding of the physics of wind as primary energy source and windenergy technology - LCE-6-2017

Advanced research (RIA)

• Reduction of environmental impact – LCE-7-2016-2017

Demonstration (IA)

• Large >10 MW wind turbines (logistics) – LCE-14-2017

Market-uptake (CSA)

• Increase market share of wind energy – LCE-21-2017

• European industries are still world leaders but the competition is growing;• Cost reductions for all components essential, in particular for offshore;• Offshore considered as the future market - large turbines to be demonstrated• Issues remain on environmental and social impact, and on public acceptance

34 (22/12/2016)

Ocean energy

Basic research (RIA)

• Upscaling technologies currently at lab-scale - LCE-6-2017

Advanced research (RIA)

• Innovative power take-off systems and control strategies – LCE-7-2016-2017

Demonstration (IA)

• Design tools for ocean energy devices and arrays development/deployment– LCE-16-2017

• European industries are leading the emergence of the technologies. • Many devices developed / prototypes tested, but market potential yet to be realised.• Demonstration of reliable and survivable systems essential.• Environmental, social and public impacts to be addressed

35 (22/12/2016)

Combined Heat and Power (CHP)

Basic research (RIA)

• Upscaling technologies currently at lab-scale - LCE-6-2017

Advanced research (RIA)

• Transforming renewable energy into intermediates – LCE-7-2016-2017

• CHP installations already in use, commercial applications exist and have been supported under previous framework programmes

• Market potential for residential scale and for specific industrial applications to increase generation flexibility.

36 (22/12/2016)

Integration of RES in the energy system

Advanced research (RIA)

LCE-7-2016-2017:

• Developing system support functions (or ancillary services) enabling RES technologies to contribute - at transmission and distribution grid level - to a stable and safe energy system;

• Define most suitable pathways for including integration considerations into the different RES development roadmaps

• Growing share of renewable energy sources requires rethink of system management;• Complementing activities supported under the area 'Integrated EU energy system',

integration is also addressed from the perspective of the generation sources in order to share burden and costs.

37 (22/12/2016)

Biofuels (1/2)

Basic research (RIA)

• Diversification of renewable fuel production through novel conversion routes/fuels -LCE-6-2017

Advanced research (RIA)

• LCE-8-2016-2017. Next generation of:

• Biofuels from CO2 in industrial waste flue gases through biochemicalconversion by autotrophic ( chemo and photo –autotrophic) micro-organisms;

• Biofuels from organic fraction of municipal and industrial wastes throughthermochemical, biochemical or chemical pathways with improvedperformance and sustainability;

• Biofuels from phototrophic algae & bacteria with improved performance and sustainability.

• European industries have leading technologies, but currently little deployment in EU;• Biofuels are medium-term solution for road and maritime transports and the only solution

for air transport;• Both biological and thermo-chemical pathways are necessary to provide technology

diversity, but the challenges in each pathway are different;• Large scale demonstrations are needed to boost market access;• Research needed to reduce cost, improve environmental impact and performance efficiency.

38 (22/12/2016)

Biofuels (2/2)

Demonstration (IA)

• LCE-19-2016-2017

• Biofuels from waste flue gases / other wastes and residues (2017)

• Biomass from aquatic biomass (2017)

• LCE-20-2016-2017

• Pre-commercial production of advanced aviation biofuels

Market-uptake (CSA)

• Market roll-out of liquid advanced biofuels and liquid renewablealternative fuels – LCE-21-2017

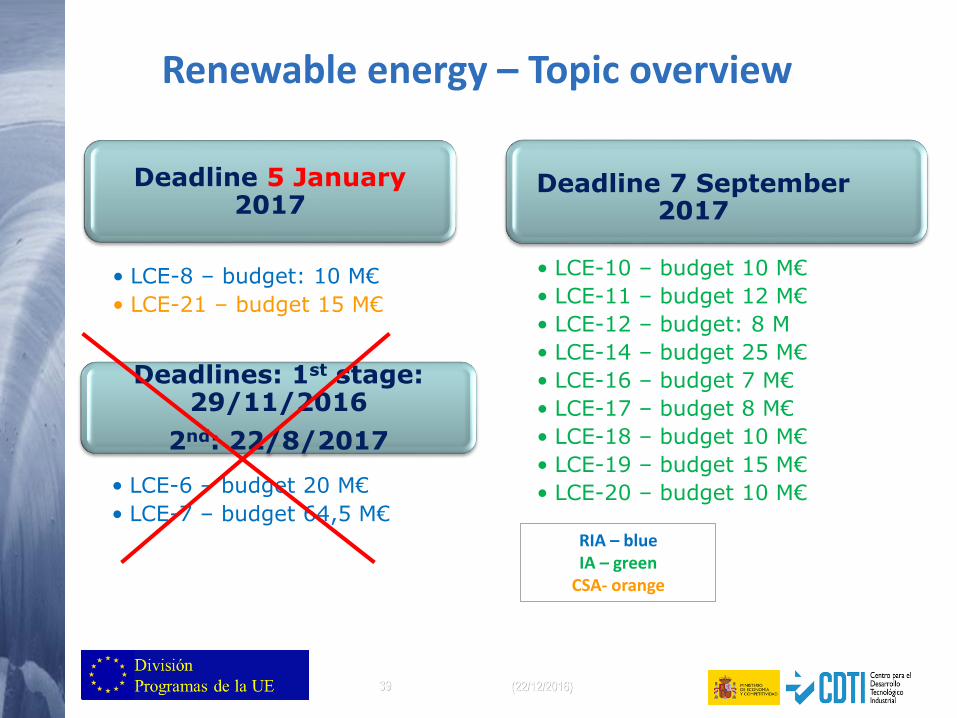

39 (22/12/2016)

Deadline 5 January 2017

• LCE-8 – budget: 10 M€

• LCE-21 – budget 15 M€

Deadline 7 September 2017

• LCE-10 – budget 10 M€

• LCE-11 – budget 12 M€

• LCE-12 – budget: 8 M

• LCE-14 – budget 25 M€

• LCE-16 – budget 7 M€

• LCE-17 – budget 8 M€

• LCE-18 – budget 10 M€

• LCE-19 – budget 15 M€

• LCE-20 – budget 10 M€

Renewable energy – Topic overview

Deadlines: 1st stage: 29/11/2016

2nd: 22/8/2017

• LCE-6 – budget 20 M€

• LCE-7 – budget 64,5 M€RIA – blueIA – green

CSA- orange

40 (22/12/2016)40

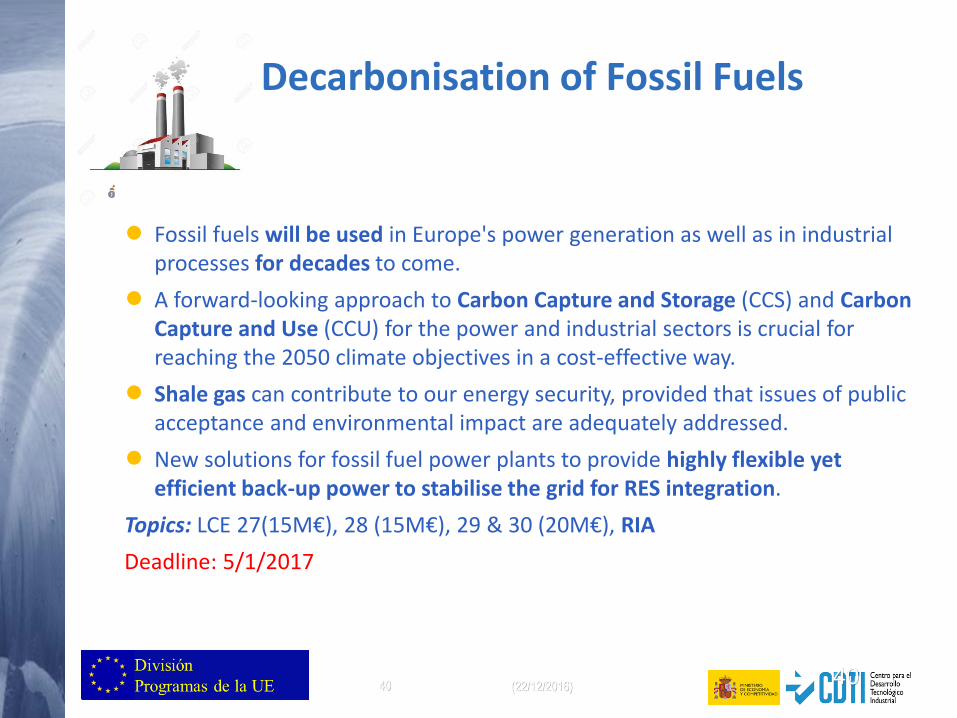

Decarbonisation of Fossil Fuels

● Fossil fuels will be used in Europe's power generation as well as in industrial processes for decades to come.

● A forward-looking approach to Carbon Capture and Storage (CCS) and Carbon Capture and Use (CCU) for the power and industrial sectors is crucial for reaching the 2050 climate objectives in a cost-effective way.

● Shale gas can contribute to our energy security, provided that issues of public acceptance and environmental impact are adequately addressed.

● New solutions for fossil fuel power plants to provide highly flexible yet efficient back-up power to stabilise the grid for RES integration.

Topics: LCE 27(15M€), 28 (15M€), 29 & 30 (20M€), RIA

Deadline: 5/1/2017

41 (22/12/2016)

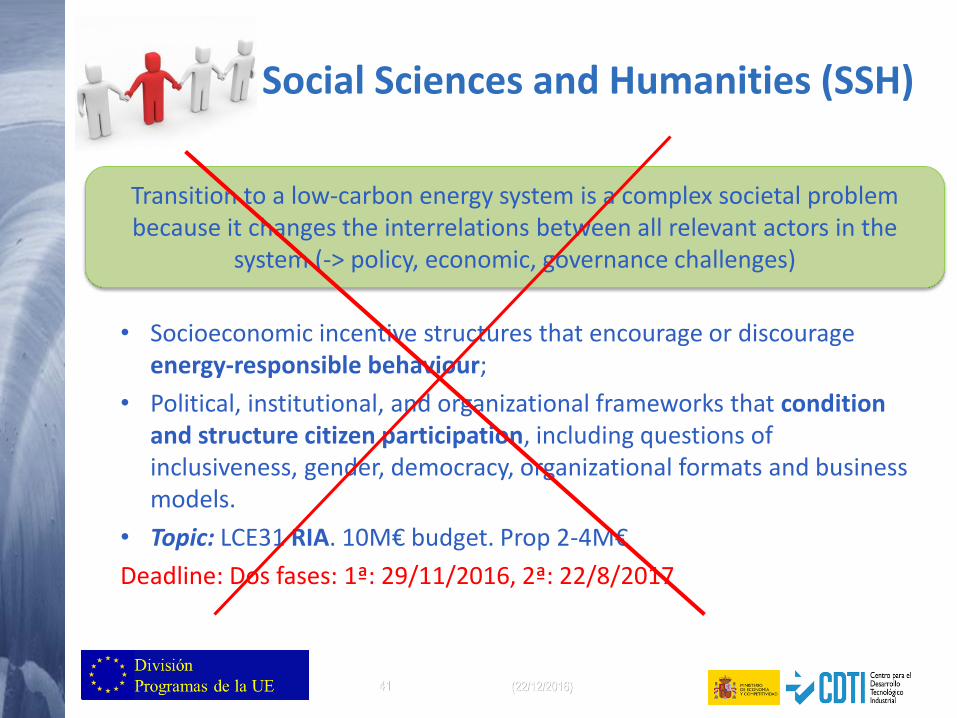

Social Sciences and Humanities (SSH)

• Socioeconomic incentive structures that encourage or discourage energy-responsible behaviour;

• Political, institutional, and organizational frameworks that condition and structure citizen participation, including questions of inclusiveness, gender, democracy, organizational formats and business models.

• Topic: LCE31 RIA. 10M€ budget. Prop 2-4M€

Deadline: Dos fases: 1ª: 29/11/2016, 2ª: 22/8/2017

Transition to a low-carbon energy system is a complex societal problem because it changes the interrelations between all relevant actors in the

system (-> policy, economic, governance challenges)

42 (22/12/2016)

Supporting the development of the European Research Area in energy

• Encourage coordination of national and EU efforts to increase effectiveness and efficiency;

• Pool resources and create critical mass to address challenges that no country can tackle alone;

• Align efforts to develop a European Research Area in energy and to create the Energy Union, one of the political priorities of the Juncker Commission;

• The new Integrated SET Plan provides the strategic framework for setting priorities and for discussing implementation;Topic: LCE 35,37 (ERA-NETs)

43 (22/12/2016)

Cross-cutting issues

Support to the energy stakeholders to contribute to the SET-Plan (LCE-36-2016-2017)

• Areas supported for 2017*:

– Geothermal Energy

44 (22/12/2016)

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

45 (22/12/2016)

Call Smart Cities and Communities

Improving quality of live, competitiveness and sustainability

Exporting European knowledge in a strong growth market estimated globally at €1.3 trillion in 2020

46 (22/12/2016)

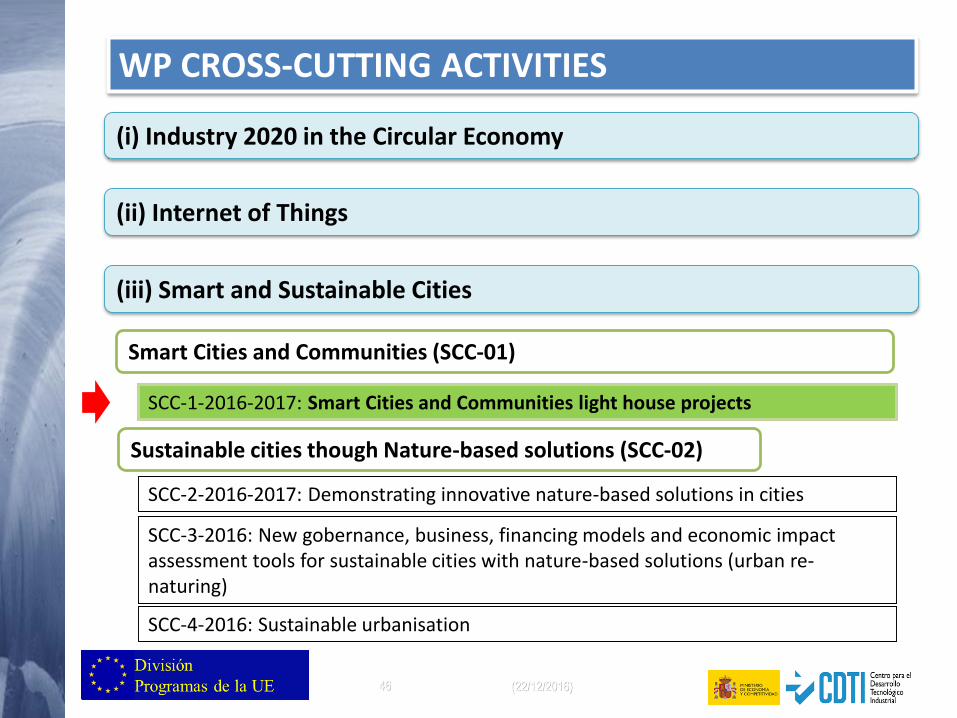

WP CROSS-CUTTING ACTIVITIES

(ii) Internet of Things

(iii) Smart and Sustainable Cities

(i) Industry 2020 in the Circular Economy

Smart Cities and Communities (SCC-01)

Sustainable cities though Nature-based solutions (SCC-02)

SCC-1-2016-2017: Smart Cities and Communities light house projects

SCC-2-2016-2017: Demonstrating innovative nature-based solutions in cities

SCC-3-2016: New gobernance, business, financing models and economic impact assessment tools for sustainable cities with nature-based solutions (urban re-naturing)

SCC-4-2016: Sustainable urbanisation

47 (22/12/2016)

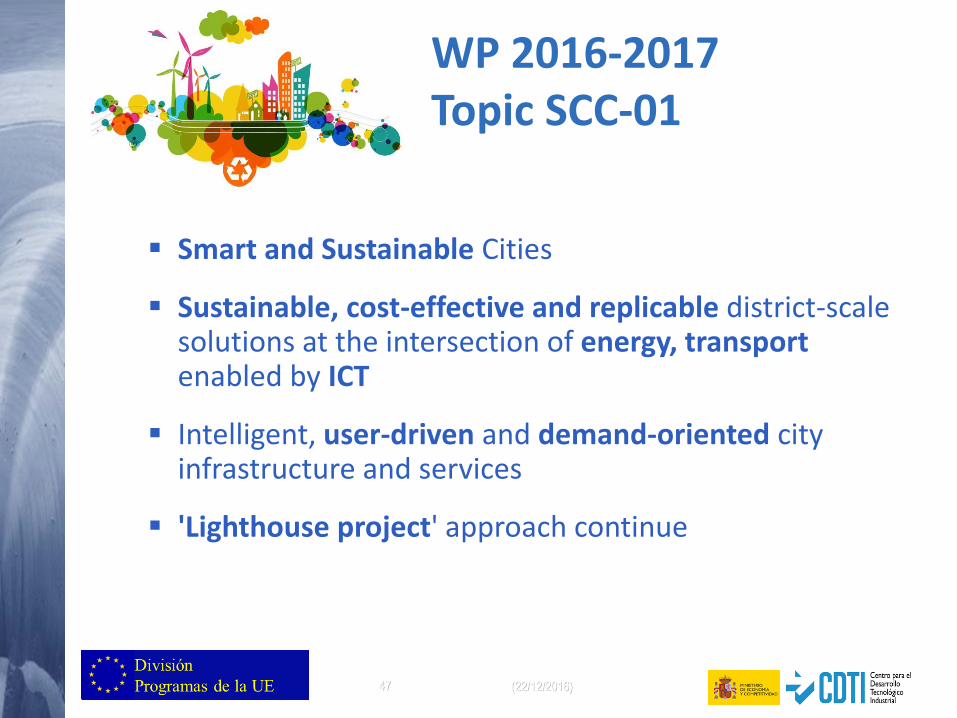

WP 2016-2017Topic SCC-01

Smart and Sustainable Cities

Sustainable, cost-effective and replicable district-scale solutions at the intersection of energy, transport enabled by ICT

Intelligent, user-driven and demand-oriented city infrastructure and services

'Lighthouse project' approach continue

48 (22/12/2016)

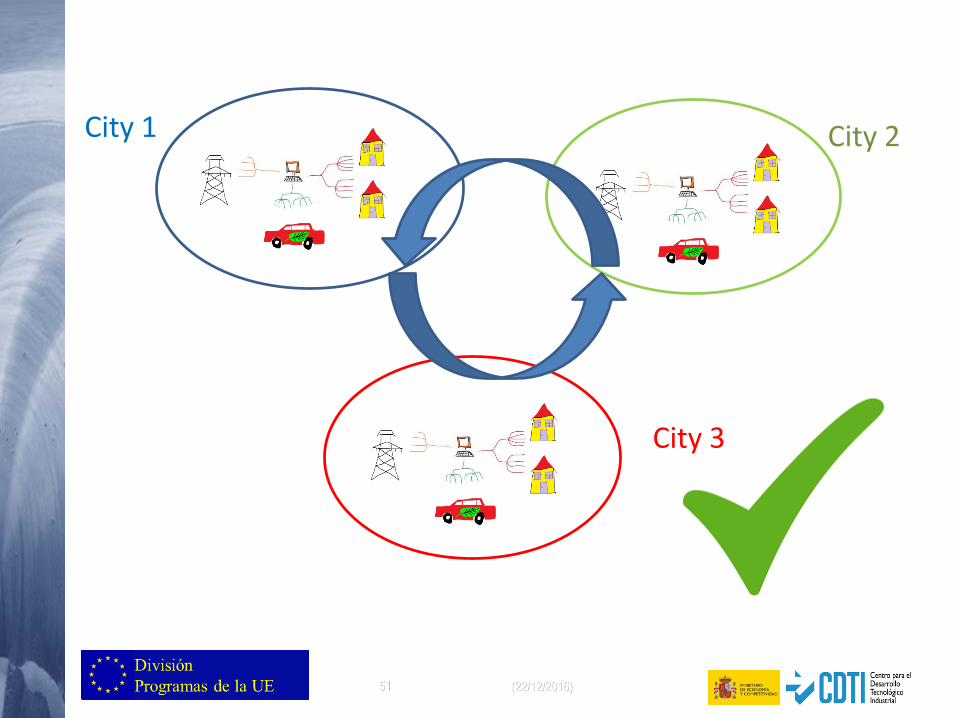

INTEGRATION

BALANCED COMBINATION

REPLICATION

• smart buildings (existing/new)

• smart grids (electricity, DH, telecom, water, etc…)

• energy storage,

• electric vehicles and smart charging infrastructures,

• latest generation ICT platforms based on open specifications

Capitalizing on synergies between components to increase efficiency and reduce costs.

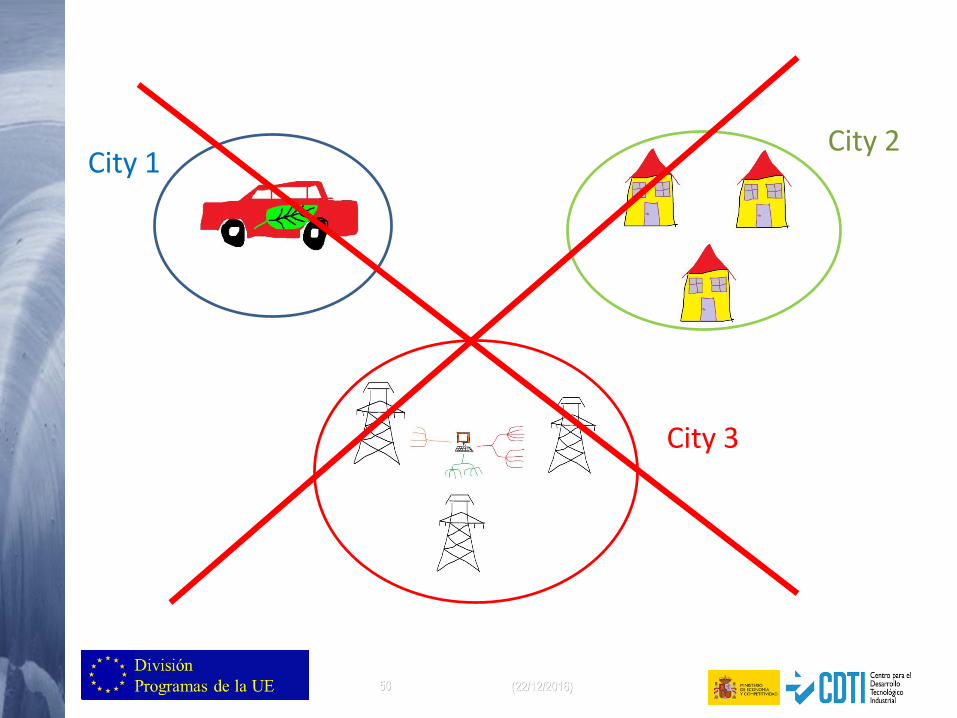

SCC1 calls 2016/2017 SCOPE

49 (22/12/2016)

Each PROJECT

Must:

• Be realised in 3 new ligthhouse cities situated in different EU member states or associated countries.

• Involved at least 3 follower cities from at least 3 different EU member states or associated countries.

SCC1 calls 2016/2017 SCOPE

50 (22/12/2016)

City 1City 2

City 3

51 (22/12/2016)

City 1 City 2

City 3

52 (22/12/2016)

Important details

A city can be funded as a lighthouse city only once under Horizon2020

Follower cities are defined as cities that have not yet acquired the full technical

competence to become a lighthouse city

Sustainable Energy Actions Plans (SEAP - Covenant of Mayors approved or

evaluated by DG JRC as having at least similar quality) are obligatory for

lighthouse cities.

Performance monitoring for at least 2 years

Convincing and realistic work, replication and investment plans

Incorporate all performance data into SCIS (Smart Cities Information System)

SCC1 calls 2016/2017 SCOPE

53 (22/12/2016)

CALL CONDITIONS

Foreseen contribution from the EU: between EUR 12 to 18 million / selected project

Call 2017:

Deadline: 14 February 2017Budget: 71,5 M.€

FAQ: https://ec.europa.eu/research/participants/portal/desktop/en/support/faq.html

Type of action: Innovation Action (IA)

54 (22/12/2016)

WP 2016-2017 ACTUALIZACIONES

55 (22/12/2016)

Índice

oContexto PolíticooPrograma de Trabajo 2016-2017: Eficiencia energética Energía Baja en Carbono Ciudades Inteligentes

oOtros

56 (22/12/2016)

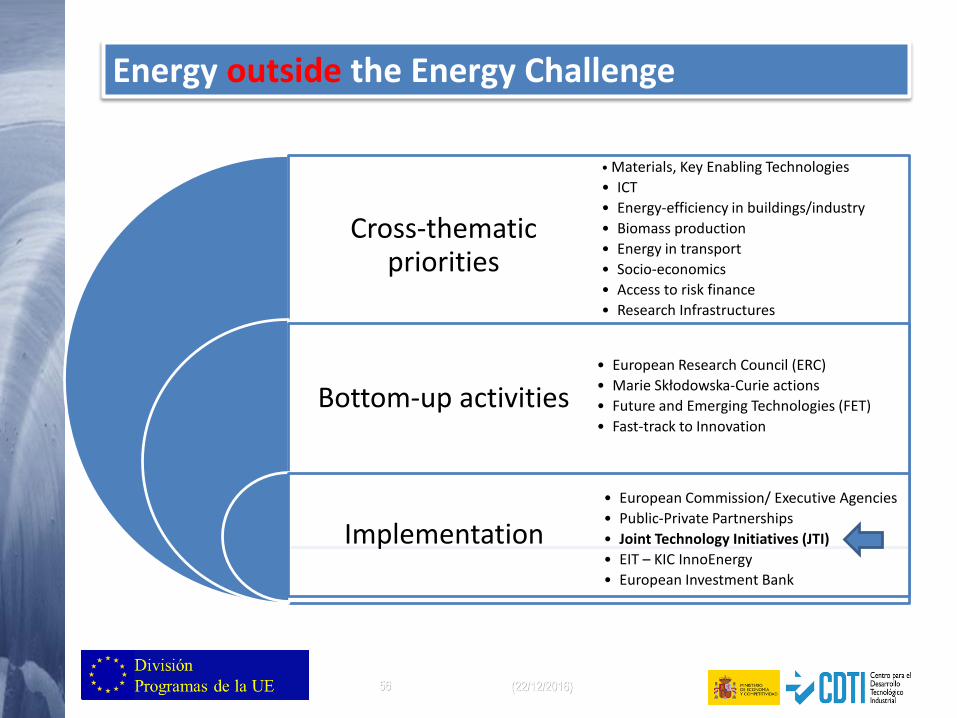

Energy outside the Energy Challenge

Cross-thematic priorities

Bottom-up activities

Implementation

• Materials, Key Enabling Technologies

• ICT

• Energy-efficiency in buildings/industry

• Biomass production

• Energy in transport

• Socio-economics

• Access to risk finance

• Research Infrastructures

• European Research Council (ERC)

• Marie Skłodowska-Curie actions

• Future and Emerging Technologies (FET)

• Fast-track to Innovation

• European Commission/ Executive Agencies

• Public-Private Partnerships

• Joint Technology Initiatives (JTI)

• EIT – KIC InnoEnergy

• European Investment Bank

57 (22/12/2016)

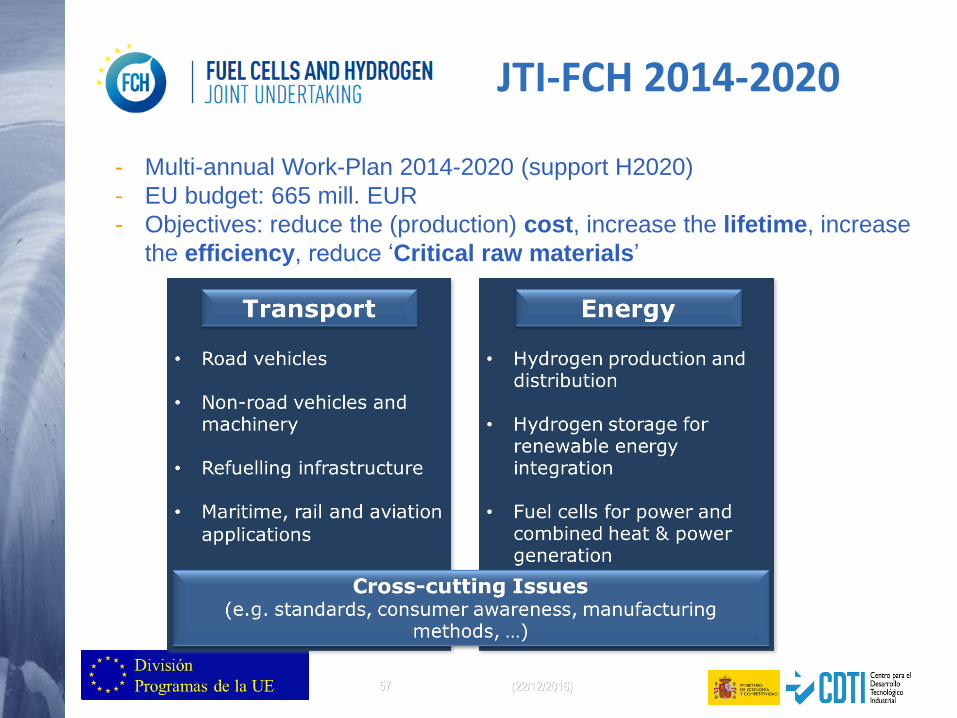

- Multi-annual Work-Plan 2014-2020 (support H2020)

- EU budget: 665 mill. EUR

- Objectives: reduce the (production) cost, increase the lifetime, increase

the efficiency, reduce ‘Critical raw materials’

JTI-FCH 2014-2020

58 (22/12/2016)

Resultados H2020:2014-2015 yprovisionales 2016

59 (22/12/2016)

2014-2015

60

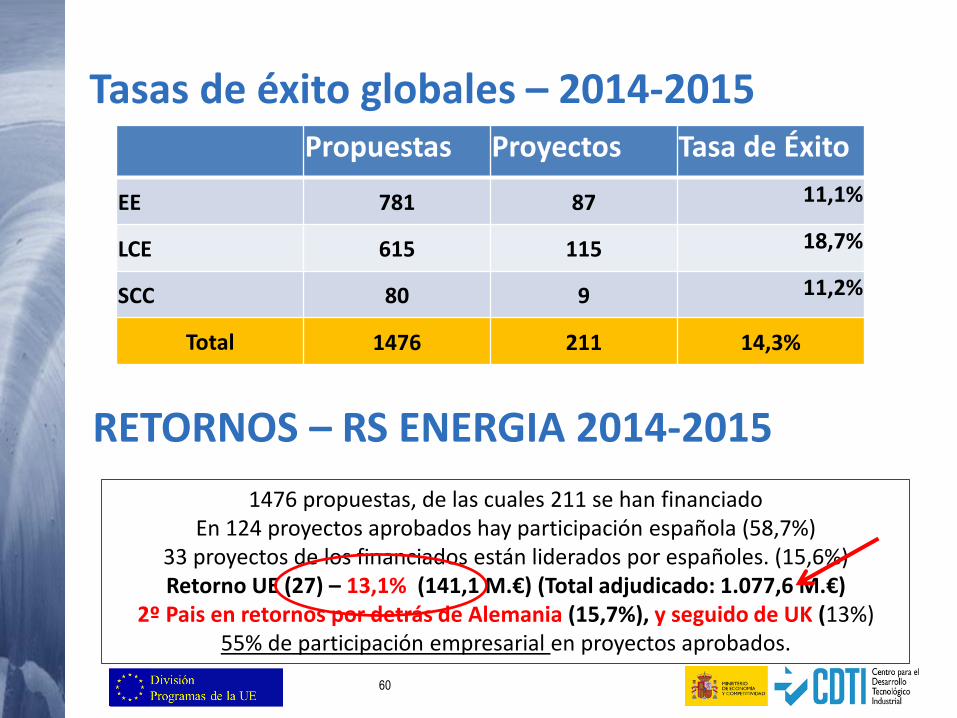

Tasas de éxito globales – 2014-2015Propuestas Proyectos Tasa de Éxito

EE 781 87 11,1%

LCE 615 115 18,7%

SCC 80 9 11,2%

Total 1476 211 14,3%

RETORNOS – RS ENERGIA 2014-2015

1476 propuestas, de las cuales 211 se han financiadoEn 124 proyectos aprobados hay participación española (58,7%)

33 proyectos de los financiados están liderados por españoles. (15,6%)Retorno UE (27) – 13,1% (141,1 M.€) (Total adjudicado: 1.077,6 M.€)

2º Pais en retornos por detrás de Alemania (15,7%), y seguido de UK (13%)55% de participación empresarial en proyectos aprobados.

61

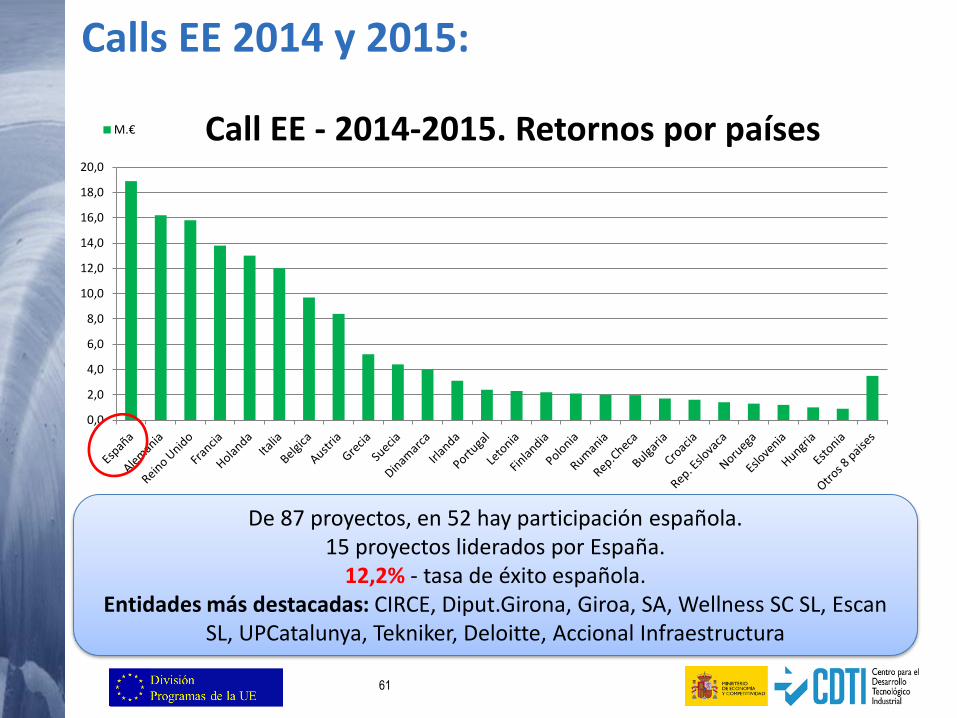

Calls EE 2014 y 2015:

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

Call EE - 2014-2015. Retornos por paísesM.€

De 87 proyectos, en 52 hay participación española.15 proyectos liderados por España.

12,2% - tasa de éxito española.Entidades más destacadas: CIRCE, Diput.Girona, Giroa, SA, Wellness SC SL, Escan

SL, UPCatalunya, Tekniker, Deloitte, Accional Infraestructura

62

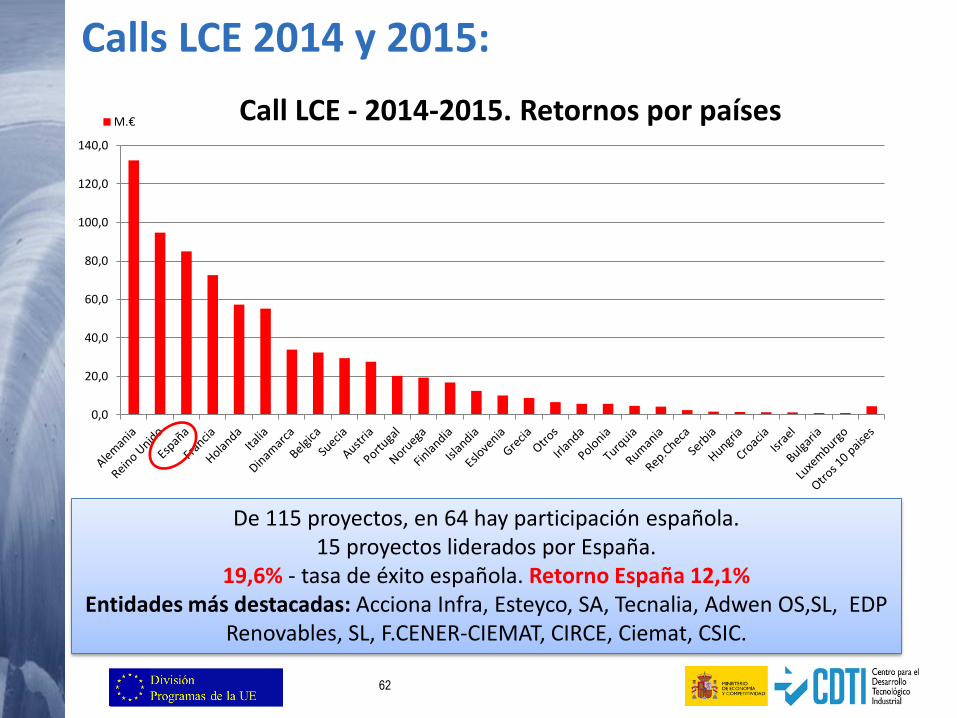

Calls LCE 2014 y 2015:

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

Call LCE - 2014-2015. Retornos por paísesM.€

De 115 proyectos, en 64 hay participación española.15 proyectos liderados por España.

19,6% - tasa de éxito española. Retorno España 12,1%Entidades más destacadas: Acciona Infra, Esteyco, SA, Tecnalia, Adwen OS,SL, EDP

Renovables, SL, F.CENER-CIEMAT, CIRCE, Ciemat, CSIC.

63

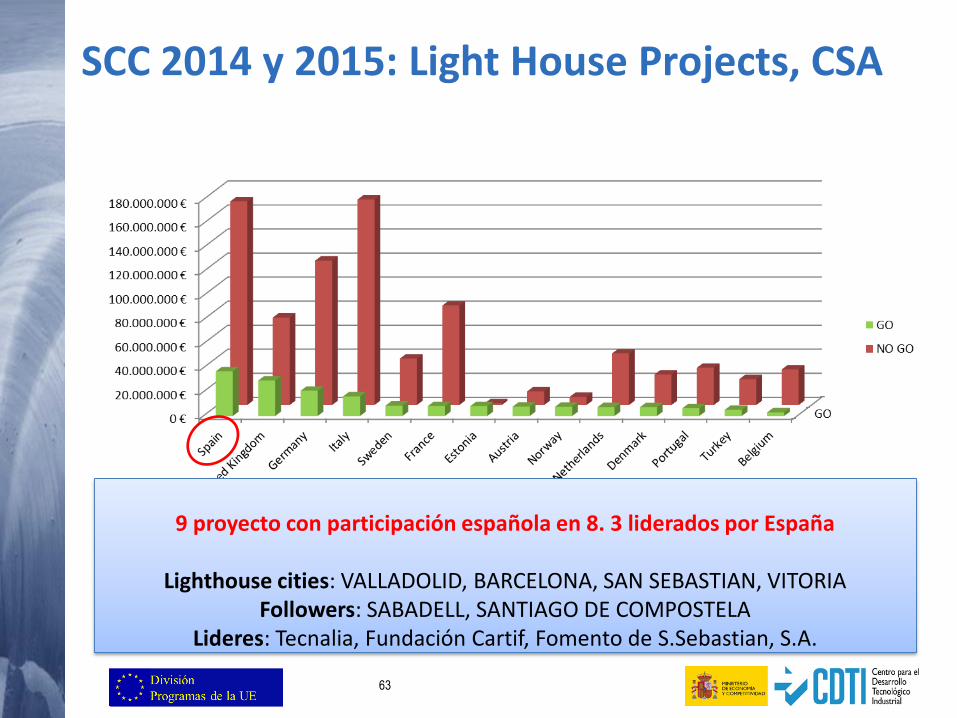

SCC 2014 y 2015: Light House Projects, CSA

9 proyecto con participación española en 8. 3 liderados por España

Lighthouse cities: VALLADOLID, BARCELONA, SAN SEBASTIAN, VITORIAFollowers: SABADELL, SANTIAGO DE COMPOSTELA

Lideres: Tecnalia, Fundación Cartif, Fomento de S.Sebastian, S.A.

64

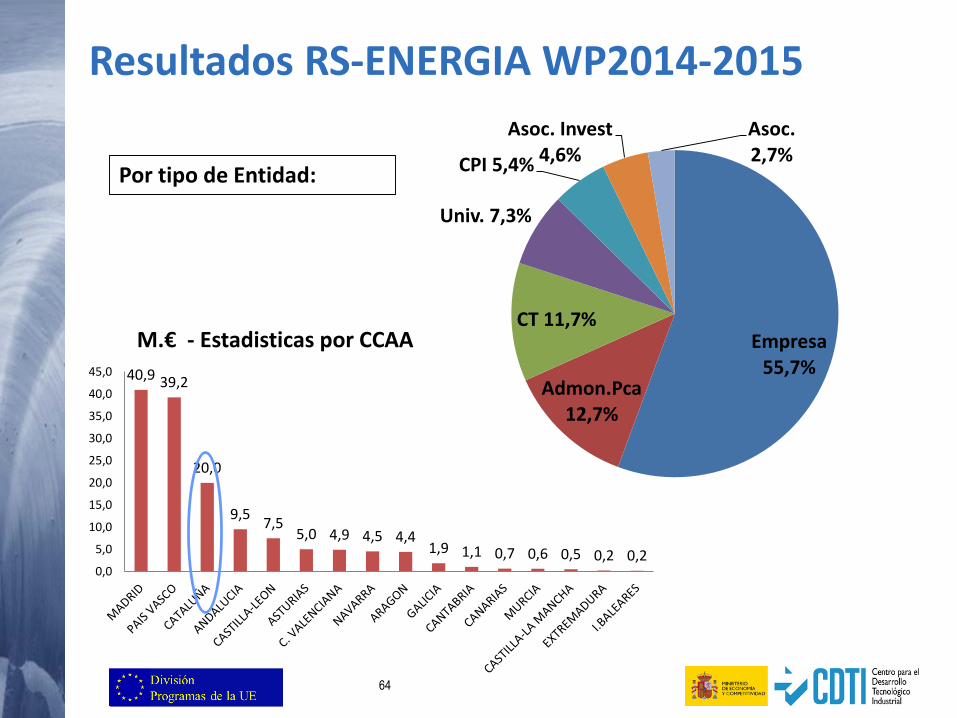

Resultados RS-ENERGIA WP2014-2015

Empresa 55,7%

Admon.Pca12,7%

CT 11,7%

Univ. 7,3%

CPI 5,4%

Asoc. Invest 4,6%

Asoc.2,7%

Por tipo de Entidad:

40,9 39,2

20,0

9,57,5

5,0 4,9 4,5 4,41,9 1,1 0,7 0,6 0,5 0,2 0,2

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

M.€ - Estadisticas por CCAA

65

2016 preliminares

66

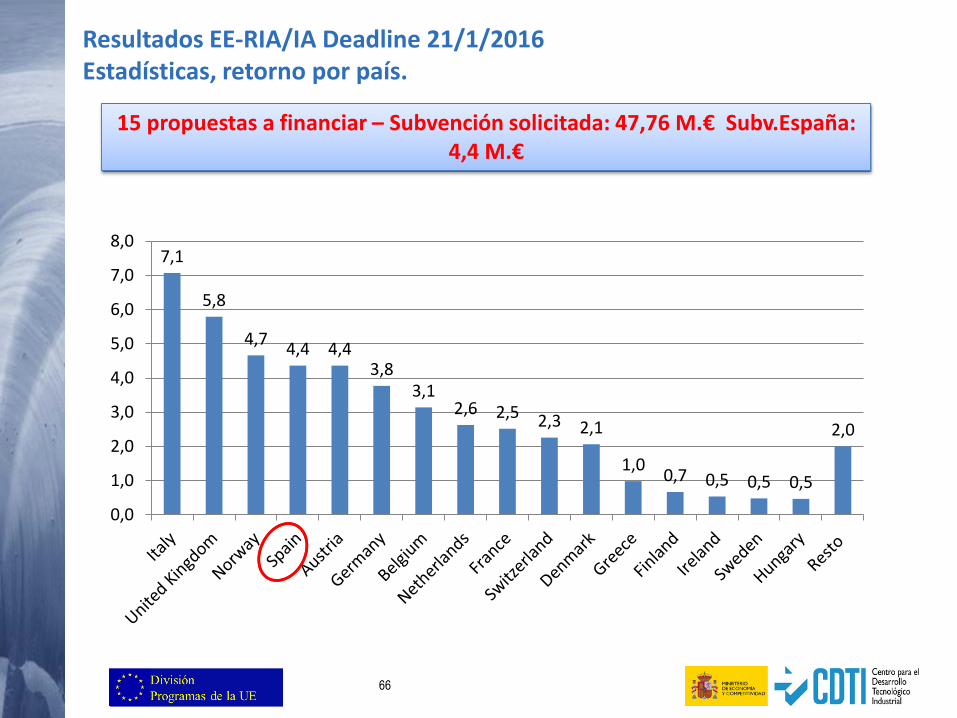

7,1

5,8

4,74,4 4,4

3,83,1

2,6 2,5 2,3 2,1

1,00,7 0,5 0,5 0,5

2,0

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

Resultados EE-RIA/IA Deadline 21/1/2016Estadísticas, retorno por país.

15 propuestas a financiar – Subvención solicitada: 47,76 M.€ Subv.España: 4,4 M.€

67

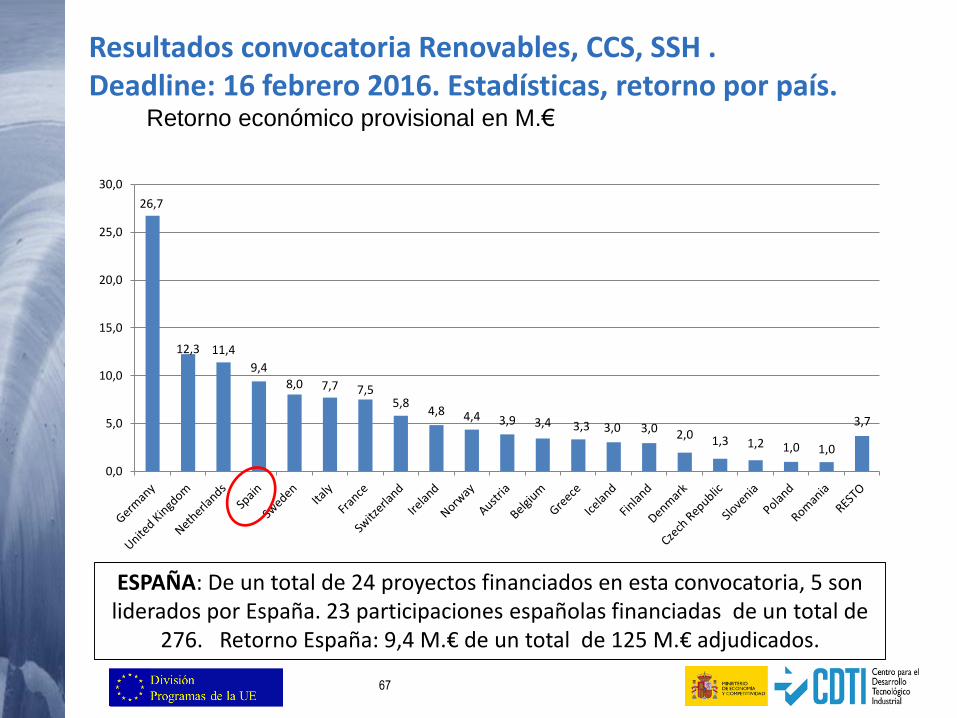

26,7

12,3 11,4

9,48,0 7,7 7,5

5,84,8 4,4 3,9 3,4 3,3 3,0 3,0 2,0 1,3 1,2 1,0 1,0

3,7

0,0

5,0

10,0

15,0

20,0

25,0

30,0

Resultados convocatoria Renovables, CCS, SSH . Deadline: 16 febrero 2016. Estadísticas, retorno por país.

Retorno económico provisional en M.€

ESPAÑA: De un total de 24 proyectos financiados en esta convocatoria, 5 son liderados por España. 23 participaciones españolas financiadas de un total de

276. Retorno España: 9,4 M.€ de un total de 125 M.€ adjudicados.

68

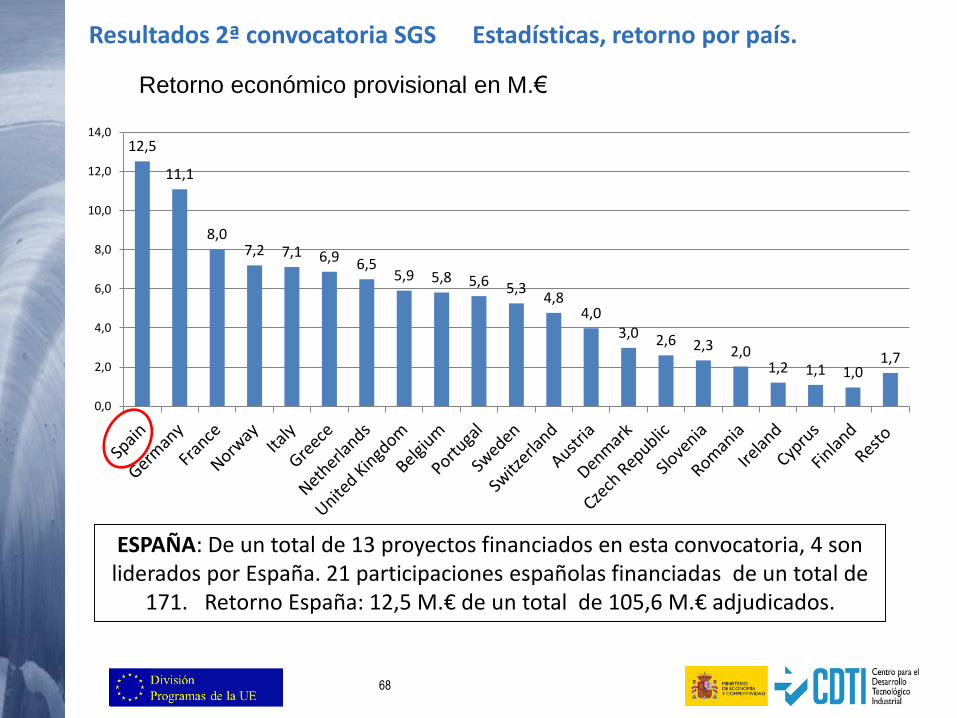

Resultados 2ª convocatoria SGS Estadísticas, retorno por país.

Retorno económico provisional en M.€

12,5

11,1

8,07,2 7,1 6,9 6,5

5,9 5,8 5,6 5,34,8

4,03,0 2,6 2,3 2,0

1,2 1,1 1,01,7

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

ESPAÑA: De un total de 13 proyectos financiados en esta convocatoria, 4 son liderados por España. 21 participaciones españolas financiadas de un total de

171. Retorno España: 12,5 M.€ de un total de 105,6 M.€ adjudicados.

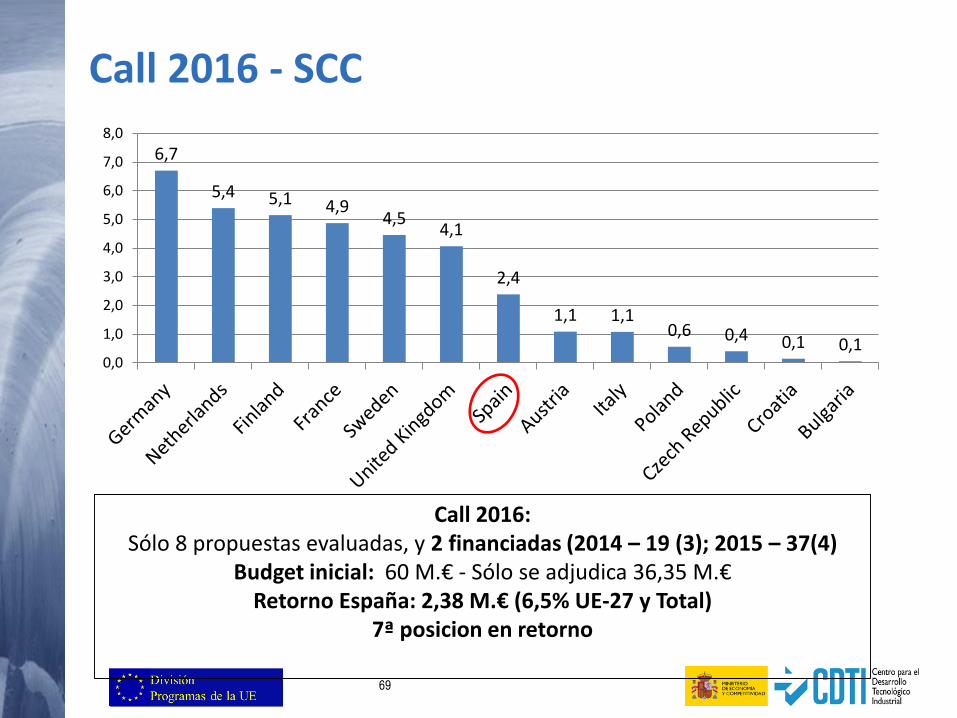

69

6,7

5,4 5,1 4,94,5

4,1

2,4

1,1 1,10,6 0,4 0,1 0,1

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

Call 2016 - SCC

Call 2016:Sólo 8 propuestas evaluadas, y 2 financiadas (2014 – 19 (3); 2015 – 37(4)

Budget inicial: 60 M.€ - Sólo se adjudica 36,35 M.€Retorno España: 2,38 M.€ (6,5% UE-27 y Total)

7ª posicion en retorno

70 (22/12/2016)

Y no olvidar…

Instrumento Pyme APC Programa de gestores en SOST Seminario de gestores…

29/01/2016 71

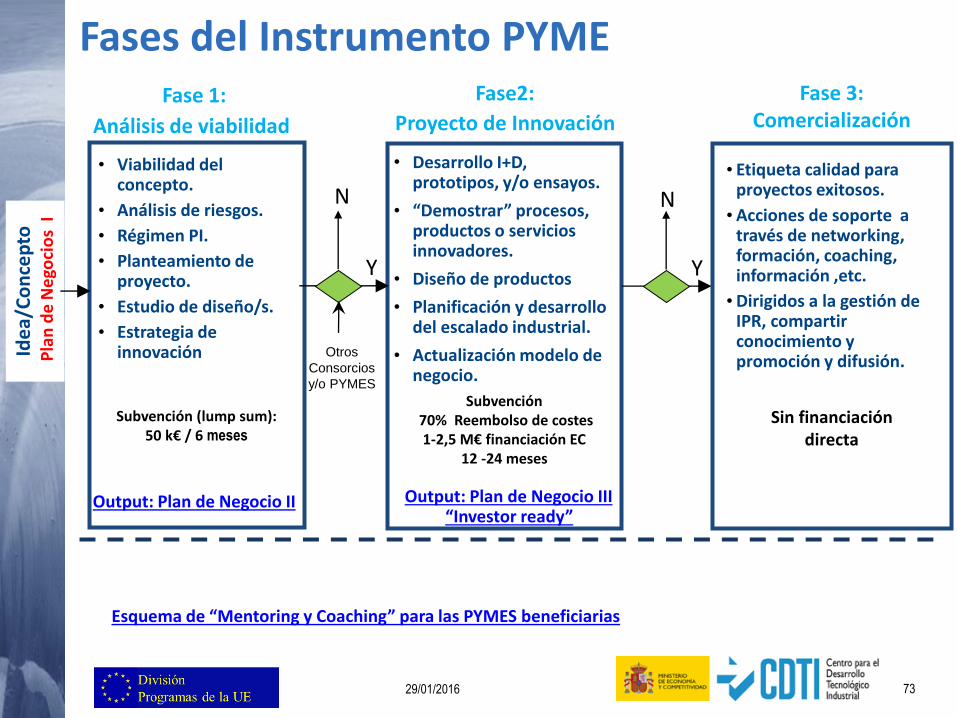

"The SME instrument is not an R&D programme. It is an accelerator for market introduction of promising

technological or non-technological innovations."

Subvención en fases para PYMES.

Sin requisito mínimo de consorcio.

Sólo para PYME como socios.

Subcontratación libre.

4 fechas de corte al año

CIERRE FASE 2 18/01/2017 CIERRE FASE 1 15/02/2017CIERRE FASE 2 06/04/2017CIERRE FASE 1 03/05/2017 CIERRE FASE 2 01/06/2017 CIERRE FASE 1 06/09/2017 CIERRE FASE 2 18/10/2017 CIERRE FASE 1 08/11/2017

29/01/2016 72

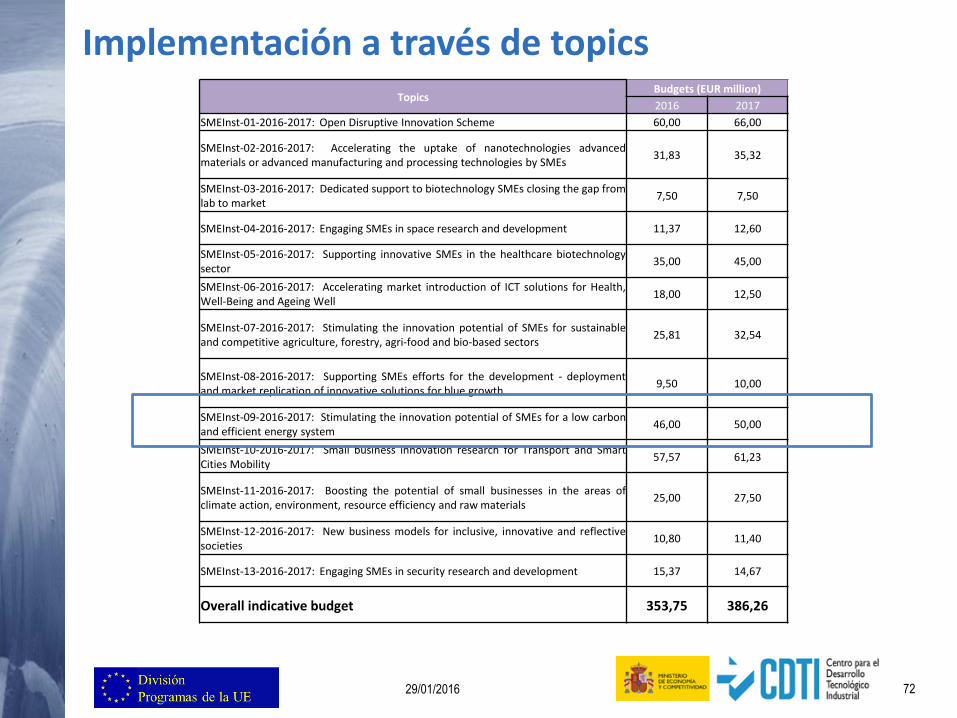

Implementación a través de topicsTopics

Budgets (EUR million)

2016 2017

SMEInst-01-2016-2017: Open Disruptive Innovation Scheme 60,00 66,00

SMEInst-02-2016-2017: Accelerating the uptake of nanotechnologies advancedmaterials or advanced manufacturing and processing technologies by SMEs

31,83 35,32

SMEInst-03-2016-2017: Dedicated support to biotechnology SMEs closing the gap fromlab to market

7,50 7,50

SMEInst-04-2016-2017: Engaging SMEs in space research and development 11,37 12,60

SMEInst-05-2016-2017: Supporting innovative SMEs in the healthcare biotechnologysector

35,00 45,00

SMEInst-06-2016-2017: Accelerating market introduction of ICT solutions for Health,Well-Being and Ageing Well

18,00 12,50

SMEInst-07-2016-2017: Stimulating the innovation potential of SMEs for sustainableand competitive agriculture, forestry, agri-food and bio-based sectors

25,81 32,54

SMEInst-08-2016-2017: Supporting SMEs efforts for the development - deploymentand market replication of innovative solutions for blue growth

9,50 10,00

SMEInst-09-2016-2017: Stimulating the innovation potential of SMEs for a low carbonand efficient energy system

46,00 50,00

SMEInst-10-2016-2017: Small business innovation research for Transport and SmartCities Mobility

57,57 61,23

SMEInst-11-2016-2017: Boosting the potential of small businesses in the areas ofclimate action, environment, resource efficiency and raw materials

25,00 27,50

SMEInst-12-2016-2017: New business models for inclusive, innovative and reflectivesocieties

10,80 11,40

SMEInst-13-2016-2017: Engaging SMEs in security research and development 15,37 14,67

Overall indicative budget 353,75 386,26

29/01/2016 73

Fase 1:

Análisis de viabilidad

Fase2:

Proyecto de Innovación

• Viabilidad del concepto.

• Análisis de riesgos.

• Régimen PI.

• Planteamiento de proyecto.

• Estudio de diseño/s.

• Estrategia de innovación

• Desarrollo I+D, prototipos, y/o ensayos.

• “Demostrar” procesos, productos o servicios innovadores.

• Diseño de productos

• Planificación y desarrollo del escalado industrial.

• Actualización modelo de negocio.

Subvención (lump sum):50 k€ / 6 meses

Fase 3: Comercialización

Subvención70% Reembolso de costes1-2,5 M€ financiación EC

12 -24 meses

• Etiqueta calidad para proyectos exitosos.

•Acciones de soporte a través de networking, formación, coaching, información ,etc.

•Dirigidos a la gestión de IPR, compartir conocimiento y promoción y difusión.

Sin financiación directa

Y

N

Y

N

Esquema de “Mentoring y Coaching” para las PYMES beneficiarias

Otros

Consorcios

y/o PYMES

Fases del Instrumento PYMEId

ea/

Co

nce

pto

Pla

n d

e N

ego

cio

s I

Output: Plan de Negocio II Output: Plan de Negocio III “Investor ready”

29/01/2016 74

Enlaces

https://ec.europa.eu/inea/en/news-events/events/2016-info-day-horizon-2020-smart-grids-and-storage

http://ec.europa.eu/research/index.cfm?pg=events&eventcode=E8549B02-9403-39F9-E71BF7B28BF5B857

https://ec.europa.eu/inea/en/news-events/events/h2020-energy-research-virtual-info-day

https://ec.europa.eu/easme/en/horizon-2020-secure-clean-and-efficient-energy-info-day

https://ec.europa.eu/inea/en/news-events/events/2016-information-day-horizon-2020-smart-cities-and-communities

75 (22/12/2016)

Roles en la gestión de Horizonte 2020

PARTICIPANTES

NCP

REPRESENTANTE

CCAA, MinisteriosExpertos

Mª Pilar González Gotor (NCP CDTI):[email protected]

Virginia Vivanco (NCP IDAE): [email protected]

Cristina Quintana (NCP CIEMAT): [email protected]

Mª Luisa Revilla:[email protected]

MUCHAS GRACIAS

Pilar González Gotor

Reto Energía – Horizonte 2020

División Programas Europeos- CDTI

partner search